The latest proposal has increased the interest rates for all crvUSD markets. We attempt to explain this as follows, assuming pegkeeper_filling = 0. According to the formula:

rate = rate0 * exp(depeg / sigma) * exp(- pegkeeper_filling / (total_debt * target_f))

The lending rate of crvUSD is positively correlated with price depeg. Assuming that the market can sustain a maximum rate r_max, and the final stable rate and the maximum borrowing amount are fixed.

When a depeg occurs, the current rate r_now > rate0, and during a significant depeg, r_now > r_normal.

From the formula, it's seen that increasing rate0 to rate0' results in a smaller depeg at the normal rate r_normal. In other words, increasing rate0 heightens the sensitivity of the rate to depeg. Conversely, a lower depeg leads to a higher rate.

Raising rate0 allows the rate to reach the maximum value r_max quicker, thus promoting the repayment and destruction of crvUSD and reducing depeg in the crvUSD pool.

We simulated scenarios where depeg varies from 0 to its maximum (users borrow more crvUSD and add it to the crvUSD pool, sustaining the depeg) and from the maximum back to 0 (users start buying back crvUSD and redeeming assets for crvUSD destruction as the rates gradually increase to the sustainable limit).

With rate0 set at 5%, 10%, and 15%, we found that increasing rate0 does not impose additional costs on users. Furthermore, it has three main advantages:

It results in a more minor degree of price de-anchoring and a quicker return to a depeg=0 state.

It allows users to reach their maximum borrowing amount of crvUSD earlier.

It causes the interest rate to rise to r_max sooner.

The simulation code is here: https://t.co/a5ixv8F4dX

@0xMC_com@paco0x

@euler_mab There might be a typographical error in the expression cye^(cy) = ce^(2c - x) / x. It appears that the correct form should be cye^(cy) = ce^(2c - cx) / x, where the 'c' in 'cx' seems to be missing in the former.

Is there an easy way to understand how crvUSD works?

Maybe these diagrams will help.

@CurveFinance@CurveCap

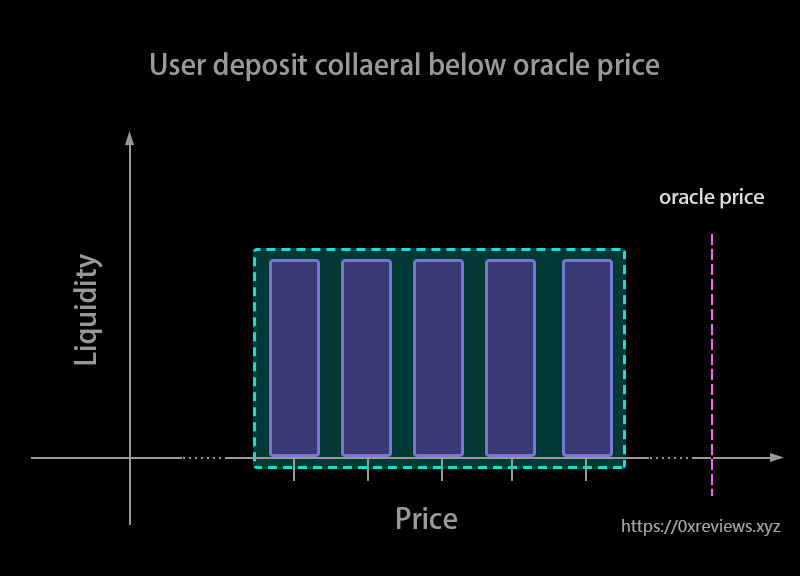

How crvUSD's AMM works (Soft-Liquidation):

1. The collateral deposited will be placed below the price

#crvUSD Automatically generate token flow charts for all soft-liquidations on LLAMMA.

After a hard time debugging, it finally looks less messy.

@CurveFinance

#crvUSD We are analyzing the soft liquidation on the LLAMMA pool, trying to generate a flow chart for each arbitrage transaction, which is a very time-consuming task.

Btw, Graphviz is a powerful tool, but it is challenging to use well. I may need a long time to explore...

🫠

4. Therefore, we need to make the liquidity and virtual reserves in regular AMMs like Uniswap V3 functions of P_oracle to adjust the price according to P_oracle. Finding such a function will allow us to obtain a very suitable AMM for settlement, namely LLAMMA.

#crvusd There is a Chinese video and an English article made by us explaining the mathematical derivation of the crvUSD whitepaper.

And we @0xstan_ and @paco0x will present a report on the behavior and motivation of arbitrageurs of crvUSD in a few weeks.

https://t.co/HSrCd5hrO7

the prices in the LLAMMA pool should be higher, making it more willing for outsiders to sell ETH to the pool. When the ETH falls, the ETH price should be lower, which allows outsiders to arbitrage in the pool, with price increases converting to ETH and price decreases to USDT.

4. Therefore, we need to make the liquidity and virtual reserves in regular AMMs like Uniswap V3 functions of P_oracle to adjust the price according to P_oracle. Finding such a function will allow us to obtain a very suitable AMM for settlement, namely LLAMMA.

making it more willing for outsiders to sell ETH to the pool. When the ETH falls, the ETH price should be lower, which allows outsiders to arbitrage and increase liquidity in the LLAMMA pool, with price increases converting to ETH and price decreases converting to USDT.

#crvusd In the case of violent market fluctuations, how does crvUSD maintain price stability by adjusting loan rates? I made a demo to show how it works.

It's mainly adjusted by two dimensions, crvUSD price and the ratio of PegKeepers' debt to total debt. @CurveFinance@CurveCap