Luca’s model for onchain lending is rigorous and the framework is genuinely novel. However, we have two disagreements with it:

1. Onchain lending is repo not a put option sale

2. If you use a more realistic LGD parameter, the model predicts observed lending rates without significant mispricing

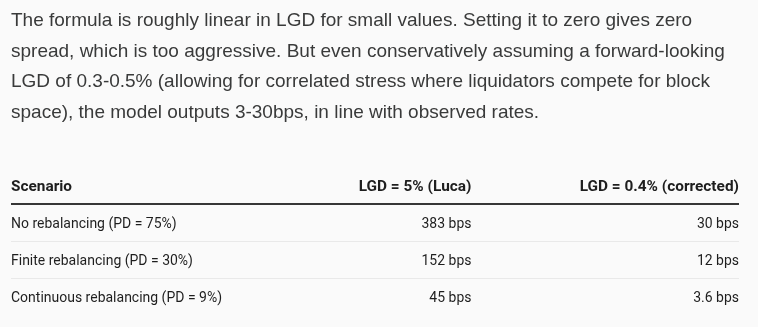

The model relies on a loss-given-default (LGD) parameter to estimate the fair value of an onchain lending position. We would set the LGD parameter to a few bps over 0% (higher than the empirical bad debt rate for lenders in Prime markets) rather than ~5% (which is modeled on the liquidation incentive, a borrower cost).

If you do, the model outputs fall exactly in line with observed rates at around 3-30bps, and the alleged mispricing disappears.

We acknowledge @ChaosLabs' sudden announcement to step down from their @Aave risk mandate.

LlamaRisk has served the Aave ecosystem for the past two years, delivering risk frameworks, parametrization, and quantitative models underpinning all Aave deployments across V3, V4, and Horizon.

We build protocol-owned risk infrastructure on @Chainlink's CRE and serve as the only independent legal and regulatory research capability within the Protocol.

Aave's risk management has never rested on a single point of responsibility. We are fully prepared to fill all operational gaps and will ensure full continuity of risk services.

Over the next week, we will present a detailed proposal, including immediate changes to delegated risk systems, to renew our unwavering commitment to the Aave ecosystem. Aave will win!

Ethena's latest blog flags commodity & equity perps as a basis trade opportunity for USDe, expanding from just arbing crypto.

Gold perp funding on Binance averaged 15%+ from Dec to Mar, with silver funding being even higher. Meanwhile, BTC and ETH funding went negative.

We modeled what happens if Ethena allocates 10-20% of its USDe backing into commodity & equity delta-neutral basis trades. At ~11% funding (conservative), sUSDe yield goes from 3.6% to 4.3-5.0% and revenue jumps $41-83M. That would significantly improve Ethena's P/F, from 3.3x up to 2.5x. It's worth mentioning that the allocation percentage would probably start out significantly lower, as the roll-out will be in controlled phases. That said, based on HIP-3's rapid growth, we think the baseline estimate of a 10% allocation is a sensible target by EOY.

More numbers and charts below.

$ENA

Desde Aureo nos orgullece presentar: Direct to Wallet (D2W)!

La forma más fácil y revolucionaria de comprar Bitcoin en México 🇲🇽

D2W es la forma más rápida y sencilla en México de comprar Bitcoin con SPEI de forma auto-custodiada.

Solo envía una transacción y, listo recíbelo directo en tu billetera.

@gustavojfe explica cómo funciona y por qué lo primero que construimos fue que tu Bitcoin sea tuyo desde el minuto uno 👇

Tu Bitcoin. Desde el minuto uno. ₿

¿Más info?, lee nuestro thread 👇🏻🧵

POST-MORTEM: The "Andes-to-Alpha" Blowup

Date: February 6, 2026

Subject: Liquidation Event – "Victoria Peak" Capital (HK)

Desk: Exotic/Macro RV

We are receiving confirmation of a catastrophic unwind involving a prominent Hong Kong-based volatility desk this morning. The dust is still settling, but the anatomy of the blowup appears to be a classic case of correlation breakdown meets illiquidity.

Here is the breakdown of the $450M implosion that just hit the tape.

1. The "Genius" RV Setup

The fund, which we’ll call "Victoria Peak" for anonymity, was running a highly levered Relative Value (RV) book designed to harvest yield from disconnected emerging market betas.

• Short Leg: Colombian Biotech basket (illiquid, sensitive to localized regulatory/drug-approval news).

• Long Leg: Bitcoin via IBIT (BlackRock ETF) Spread Options.

• The Thesis: They were betting on a "Risk-On" global environment where crypto beta (IBIT) would outpace obscure LATAM healthcare (Colombian Bio), effectively hedging the crypto volatility with the biotech short.

