Former Treasury Secretary Henry Paulson called on US authorities to prepare a back-up plan in order to avert a potential collapse in demand for Treasuries https://t.co/SljrcfTMjw

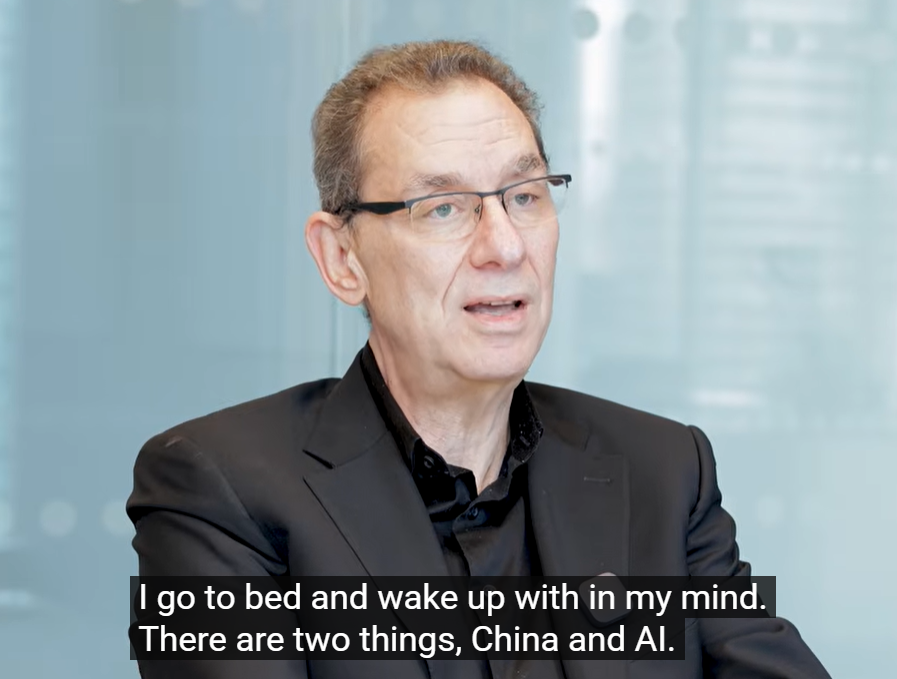

Pfizer CEO on the Norges interview, he goes to bed and wakes up with two things in his mind: "China and AI." common theme too with other pharma CEO interviews.

He said a few interesting things, below, and before you start screaming how much you dislike this guy (imagine thinking Greeks ever cared about being liked) just discount his message according to your bias.

For me, a lot of what he is saying is probably pumped on purpose to send a message to his regulators (wake up or China will eat our lunch). But still worth incorporating into your thinking.

1-In his view, Chinese pharma strength right now is in early stage (discovery, chemistry, testing, preclinical) "for every one area we have a company working on something novel the Chinese have ten companies working on it too" and on R&D productivity "they do things 3 times faster and at half the cost"

2-Another strength is the technical capability of the regulator, paraphrasing "they spent years copying the FDA, iterating, their process mirrors it, but is now faster, and with an ability to quickly distinguish garbage from diamonds" (the Novartis guy also mentioned something like this)

3-And final strength, most surprising for many: he says it is a great place to invest because of how they have developed a very strong IP protection system (imagine that) "the judiciary system can resolve IP issues very quickly, if someone challenges your patent you are not having uncertainty for 10 years"

4-He says Chinese pharma weakness is they still don't have global clinical development teams neither global commercialization teams. That is what makes all these licensing deals with global pharmas possible:

---usd200bn deals announced over the past couple of years, latest actually on Friday by Pfizer usd650m + usd10bn licensing deal with Innovent for 12 early stage oncology candidates

5-However, he thinks licensing is not a sustainable strategy for global pharmas, because at some point Chinese pharmas will stop selling their drugs to global players, and instead go to market themselves to keep the profit

6-So the only way long term is to be better than them, and that requires an exponential change to productivity, since the benchmark is the above "3 times faster, half the cost" (hint to the regulator there)

