Interesting. the drilling season will be very exciting for both juniors. One is about 6x cheaper than the other with arguably the more attractive location (based on MMG's discoveries metres away from it). #ARCM $LVX #KCB

Very relevant for #ARCM - Arc is about 2 months from drill start. Our license much closer to Mawana Fold and Z9 (T1 discoveries) plus more evidence of Cu. They’re up 40% and Mcap of £83m…

Just look at these maps. We are ”priority” to MMG.

Botswana up n coming.

$UTHR has been trading around 7x sales for a while now.

no legal overhand would mean $LQDA should also trade at 7x sales minimum. Could argue for a higher multiple based on the growth and market share gains shown by LQDA. it seems totally reasonable to expect 1.2bn+ sales in 2027. At 7x Rev, that implies a share price of $105. 8x Rev = SP of $120.

So i think a legal win or <10% royalty would open the door to $120 share price by year end.

Atlantic Lithium taken over by Huayou Cobalt at 18.8p per share.

Not surprised but the price seems low, considering Assore (largest shareholder at 26%) were happy to pay c.30p at similar spod prices, before permitting. They kept buying blocks at 25p.

The statement suggests that Assore is open to higher offers. Maybe CATL ? #ALL #A11 #AtlanticLithium

Atlantic Lithium is pleased to announce it has entered into a binding Scheme Implementation Deed with Zhejiang Huayou Cobalt Co., Limited ("Huayou"), under which it is proposed that Huayou will acquire all of the issued shares in Atlantic Lithium by way of an Australian scheme of arrangement.

Read in full: https://t.co/uORoNui52X.

#ALL #A11 $A11 #ALLGH #Lithium #Ghana #Mining

If Mr Friedland is correct, and that the DRC is struggling to get sulphuric acid for copper oxide ore processing, then the Manono North lithium sulphate plant that is meant to start producing this year could be in a bit of trouble also.

Converting spodumene concentrate to lithium sulphate can use a broadly similar amount of sulphuric acid per tonne of final product, as processing copper oxide ore to copper.

If they can't produce a sulphate intermediate product, they will need to transport spodumene concentrate. Sulphate contains ~5x the amount of lithium in say SC5.2. Transportation costs will be significant given the location of the mine.

Could be one of the many reasons as to why the price of spodumene is running?

According to CNN, based on satellite imagery, while the airstrikes have struck 77% of tunnel entrances to underground missile launch facilities, within 48 hours most are reopened by digging out blocked entrances.

https://t.co/RL6jvDXM34

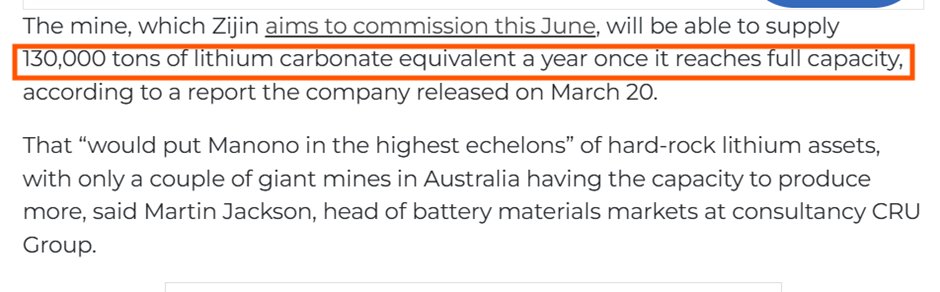

Saw this article today on the Manono North Deposit and just couldn’t help myself but to make comment. I'll also give my opinion on the deposit as I've had a few people ask for it.

Firstly, the deposit was stolen from AVZ shareholders. I hope AVZ holders get what they deserve for this deposit and it's absolutely pathetic by the Australian government to sit idle. Lots of hard earned Aussie dollars were put into exploring and developing the orebody and the government stays silent? This orebody needed to stay under the one company in order for it to achieve its maximum potential.

Zijin gained control of what is now known as Manono North which predominantly consists of the The Carriere de l’Este Pegmatite, often referenced as the CDL Pegmatite. I do think it's the inferior part of the orebody. It's lower grade than the Roche Dure Pegmatite (not in Zijin's control and to the south) and from an early stage, it seems its metallurgy wont be as good.

Personally I think splitting the deposit up was also a technical mistake. I think it was important from a metallurgy point of view to keep the both the north and south together.

The article states that the Manono North mine will produce up to 130,000 tonnes of LCE per year. I’d argue it won’t be anywhere even close to this.

40.4/(0.82*6) = 8.2 tonnes of SC6 per tonne of LCE.

130,000 * 8.2 = 1.06 million tonnes of SC6.

6/(1.58*0.7) = 5.43 tonnes of 1.58% ore needed per tonne of SC6. I’ve used a very generous recovery rate of 70% and you’ll see why it's generous later.

1.06million tonnes * 5.43 = 5.75Mtpa

This seems doable but the problem is, I don’t think Manono North is going to produce SC6 looking at historical met work and its grade. I think Manono will join the same club as LTR, PLS, MIN, in terms of recoveries. It’s not Greenbushes. I think it will produce somewhere around SC5.2.

