$PP

This dev aren’t going anywhere. He’s a real chad. Pushing n delivering even in these hard times.

Check progress below this post 👇

Current mcap: $80k

FDV mcap: 109k (24% is locked)

🎯 1m+ mcap in next 1-2 months

Slowly but steadily.😎

DrnF17MbiKXu7gVyfL13UydVvhFTSM7DDWN3Ui8npump

$sol $river $pippin $cc $aisi $avici $kamiyo $btc

$PP @Privatepay_ dev has delivered so many #privacy products in this bear market and built an entire privacy ecosystem on $sol

The doxxed Chad dev is so determined to make this a success 🙌

Only a 50k mc and chart continues to be healthy and grind up

https://t.co/xMw4coFZFT

$PP - update 💪

We Just Launched PrivatePay API

Issue. Fund. Manage. Virtual Cards.

All through code.

Whether you are building fintech, ad-tech, SaaS, or anything in between — PrivatePay handles the hard part. You focus on your product.

✅ Create virtual Visa/Mastercard

✅ Fund cards via REST API

✅ Set your own pricing & markup

✅ Full webhook support

✅ IP whitelisting & priority support

Three words:

Ship. Faster. Win.

Your customers get instant cards.

You keep the margin.

We handle compliance & infrastructure.

Ready to build?

👉 https://t.co/NCb0RfAs6B

$PP dev has no slow down button, top tier in the game and huge respect to the work being put in here.

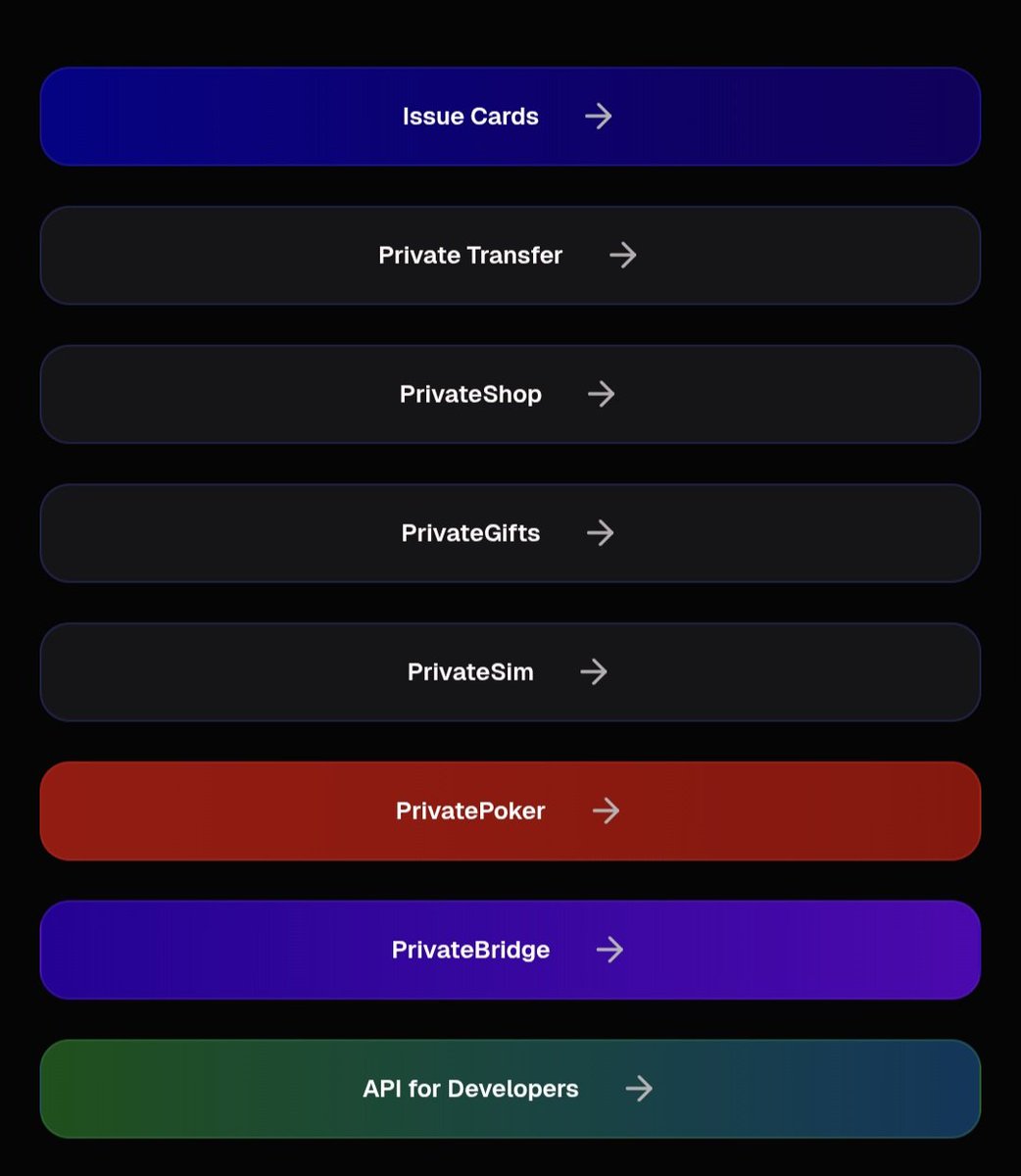

Also in last few weeks he delivered:

✅ Private transfer

✅ PrivateShop (almost done)

✅ PrivateGifts

✅ PrivateSim

✅ PrivateBridge (almost done)