7-Finally after 30min of talking he decides to directly point at the regulator saying "stop spending 80% of your time and effort in slowing down China, because it is not going to work, and instead spend 80% of your time an effort in helping us accelerate"

Now, from an investing perspective:

8-There is a big mismatch between China biotech "insider vibes" from CEOs, industry participants, and commercial newsflow, vs share price performance

9-Innovent stock was up 11% on Friday on the back of the Pfizer deal, but has been rangebound for almost 1 year, and recently starting to break lower. Similar story with Beone or Akeso. Other China pharma bluechips like Hengrui are already down 30% (from big multiples true).

---On the fundamental front, Innovent and Beigene had 2025 as their first year of profitability, with top line growing at 40%. They trade at 10x 6x P/S respectively

10-Similar story around services, where only Wuxi Apptec is working, while XDC and Biologics are rangebound (despite XDC saying they are fully booked till 2030, almost as if they were making datacenter gas turbines), and tier two names like tigermed, pharmaron, joinn starting to break lower.

11-Medical equipment is even worse, from big guys like Mindray to smaller like Tofflon.

12-Even AI pharma pump names like Insilico are breaking (this company btw gives me forbes 40 under 40 vibes, though I confess I haven't bothered to look in detail, it may be a fantastic business, you tell me)

So, a lot of good stuff happening for people, new good cheaper drugs, not a lot of good stuff happening for investors. May be a global sector issue, may be a flow issue, which generalist in its right mind is selling Nvidia to buy Chinese pharmas.

Most of what you hear about the war in Iran is wishful thinking or American policymakers just talking to each other. Here's the true gen: Iran is suffering but the U.S. will suffer more. It's a game of chicken that Iran will win in the end.

https://t.co/pzhlvR0jn2

Silver miners relative to gold miners appear to be on the verge of a significant breakout.

It doesn’t take a mathematician to recognize what happens when a business is selling metal for $75/oz while production costs remain closer to $15–20/oz.

These are the strongest margins this industry has ever experienced.

https://t.co/S7emky0bKp

Mining companies today are generating the largest profit margins of any sector in the global economy by far.

Much of the market remains asleep and still analyzes mining through an outdated framework from decades ago.

To be clear:

Miners today are producing profit margins nearly double those of tech companies.

At current metal prices, this environment is absolute nirvana for well-run mining businesses.

https://t.co/rRpQ7qqZ5H

Welcome to the most asymmetric trade in modern financial history.

The thread below lays out why. The opportunity exists because capital has chased the AI trade while ignoring the physical assets AI requires to run — assets that have quietly become the best-performing asset class of the decade. Since October 2020 when we first called for the commodity super cycle: QCI Total Return +217%, GSCI Total Return +205%, Gold +140%. NASDAQ trails at +130%. S&P 500 at +85%. The top three are all commodities. Yet oil cannot get out of its own way while copper and the broader atom complex prints fresh highs . That is the dislocation. That is the trade.

Get long. Buckle in. Hang on for the ride.

Forgive the longer posts in this thread — attempting to mimic my old 10-bullet commodity takes. On to it.

The crew on @CNBCFastMoney all agree that now is the time to sell the gold miners. You can’t ask for a better buy signal. It bothered me that they were so bullish at the highs, so this capitulation is as good a contrarian indicator as you are likely to get. Buy with both hands!

