Part-time researcher and analyst. Value orientated. ASX focused. Turning over unusual stones. I do regular deep dives (see my pinned tweet) and company updates.

⚡️ “Index of Deep Dives”

Each week I try to do a deep dive on an #ASX stock that I am considering to buy, to add to my watch list, or to update my research on a stock in my watch list. Here is a list of recent deep dives compiled in one easy spot👇

https://t.co/6CEnYLjXLR

Overall, a higher price and some competitive bidding would be nice, but current value unfortunately is probably 'fair'.

If you enjoyed this, bash the like / retweet / follow buttons.

Questions and feedback always welcome. DYOR.

Disclaimer, I'm long GNX.

To be honest, ever since Skip's bid fell through and Genex have needed to finance the pipeline of projects themselves, they've been advertising themselves as a takeover target. No surprises.

@IllistromEmpire J-Power already owns an equity stake and substantial project stake, so as an insider, less likely to pull out following. Management will sell and take ongoing corporate role probably. Just reckon the time for M&A in long duration renewables seems pretty solid..

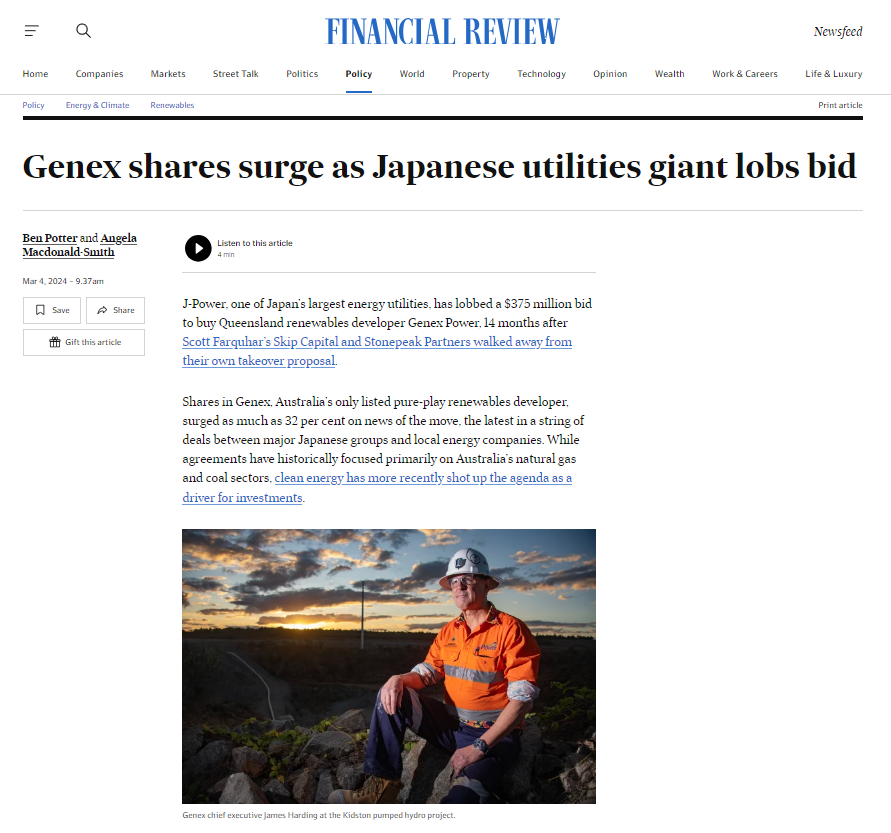

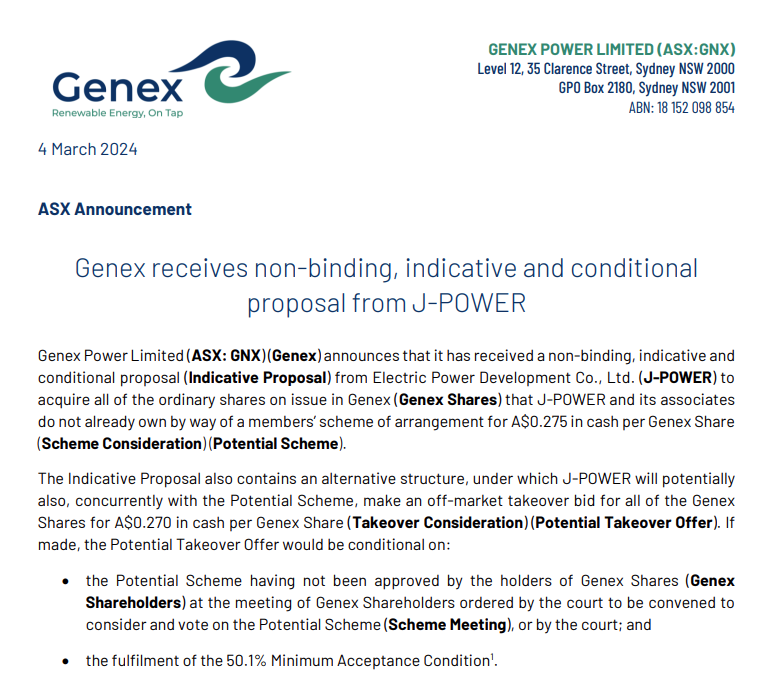

Genex $GNX $GNX.AX get's another takeover bid, at a 2c premium to Skip back in 2022 which fell through when rates went up. This time I reckon J-Power and the Board will get the job done, with 27.5c being around fair value imho. 🥳

