🟠 AI isn’t just code — it’s becoming an industrial system.

Datacenters now use ~2 % of the world’s power and billions of gallons of water.

By 2030, usage could double, reshaping who really wins the AI race.

In my latest FOCUS, I look at:

- Why the next AI moats are power, land & water

- How hyperscalers like Microsoft & Google are driving resource demand

- Where investors might find opportunity in grids, cooling, REITs & ETFs

👉 Read here:

https://t.co/fc6AzW3e1j

🟠Something big is happening in Shanghai — gold warrants on the Shanghai Futures Exchange are up 25x since January.

For context: a gold warrant is basically a digital claim on a bar of physical gold stored in an SHFE-approved vault. It’s what traders use to take delivery against futures contracts. Each warrant represents 3,000 grams of gold — and demand for them has exploded.

Why? Because China is quietly remonetizing gold.

Central banks — led by the PBoC — are stacking at record pace. Investors are rushing for safe havens. And with price volatility and tariff uncertainty shaking global markets, Chinese traders are increasingly turning to gold as both hedge and liquidity tool.

Shanghai is becoming the physical heart of global gold trade. In China, it’s becoming money again.

🟠Here’s a striking one: U.S. oil production keeps rising even as rig counts keep falling.

Rig activity (green line) has been sliding for months, yet output (red line) keeps inching higher.

Fewer rigs, better tech, more output per well. The U.S. shale patch has turned into a productivity machine.

And politically, this is exactly what Trump wants:

- Keep oil prices low → tame inflation → give the Fed more room to cut rates.

- Crank up production → strengthen the U.S. trade balance.

- Squeeze Russia → cheap oil hits Moscow’s revenue.

High output, low prices — it’s the holy trinity of energy, geopolitics, and monetary comfort.

🟠 China’s deflation loop deepens.

September CPI fell –0.3% year-on-year, and producer prices dropped –2.3%, marking yet another month where both consumer and industrial prices are shrinking.

The government keeps trying to pump up spending, but households are saving, property’s still shaky, and companies are cutting prices.

🟠Remember when Japan and China basically were the U.S. bond market? Back in the 2000s, they owned almost two-thirds of all foreign-held Treasuries. Japan alone held nearly 40%, China another 29%.

In mid-2025: Japan’s down to 13%, China to 8%. Together, they now make up just a fifth of what foreigners hold. That’s a massive shift… and it says a lot about how global finance is changing.

Japan’s story is simple: the yen crashed to its weakest level in decades (~160 per dollar), so Tokyo had to dump Treasuries to buy yen and defend the currency. China’s move is more strategic: it’s not trying to crash the dollar — just making sure it’s not too dependent on a system the U.S. controls.

Foreigners used to finance over half of America’s debt back in 2008. Today, it’s under 30%.

So no, the dollar isn’t dying. But the world’s clearly saying: we’d rather not keep all our savings in Treasuries. And that means the next big buyer of U.S. debt… is probably the U.S. itself.

Source: https://t.co/kVJFiPUqmj

🟠Subprime auto loan delinquencies just hit record highs, now topping 6% of total loans, according to Fitch. Car loans used to be the safest corner of consumer credit. People would skip credit cards or even rent before missing a car payment — you need the car to get to work, right?

Not anymore.

Lower-income households are under stress.

And as always in credit… if you spot one cockroach, there are probably more behind the wall.

🟠 In short: tariffs are inflationary just not instantly

A new Harvard-led study tracking U.S. tariffs in real time gives investors a clearer picture of how trade wars hit prices and it’s not as explosive as feared.

Here’s the takeaways:

Despite a wave of new tariffs in 2025, retail prices rose only 4–5% for imports and about 2% for domestic goods, according to high-frequency data from five major U.S. retailers. That’s far below the headline tariff rates — proof that pass-through remains partial and slow.

Still, the market signals are telling:

China’s exports saw the biggest jumps in prices (+4–5%), followed by Canada and Turkey.

U.S. goods in the same categories also rose, showing how tariffs ripple through domestic supply chains.

The pressure was strongest in household and furnishing goods, a China-heavy import segment.

In short: tariffs are inflationary — just not instantly. Retailers absorb part of the shock, but as inventories turn and uncertainty lingers, costs creep into prices.

