Most Bitcoin holders think borrowing against BTC means handing it to a platform and getting dollars wired back.

That’s not what Cadena does.

And the difference is exactly why BlockFi and Celsius don’t exist anymore.

A thread🧵

Tom and his wife found the house after three years of looking. The offer had to be cash-competitive. They were $120,000 short.

They held Bitcoin. Enough to cover the gap, but the one asset they refused to sell right before the part of the cycle they’d been waiting for.

Selling meant a capital gains bill and giving up an asset at exactly the wrong moment.

As Kevin Bell explains, they didn’t have to choose.

On Cadena, Tom borrowed dollars against his Bitcoin through a DLC at 50% LTV.

Fixed cost, no margin calls, no platform custody. He repaid at maturity. His coins never moved.

They made the offer. They kept the Bitcoin.

Read Kevin’s full breakdown on LinkedIn

https://t.co/wuLq6Hj9wM

@hillery_dan The preferred-as-perpetual-income point is a Bitcoin-fixed-income point in disguise. As BTC-collateralized credit matures you get a genuine Bitcoin yield curve — that's what challenges the 60/40, not just price appreciation.

@Mulana_intern Strong framing — yield as paid risk transfer. The cleanest version keeps collateral non-custodial so the "yield" isn't quietly counterparty risk wearing a coupon. That's also the bar a Bitcoin fixed-income layer has to clear before it can stand in for the bond side of a 60/40.

The sequencing is right — yield was the on-ramp, digital credit is the product. What decides whether it lasts is collateral integrity: a Bitcoin credit market only earns a real yield curve if collateral is verifiably non-custodial and not rehypothecated. Otherwise digital credit inherits the Celsius failure mode.

@ZestProtocol@yzilabs@TimDraper@muneeb Good to see self-custody becoming the baseline for BTC lending — right direction. The next bar is no-liquidation / no-margin-call on top of self-custody, so a drawdown never forces a sale.

Exactly the problem with margin/custodial lending — a dip forces a sale at the worst time. The fix isn't avoiding BTC-backed credit, it's structuring it without liquidation or rehypothecation: keep your keys, lender can't call your collateral, a drawdown never ends with you selling the stack.

@GuruVerseX Directionally agree. The structural unlock isn't just removing the margin call — it's removing custody risk at the same time. Non-custodial + no rehypothecation is what makes the credit durable; otherwise you've just relocated the counterparty risk.

Live on Spaces 🇸🇻 — Talking through where Cadena Bitcoin is: mainnet-live, non-custodial, no margin calls.

Endgame Book launch and what's coming next (liquidity partner announcement? 👀)

Come with questions 👇https://t.co/p8FXvKwL5U

@Josico120 This is a Bitcoin-native product, base layer, no sidechains, no wrapped assets.

The self-custody piece isn’t a crypto philosophy, it’s a consequence of how DLCs work on Bitcoin L1.

Sziller said it plainly in Episode 20:

We are not your custodians.

Your Bitcoin. Your money. Your decision, full stop.

At Cadena, we don’t hold the keys. We don’t make the calls. That’s on you, the way it should be.

Watch the clip to hear it straight from our CTO.

@CyrptosSherlock Worth being precise: this isn’t about empowerment messaging.

The architecture physically can’t take custody. That’s a different thing than choosing not to.

A miner in West Texas is sitting on 40 BTC and a power contract that could support 3x his current hashrate.

The problem isn’t conviction. He has plenty

The problem is that scaling the operation means buying rigs and buying rigs means selling Bitcoin he doesn’t want to sell at the bottom of a cycle.

So he doesn’t scale. The opportunity sits there.

Here’s what the Cadena structure makes possible instead:

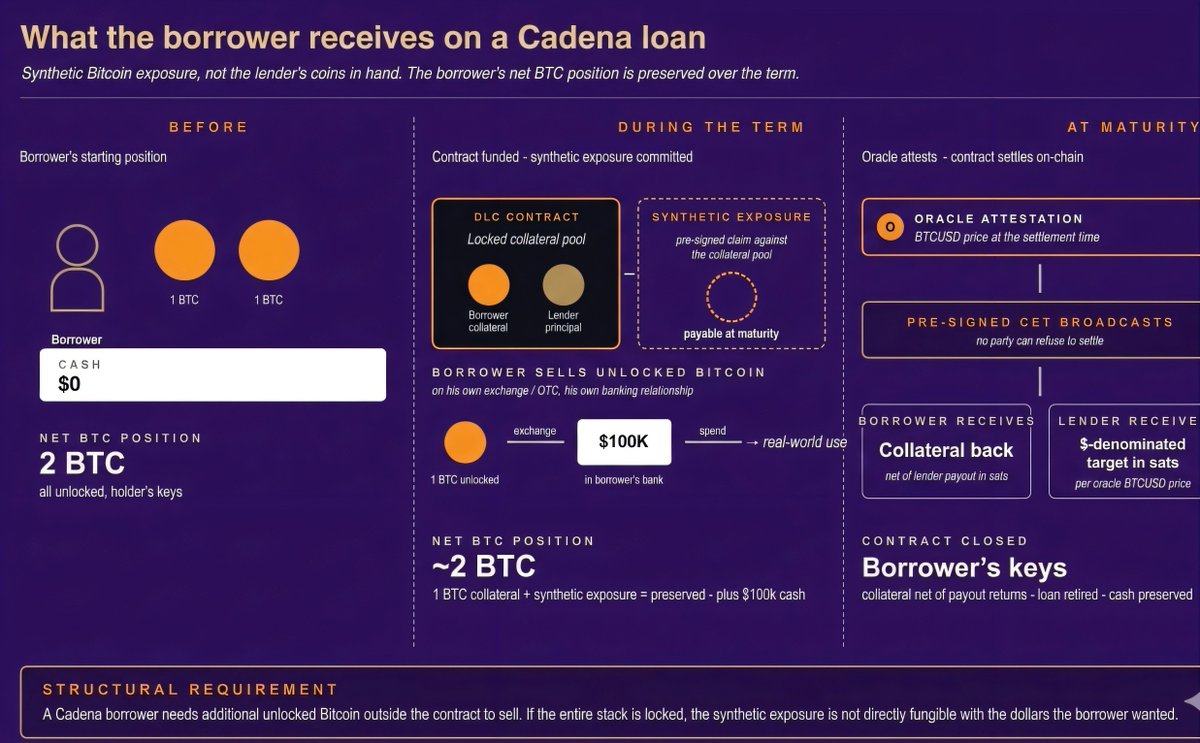

He locks a portion of his stack as collateral. He sells a separate portion on his own exchange for the capital he needs.

The synthetic exposure inside the contract preserves his total Bitcoin position over the term. He buys the rigs. The operation scales.

At settlement, his collateral returns and he’s running 3x the hashrate he was running before, without having permanently reduced his stack.

No margin calls mid-cycle. No custodian holding his Bitcoin. No bank asking what a DLC is.

That’s the Bitcoin Entrepreneur use case. Amplify the operation. Keep the stack.

If you’re a miner and you’ve run this math before, what’s been the actual blocker? DM us or reply here.

Amazing innovation. That 74% gap is the story. Custodial failure and liquidation anxiety is the biggest drivers. It's why we built Cadena around loans that can't be liquidated on a price wick, with you keeping custody of your keys the whole time. The fear is rational; the product design should answer it, great job.