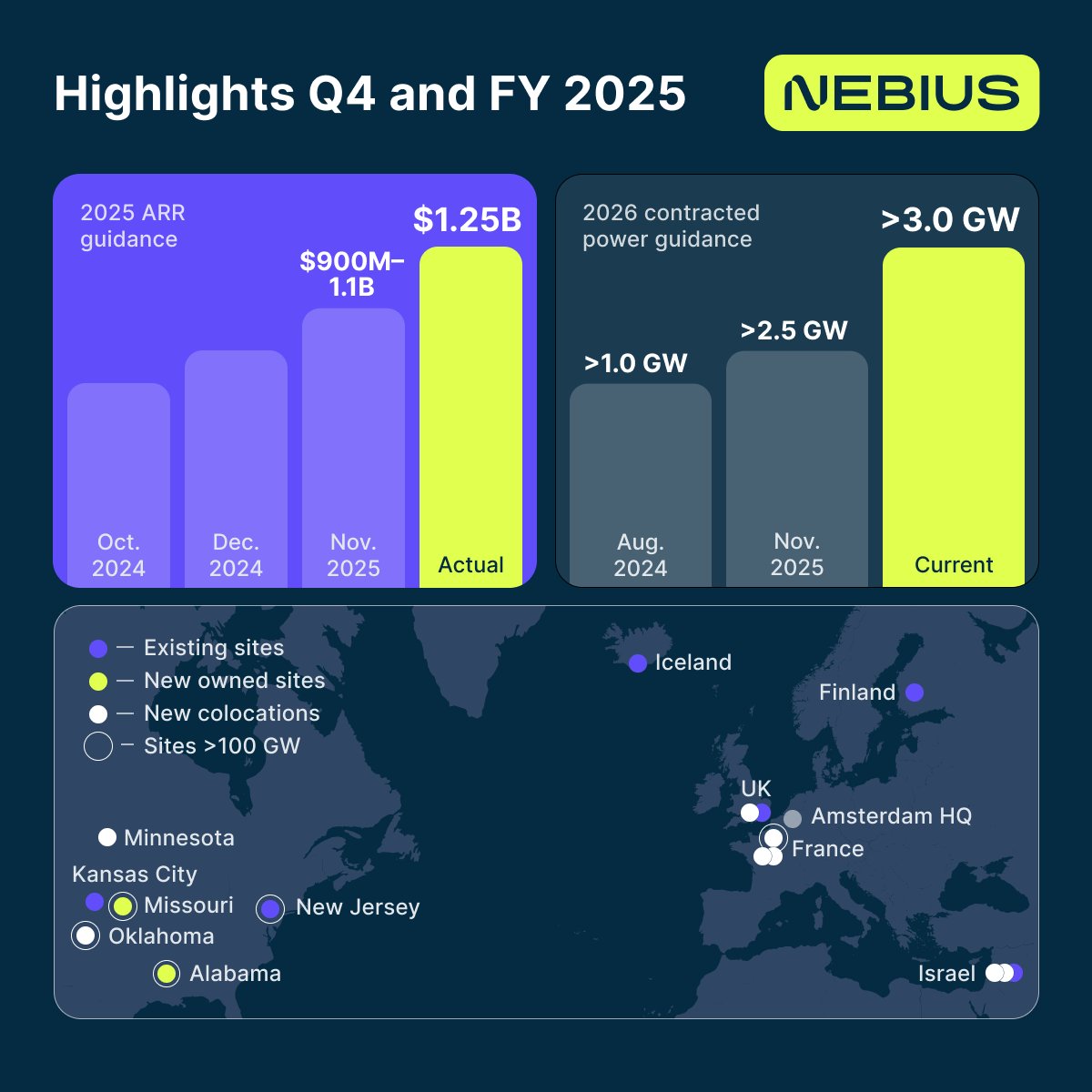

Today, we reported our Q4 and full-year 2025 financial results. The highlights include:

- ARR as of year-end was $1.25B, ahead of our most recent guidance of $900M–$1.1B

- This paves the way for significant continued growth. We are on track to end 2026 with ARR of $7B–$9B

@arv9293@StockSavvyShay Q4 guide: $985M mid, 35-36% op margin, $2.95 EPS.

Before OCS and CPO even "begin to kick in", Hurlston's words tonight.

Gross margin 47.9%. This isn't normalizing, it's accelerating.

What number in tonight's release supports the correction thesis?

Penser que la menace IA pour les SaaS se limite aux LLM grand public, c’est rater 80 % du sujet : le vrai choc vient des modèles intégrés aux produits et des LLM privés/open source branchés aux données des boîtes.

Autre erreur : croire qu’on est déjà au max des LLM. Compare juste le “Will Smith qui mange des spaghetti” de 2022 à aujourd’hui : on est passé du glitch immonde à la vidéo quasi réaliste en un prompt. On est encore très tôt dans la courbe.

https://t.co/PePS3sy6KW

@gabrelyanov The $NBIS community has been pretty healthy so far, focused on execution, MW ramp and capital structure.

We don’t need “bigger than Amazon” narratives.

If the thesis plays out, the upside is already huge.

Let’s keep it analytical.

You’re right. $160 is more a strategic milestone than a valuation ceiling. For me, it represents the first confirmation that “stage one” of the thesis has played out successfully, execution at scale validated, 2026 materially de-risked.

When I say I won’t sell before $160, it’s not about anchoring to a number. It’s about not front-running my own thesis.

At that point, I’ll reassess based on fundamentals, execution and forward risk/reward.

Price is a checkpoint. Thesis evolution is what will drive my allocation.

I genuinely enjoy researching other companies.

But today, I don’t see a better place to allocate my capital than $NBIS.

Added again at the open yesterday.

No intention of selling a single share before $160.

And even at $160, if it’s still the best risk/reward over the coming years, I’m fully comfortable staying 100% allocated.

Price is just a milestone. Thesis is everything.

100% $NBIS. High conviction. Thesis intact.

Now comes the hard part: waiting.

Capital concentrated. Curiosity, not so much.

So I’ve been quietly digging into a few names that caught my eye:

$KRKNF $LITE $ASTS $SATS $ONDS $EOSE

What’s your highest-conviction idea outside $NBIS?

Le Q4 m'a vraiment convaincu. La seule crainte possible était l'exécution, le fait qu'ils soient en avance me fait vraiment envisager l'année à venir extrêmement sereinement.

J'avais ciblé 160$ fin 2026 avant les résultats, je suis un peu plus haut à présent mais c’est surtout que ma conviction qu’ils puissent atteindre 160$ a nettement augmenté.