This means inflation could prove stickier than models imply, especially if trade tensions persist. Supply chains may adjust, but not overnight — and “slow burn” inflation can keep real yields elevated and central banks cautious.

(Source: Cavallo, Llamas & Vazquez — “Tracking the Short-Run Price Impact of U.S. Tariffs”, Harvard Business School Pricing Lab, 2025)

🟠TSMC just smashed expectations — again.

Third-quarter profit jumped +39% year-on-year, hitting another record as AI chip demand keeps roaring.

- Revenue: NT$989.9B vs NT$977.5B expected

- Net income: NT$452.3B vs NT$417.7B expected

- AI & HPC chips = 57% of sales

- Advanced nodes (≤7nm) = 74% of total wafer revenue

CEO C.C. Wei said it plainly: “Our conviction in the AI mega trend is strengthening.”

TSMC now expects 2025 growth in the mid-30% range — up from 30% before — and raised its annual capex floor to $40B.

What’s driving it? Explosive orders from Nvidia, Apple, and other AI GPU makers, plus tight utilization of its 3nm and 5nm lines.

Tariffs and trade politics are a headache, but not a showstopper — TSMC’s U.S. expansion helps cushion that risk.

Shares are already up +38% this year, and this quarter just added more fuel. AI isn’t just a story for the future anymore — it’s showing up in earnings.

🟠The Fed’s so-called “tightening” isn’t as tough as it looks.

This chart shows it clearly: they haven’t really touched long-term Treasuries (red line). Those holdings are still near record highs.

All the real “QT” action happened in short-term bonds (blue line). Basically, the Fed’s been draining liquidity, but doing it carefully, making sure nothing breaks.

They’re keeping a safety net under long-term debt to avoid a rate spike and a market mess.

So yeah, the Fed were tightening…. loosely.

🟠The IMF just upgraded its global outlook and the U.S. is doing the heavy lifting.

Thanks to a massive AI-driven investment surge, America’s economy is now expected to grow 2% in 2025 and 2.1% in 2026, far outpacing every other G7 country. Global growth should hold around 3.2% this year.

The same AI boom keeping growth alive is also stoking inflation. As IMF chief economist Pierre-Olivier Gourinchas put it, people “feel richer because equities are high,” but productivity hasn’t caught up — it’s wealth on paper.

The U.S. economy isn’t cooling, it’s doped by AI.

🟠ASML Calms the Market but Warns on China

ASML eased investor nerves this week, saying 2026 sales should at least match 2025, despite fears of a slowdown. The stock jumped +3%, now +24% YTD.

The company still expects +15% growth in 2025 and solid 52% margins, powered by the AI boom — €5.4 billion in new orders last quarter.

But there’s trouble ahead: sales in China are set to drop sharply next year as U.S. restrictions bite.

Net sales: 7.516 billion euros vs 7.79 billion euros expected

Net profit: 2.125 billion euros vs 2.11 billion euros expected

So, no meltdown, just a pause. 2026 might be a breather before the next leg of the chip cycle or the start of a tougher climb.

🟠 This is how the next industrial era begins, not with trade deals or tariffs, but with industrial efficiency.

China now installs more industrial robots each year than the rest of the world combined, and its robot density — robots per 10,000 workers — has overtaken the U.S., Germany, and even Japan.

China is moving from labor advantage to productivity and precision dominance, fusing robotics, AI, and state-backed industrial policy into one unstoppable machine.

🟠Wall Street Just Put on a Show

The big banks just posted strong across-the-board results, with consumers holding up surprisingly well, dealmaking returning, and trading desks firing on all cylinders.

- JPMorgan kicked things off with a 12% profit jump to $14.4B, powered by record trading revenues (~$9B) and a rebound in investment banking fees (+16%). Jamie Dimon said every division “performed well,” though loan losses are inching up to pre-COVID levels.

- Goldman Sachs had an even bigger rebound — profits up 37%, led by a 43% jump in investment banking revenues and strong fixed-income trading. M&A and IPO pipelines are finally reopening, and it shows.

- Citigroup delivered 16% earnings growth, with trading and investment banking both up double digits. Wells Fargo beat expectations too, thanks to a 32% boost in investment banking and a healthier consumer loan book.

- Meanwhile, BlackRock quietly hit a record $13.5 trillion in AUM, with $205B in new inflows — most of it into ETFs and fixed income products.

