The Rupee Bled. FIIs Fled. Earnings Held. Now the Reversal Begins..

The Indian Rupee has collapsed from ₹83 → ₹96+ in just over a year.

Everyone blames FII selling.

That's lazy analysis.

There are 3 deep structural forces that killed the rupee — and they all hit simultaneously.

🥇 GOLD: Gold surged from ~$2,000 → $5,600/oz in 2 years. India didn't stop importing — we just paid 3x more dollars for the same metal.

India's gold import bill hit a record $71.98 billion in FY26, up 24% in value even as volumes fell 4.76%. To put that in context: our gold import bill was larger than India's entire defence budget. And what did the government do in 2024? Cut import duty from 15% → 6%. Imports exploded. Duty is now back at 15%.

The CAD damage is already done.

🛢️ OIL: Crude was at ~$60/barrel before the Iran-US conflict escalated. Oil moved to $115. India imports ~85% of its crude needs — every $10 rise adds $12–15 billion to the annual import bill.

But oil doesn't just hurt through imports.

It triggers a chain reaction: higher oil → higher inflation → RBI can't cut rates → growth slows → earnings disappoint → FIIs sell more. Oil is not just an energy story. It is the rupee story.

📉 FII SELLING: This isn't one bad quarter — it's been an 18-month relentless exodus. FY25 alone saw ₹1.27 lakh crore pulled out — the second largest annual outflow ever. Full year CY25 hit ₹1.6 lakh crore ($18 billion) — an all-time record. FY25 + H1 FY26 combined: over ₹3 lakh crore gone from Indian equities. FPI ownership in NSE-listed companies fell to 16.9% — the lowest in over 15 years.

Why? US tariffs, no US-India trade deal, global risk-off on AI/growth concerns, and China stimulus pulling EM money away. India didn't break. The risk-reward just shifted.

The combined damage: CAD for Apr–Dec 2025 stood at $30.1 billion (1.0% of GDP), with Q3FY26 alone at $13.2 billion as merchandise trade deficit widened to $93.6 billion.

And the dollar index (DXY) touching 97 added a brutal multiplier — a stronger dollar means every import costs even more in rupee terms, compounding the pain across gold, oil, and capital outflows simultaneously.

But here's where it gets interesting — the silver lining is forming.

☀️ Gold entering bear territory: After peaking at $5,600, gold has broken down technically. Gold is now trading around $4369 — caught below its 20/50/100-day SMAs, with the 200-day EMA at ~$4,380 acting as the critical bull/bear dividing line. A weekly close below that level would confirm a structural bear phase. Every $500 drop in gold directly saves India billions in forex outflows — this is one of the most important charts for the rupee right now.

⛽ Oil retreating despite the war: Crude has pulled back to ~$90 even with the Iran-US conflict ongoing. Markets are pricing in demand destruction over supply disruption. The dollar index has also slipped back to ~99, snapping its winning streak as ceasefire hopes emerged. If geopolitical de-escalation follows, sub-$80 crude is a meaningful tailwind for India's CAD.

🌏 AI trade reverting to mean = flows back to India: The global AI euphoria that sent capital rushing into US tech is showing signs of mean reversion. When that trade unwinds, emerging markets — especially India with its quality earnings and deep domestic consumption story — are the natural beneficiaries. Anti-AI = pro-India in global flow terms.

🏦 Game-changing policy moves this week: The government just exempted foreign investors from income tax on interest earnings and capital gains from government securities — effective April 1, 2026.

FPIs have already net bought ₹5,262 crore in April, ₹5,512 crore in May, and ₹3,395 crore in the first five days of June through the FAR route alone.

The RBI also expanded FAR eligibility to 15, 30, and 40-year G-secs, deepening the bond market structurally. Add the government's push on ease of doing business, capital market reforms, and increased FPI investment limits — the policy backdrop has shifted decisively in India's favour.

📊 Earnings: The foundation is already delivering: In Q4FY26, midcap earnings jumped 27% YoY and small-caps surged 37% — the Nifty-500's strongest earnings quarter in five quarters. Median operating profit for companies in the ₹500 cr–₹50,000 cr market cap bucket grew 14.1% YoY in Q3FY26. Q4FY26 numbers are continuing that trend. Yes, Q1FY27 will see some tariff and macro-related pressure — but the market has largely priced that in already. The earnings upcycle for Indian small and midcaps is quietly firing on all cylinders.

The bottom line: The same 3 forces that crushed the rupee are now either reversing or being actively countered by policy.

Gold is technically rolling over.

Oil is retreating.

Bond market reforms are unlocking fresh dollar inflows. FII equity flows have a credible catalyst to turn positive. Corporate India — especially in the mid and small cap space — is delivering earnings that the market is yet to fully price in.