https://t.co/YON8bLqD9Q

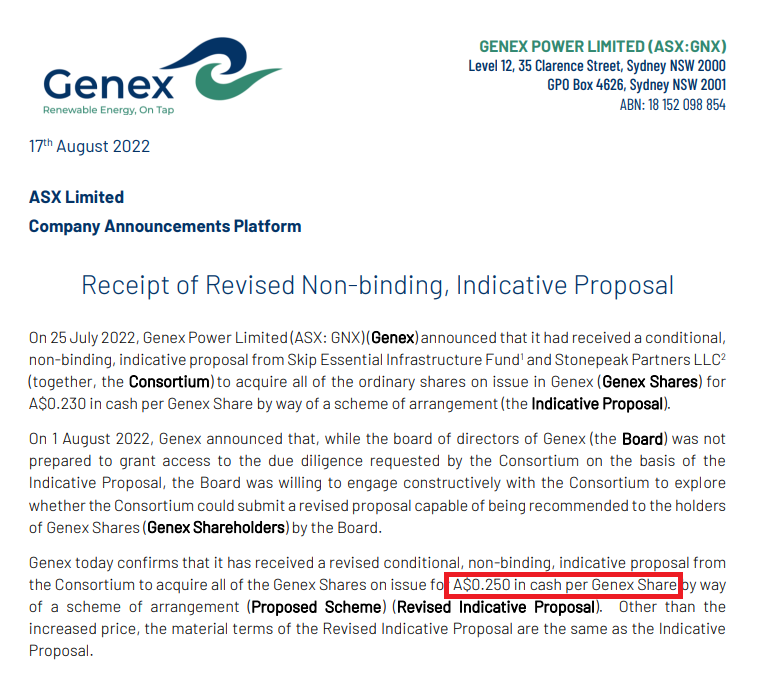

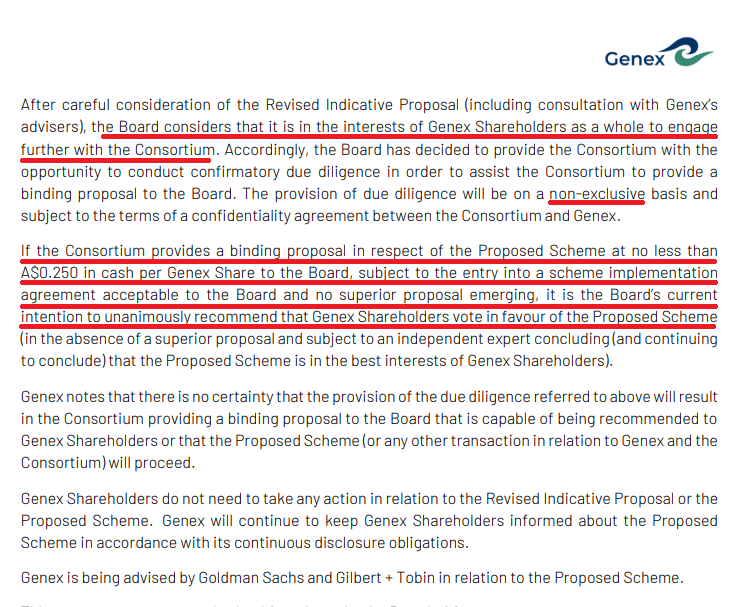

Genex $GNX $GNX.AX has received a +8.6% bid from Skip at 25c per share. But, the board rightfully is saying that is not enough. You can see our books on a non-exclusive arrangement, but we're sending out Goldman Sachs to go fishing for more.

Crack out the popcorn 🤓🍿

@neke86_ With all those de-risking events, and their pipeline stuffed to the gills but insufficient capital to finance them, no wonder J-Power is getting in on the action. Good one! 🤓🍿

@RonShamgar Not so black and white in my opionion. Earnings per share down after the cap raise / dilution / acquisiton. $8m wrote down in amortisation on that acquisition didn't help the results either. Still, a decent operating performance.

(Held)

@TheFinCurator@Mathan_Soma I don't believe so. They have stages of capital investment and conversion to orchards, so there is some risk and sunk costs there if that doesn't eventuate.

Rural Funds $RFF $RFF.AX with a strong update; asset evaluations up significantly led by their once-maligned macadamia. NAV up from $2.93 to north of $3.14, trading at $2.15. 🥜 💪

@neke86_ @Mathan_Soma You can fade some of the valuation of plants in the ground particularly almonds, and cattle stations perhaps because they're post peak prices now.. but by and large, yep. But a 35% discount to NAV is very high historically for RFF.

@TheFinCurator@Mathan_Soma I don't know reallyy. They don't sell the macadamias, they lease the land they're grown on. Increasing valuations drives up their rental yields (based on CAPEX and a combination of CPI and valuations) and lowers their gearing, so both your concerns getting, well, less concerning.

@Mathan_Soma Good choice. Confirmation bias here, but it was my pick for 2024.

I hope we will see AFFO exceed dividends this year, a rerate of macadamias, and the NAV discount diminish substantially. 🤔

@berthon_jones Yep, lots of change. The Lebanese place opposite Crescat is quite good. But I am old school and often end up back at Gallery for their curries.