2. The Exogenous Shock: The TIA/EIGEN Collapse

The structural flaw wasn't in the main legs, but in the collateral management. The fund was using a basket of "Modular Blockchain" assets as cross-margin collateral.

• Specifically, they were heavily exposed to the TIA/EIGEN ratio (Celestia vs. EigenLayer).

• The Event: A governance fork rumor caused TIA to nosedive while EIGEN stayed bid. The ratio collapsed -34% in 4 hours.

• This vaporized their collateral buffer. Because the Colombian Biotech market is so thin, they couldn't cover the short without pushing the price against themselves.

3. The Contagion: Puking the Macro Book

With the crypto-collateral worthless and the Prime Broker (PB) issuing an immediate margin call, Victoria Peak had to liquidate their only liquid assets to stay alive.

• The Victim: Their macro hedge book—Long KRW / Short Copper.

• Usually a play on Asian industrial manufacturing slowing down, this was their safe haven.

• They were forced to panic-sell KRW and buy back Copper futures at market execution. This caused a temporary 40-pip dislocation in USDKRW spot markets and a random spike in COMEX Copper.

4. The Kill Shot: Enter Cyant Arb

The market smelled blood, but one desk acted fastest. Cyant Arb, a notoriously aggressive proprietary trading firm known for predatory liquidity provision, identified the distress flows immediately.

• Cyant’s algos detected the correlation break between the TIA liquidation and the forced KRW selling.

• They widened spreads on the IBIT options and stepped away from the bid on the Biotech stocks, trapping Victoria Peak in a liquidity vacuum.

• The Liquidation: Cyant eventually stepped in to act as the counterparty of last resort, buying the fund's KRW/Copper bags at a massive discount while simultaneously squeezing them out of the IBIT options.

Result: Victoria Peak is effectively flat (and arguably insolvent). Cyant Arb booked an estimated +18% PnL on the session.

In anticipation of the Labs' proposal next week, we will be recapping the $AAVE drama from early December.

AAVE recently went through a governance standoff over $10M/year in frontend fees. 41% of voters abstained in protest. Labs responded with a revenue sharing commitment, but the details aren't finalized yet.

On Dec 4, Aave Labs swapped the default frontend provider from ParaSwap to $COW Swap. Fees (~15-25 bps) that previously routed to the DAO Treasury started flowing to a Labs controlled wallet (est. value: $10M/year).

A week later, delegate EzR3aL caught this onchain and posted findings to the governance forum. Marc Zeller (Aave Chan Initiative) called it 'Stealth Privatization'. The DAO had funded frontend development through Service Provider Grants, though Labs argued aave(dot)com is a private product.

Things escalated quickly. Former CTO Ernesto Boado posted a proposal requesting Labs transfer all IP - domain, trademark, socials to a DAO controlled entity. Stani then pushed it to Snapshot himself, scheduled over Christmas, without Boado's consent. AAVE dropped ~20% during the week.

As voting opened, Stani bought ~$15M in AAVE on the open market to signal token alignment. Wintermute voted NO, citing poorly defined terms. Zeller rallied delegates to vote ABSTAIN. The goal wasn't to win, but to delegitimize the process.

Final tally (Dec 26):

• NAY: 55.29%

• ABSTAIN: 41.21%

• YEA: 3.5%

• Turnout: 1.8M AAVE (record)

On Jan 2, Stani posted ‘Aave 2030’ - an olive branch :

• Revenue sharing from off protocol sources with stakers

• Legal guardrails giving DAO some rights over the brand

• Labs keeps IP ownership

Price bounced 5% vs the broader market due to tamed expectations.

Where it stands now: The commitment is there, but the terms aren't. ACI wants hardcoded smart contract enforcement, not just a promise. We're still waiting on Labs' formal proposal. A 50/50 split is the line in the sand used for Horizon RWA revenues.

The market is waiting on this proposal to pick a direction: will AAVE slowly downgrade to a pure governance token, or will it reinforce revenue accrual?

Follow @credo__v, we'll cover it when it drops.

A lighter summary is coming soon, plus details on putting these recommendations into practice.

For those who are quantitatively inclined, we hope you enjoy the full paper and please reach out with any feedback or comments.

Full paper: https://t.co/Kd261FPnxZ

Trump backed American Bitcoin $ABTC increases its $BTC holdings to 5,044 BTC.

$JPM launches $100M tokenized money market fund, MONY, on $ETH for subscription via cash or $USDC.

Pyth network introduces $PYTH reserve to boost network value with monthly token purchases using protocol revenue.