And despite rising rates and sticky inflation, consumer credit remains stable. JPMorgan, Citi, and Wells Fargo all reported credit metrics better than expected.

Wall Street’s biggest names are showing strength on every front: trading, banking, and consumer finance. The economy might be late-cycle, but the banks aren’t blinking yet.

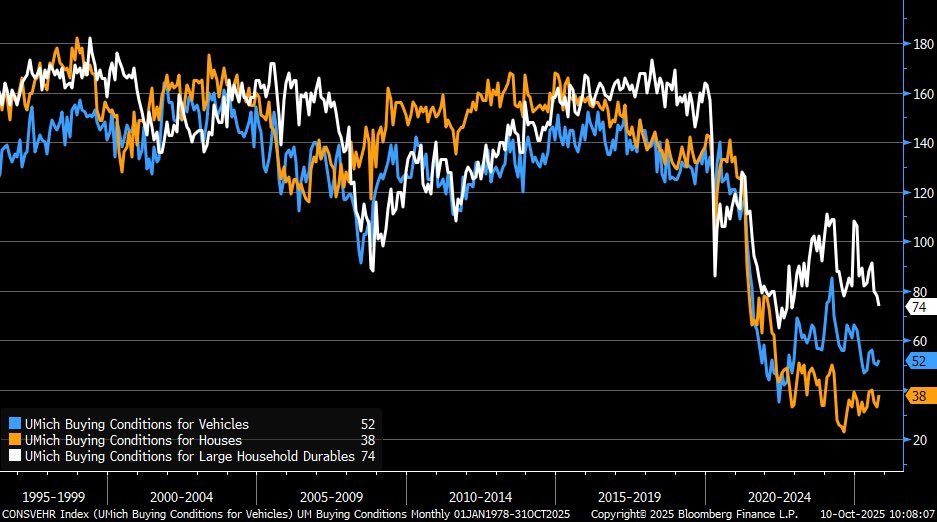

🟠Americans aren’t buying big-ticket items.

According to the latest University of Michigan survey, buying conditions for homes, cars, and household goods have all fallen to record lows.

Mortgage rates above 6%, flat real incomes, and tight credit are straining consumers — and it’s now showing up in spending data.

When even durable goods take a hit, it’s a clear sign: the U.S. consumer, long the engine of growth, is running out of fuel.

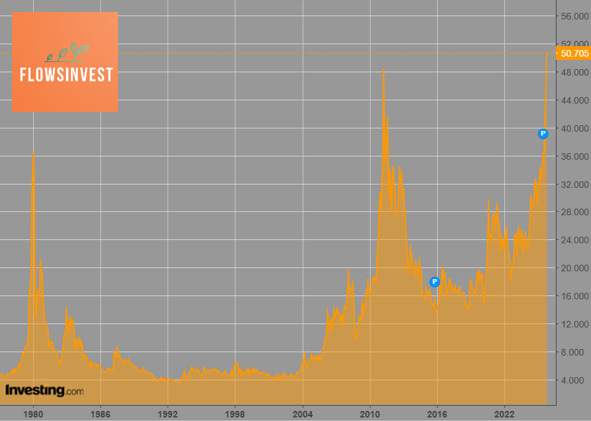

🟠Silver just broke records — $53/oz, up 85% this year, outpacing gold.

A mix of investor frenzy, industrial demand, and a physical shortage in London so severe that traders are flying silver across the Atlantic to fill gaps.

With inventories near historic lows, premiums have surged — and unlike gold, silver has no central bank backstop.

The last time silver moved like this was 1980.

🟠The Weekly Market Pulse #20 is out!

Powell’s flying blind, Trump’s back on tariffs, and gold just broke $4,000.

This week: the shutdown silences data, gold hits a record, and Trump reignites the trade war... for 48 hours.

I broke it all down — from Oracle’s AI margins to Europe’s auto slump — in this week’s Weekly Market Pulse #20.

Read it here: https://t.co/tFJz1hyf6Q

🟠Bond investors are demanding ever-higher real yields to hold developed-nation debt, as instability in France and Japan shakes confidence in fiscal discipline.

Across Europe, real yields on long-dated bonds (German 25-year, French 30-year, UK 30-year) are now sitting at multi-year highs.

Markets are starting to price in the risk that governments (not central banks) might be the ones who lose control next.