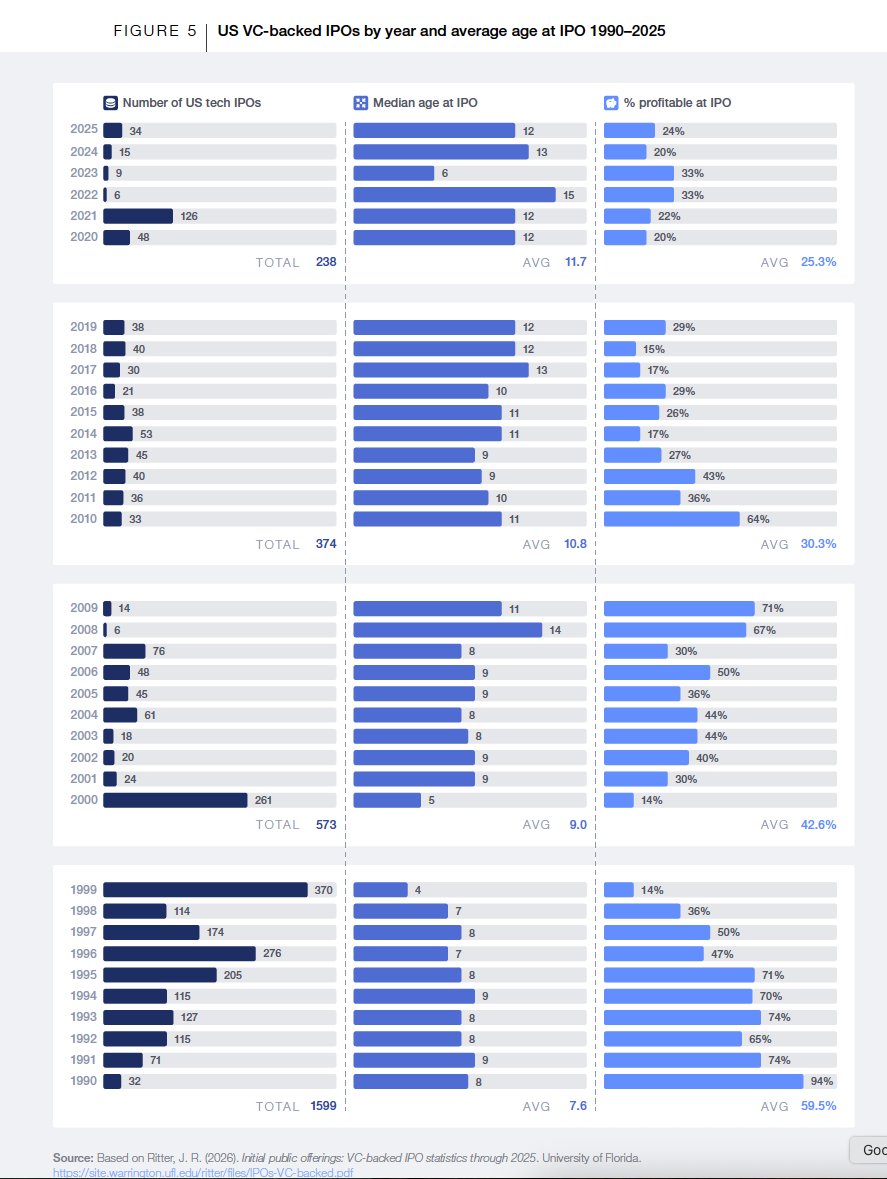

I feel like the conventional narrative is that all the IPOs from the 1990s were unprofitable and all the IPOs today are late stage profitable...

...but that's....backward? via @wef

https://t.co/HbhGB0CnvV

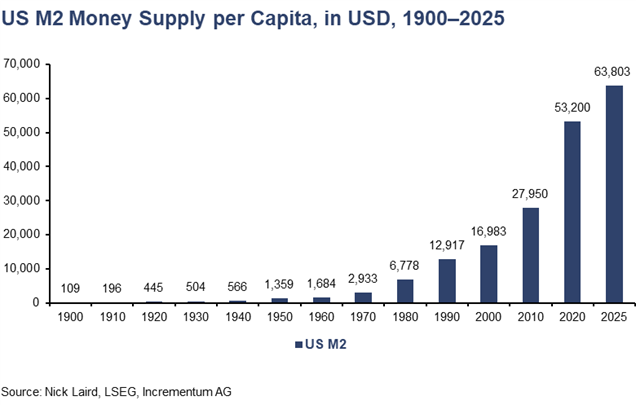

Since 1900, the US M2 money supply grew from 9billion to 23 trillion. On a per capita basis, this represents an increase of more than 540 times, from USD 118 to over USD 63,000....

#INFLATION