40.4/(0.82*5.2) = 9.47 tonnes of SC5.2 needed per tonne of LCE. It becomes very different when you plug this in.

So they are going to need far more than the 850kt of concentrate as stated within the article to produce those 130kt of LCE.

At the time Zijin took control of the north section, the resource was entirely inferred. This is understandable given the lack of drillholes and met work that had been undertaken (AVZ were mainly focusing on the south and doing a great job). I could be mistaken, but I haven’t seen anything via satellite (generally signs of drillholes are easily identifiable) that suggest Zijin has done further work to progress the deposit from Inferred to indicated or measured. So there's a decent chance that the proper work hasn't gone into understanding CDL and it's getting rushed.

One thing that is important to understand is that size of the deposit just one of the many criteria which should be used to rank a deposit. If the deposit is larger than 90-100Mt, I’d say it gets less and less important. Grade and metallurgy become king. So, Manono North is large, but lets talk about its grade and metallurgy.

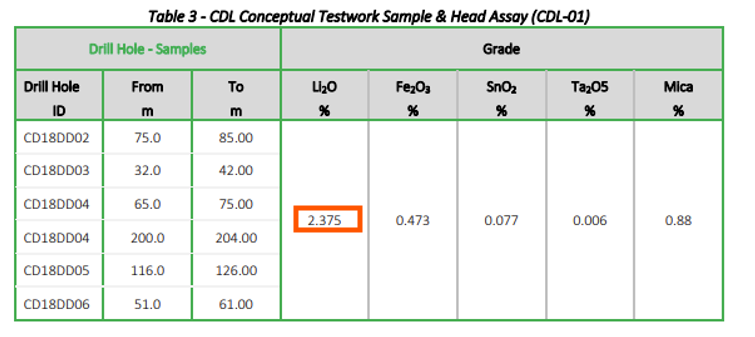

I dug into historical metallurgy testwork undertaken on the CDL pegmatite and it was average. I can’t find any flotation testwork done on CDL specifically, but the DMS testwork gave 55% recoveries for 5.6mm size and 66% for 3.35mm size. But here's the issue, the head grade used in these tests was 2.37% Li2O. The average grade of the deposit is 1.58% Li2O … What happens if you plug in the average grade of the deposit? So that rules out it being purely a DMS deposit and flotation will be required. Here’s some info from an old post on DMS and flotation from an older post of mine:

https://t.co/ZpPkyvtyMh

So they’ll need to float it which means higher CAPEX and OPEX.

There is some flotation test work done on the pegmatite to the south so I’ll use that as a bit of a guide (It’s a rough guide as metallurgy can change rapidly over 50 meters let alone kms). It came in at 81.5%. Lab work always comes in higher. Every single time. Also it's important to note that this test work was done on a higher grade pegmatite than CDL.

One example which is comparable from a testwork and grade point of view is Kathleen Valley. Manono south's testwork for flotation comes in at almost identical to how Kathleen valley’s (whole of ore flotation not DMS + flotation) did. 81.5% vs 81%. Liontown’s recovery is now at ~63% for SC5.2, 18% less than what the test work gave and not for SC6 as their test work suggested. Just an example how lab tests don't equal what actually happens in practice.

Summary: So in my opinion, Manono North will be somewhat similar to another Kathleen valley or Wodgina coming online. It's grade is somewhat above average @ 1.58% and I'd say its metallurgy is average. Yes it's large, but above 90-100Mt, this becomes less important. So overall a good deposit, but it's no Greenbushes and i don't believe it will spit out the tonnes as what many are suggesting. In order to get those tonnes you're going to need an extremely large capex and i don't think Zijin will invest that much given the nature as to how they got the deposit and also the jurisdiction (unstable).

Those are my thoughts on the Manono North Deposit. Cheers for reading.

@sparkes_dwayne@Trisseswe Brilliant analysis as always. Thanks.

Any similar review of the Ewoyaa project in Ghana? Significantly smaller resource but I keep being told that the product metallurgy is above average quality and infrastructure / logistics much better.

@Trisseswe@AtlanticLithium Likely Longstate selling down in a weak market. It didn't stop the shares doing 3x over the past few months with them selling. It won't change the outcome imv:

30-35p in q2. Or much higher if #ALL goes through with FID in H2.

Lithium prices up again in Asia. Lithium names are flying on the ASX. Note how Elevra Lithium is rerating. I would add them to the list of potential buyers of @AtlanticLithium alongside Assore and Chinese producers. #ALL#A11

Elevra is about 5x the market cap of Atlantic and yet with similar targets to produce just over 300ktpa of spodumene concentrate by 2029/2030. Obviously Elevra is already a producer, so definitely more advanced and derisked but you can see the logic for them to buy Atlantic at 30-35p and be highly value accretive for Elevra shareholders. #ALL #A11 $ELVR #ELV

The EV/battery/lithium sector is going to benefit from the sad conflict in the middle east. @AtlanticLithium is the only fully permitted quality spodumene project in Africa that has not yet been acquired by larger lithium producers. And it is still valued at only 20% of Project NPV using conservative assumptions. #ALL #A11