The new bull market in India isn't a hope. It's already loading.

Samirji, for IT services, fewer people directly hits the per-hour billing revenue. But for product-based firms, wouldn't this create massive operating leverage? If a product is built and maintained by 40% fewer people, it’s a pure margin expansion story. Does your thesis see this as a bigger valuation re-rating trigger for products than services?

@SouMan2132@SureshKBN currently running on 80-90% capacity..new capacity should come online by 2027..dont see earning trigger..though valuation wise vey cheap..what your thesis for 5k?

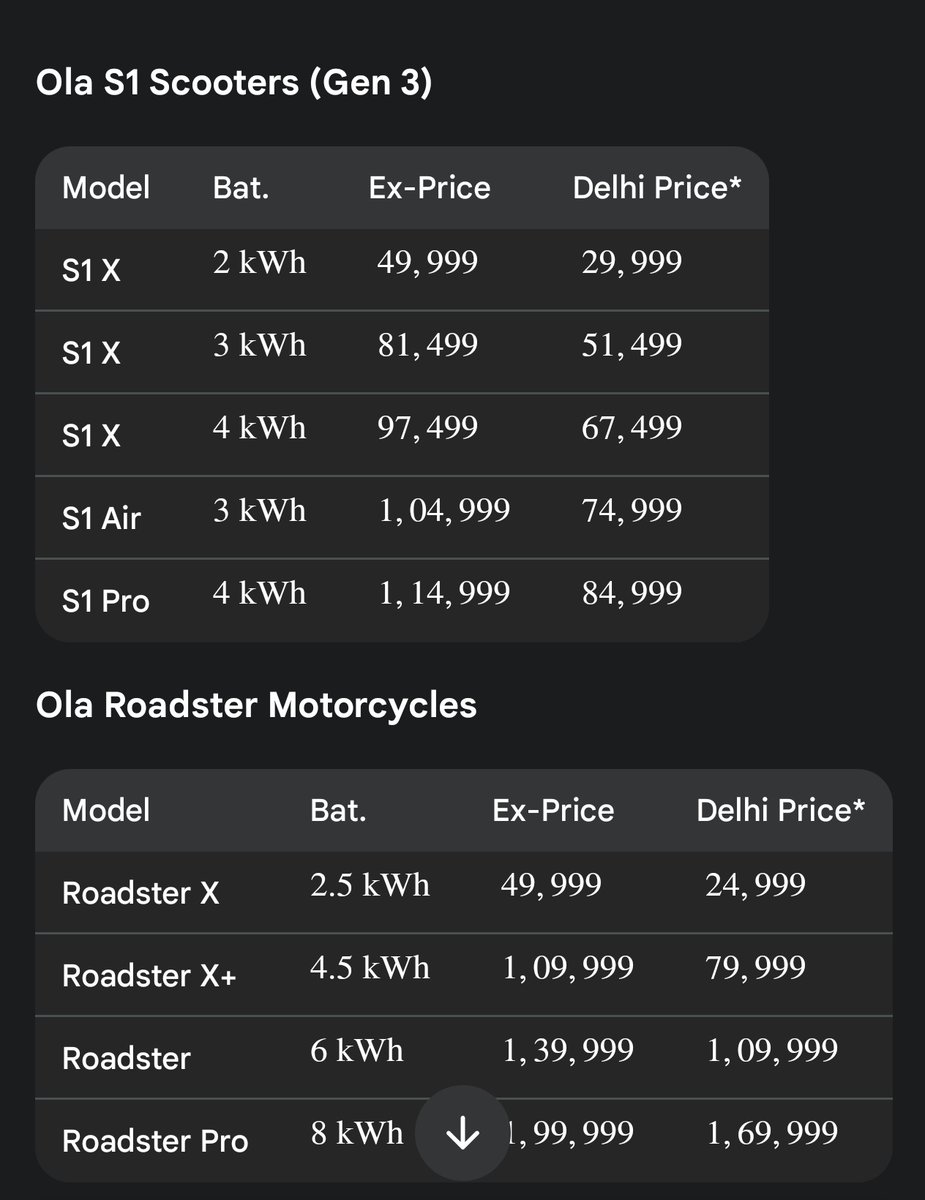

Delhi, the revolution just got real! ⚡️

The new EV policy is a total game-changer for every Delhiite. With @bhash leading the charge, you can now own an Ola for a price that feels like 'practically nothing'—starting as low as ₹29,999! 🤯

Cheaper than most smartphones, better for the planet. Time to #EndICEAge in the capital! 🇮🇳🚀

@bhash : can you confirm Are these prices for real for Delhietes?

#Ola #DelhiEVPolicy #ElectricRevolution #MissionElectric