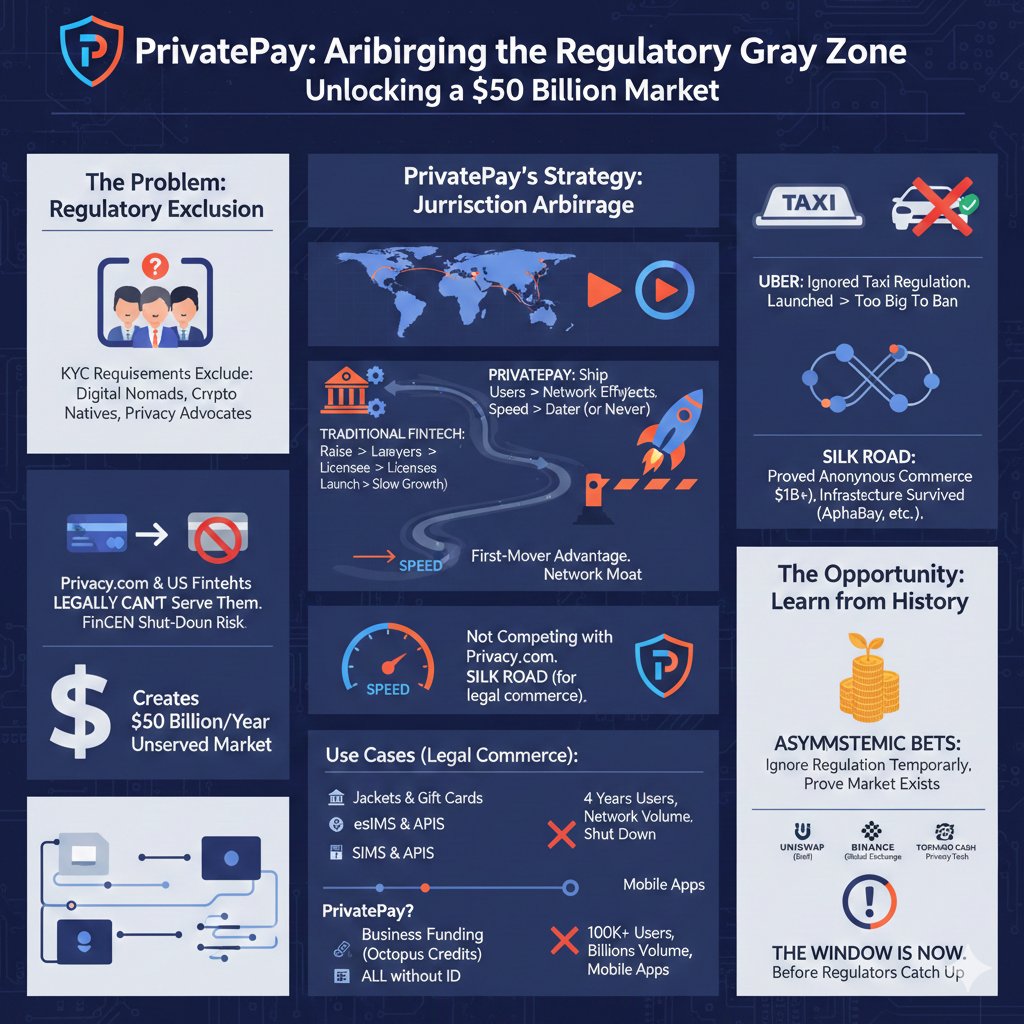

I bought $PP at 50k yesterday. Not because of the tech. Because of the arbitrage.

PrivatePay isn't competing with fintech. It's arbitraging regulatory capture.

Let me explain.

KYC requirements exist to exclude people. Digital nomads without fixed addresses. Crypto natives without utility bills. Privacy advocates who refuse to upload passport scans.

https://t.co/l3BLHjNZxd can't serve them. Not because they don't want to. Because they legally can't.

The second https://t.co/l3BLHjNZxd tries to go no-KYC, FinCEN shuts them down. They're a U.S. company. They play by U.S. rules.

That exclusion creates a $50 billion annual market that nobody can legally serve.

Until now.

PrivatePay isn't trying to be compliant. They're arbitraging jurisdiction.

They exist in the regulatory gray zone — the space between "legal" and "illegal" where innovation happens before lawmakers catch up.

This isn't reckless. It's strategic.

Think about how Uber started. Taxi medallions in NYC cost $1M+. Heavily regulated. Impossible to compete legally.

Uber didn't compete. They ignored the regulation entirely and launched before regulators could stop them.

By the time cities tried to ban Uber, millions of people were already using it. Too late.

PrivatePay is doing the same thing.

They're serving the $50 billion market that regulation created before regulators realize what's happening.

Traditional fintech goes: raise money → hire lawyers → get licenses → launch compliant product → grow slowly.

PrivatePay goes: ship product → get users → build network effects → deal with regulation later (or never).

Speed is the moat.

in crypto, speed = everything. First-mover advantage locks in. Users develop habits. Switching costs rise.

By the time https://t.co/l3BLHjNZxd adds no-KYC features (if they ever can), PrivatePay will have 10,000 users, 8 products, and a network moat.

Everyone's saying: "PrivatePay is gonna get Tornado Cash'd."

But Tornado Cash got shut down for one reason: it facilitated $7 billion in transactions including ransomware payments and North Korean sanctions evasion.

PrivatePay is selling jackets and gift cards.

And even if regulators come, they'll move too slow.

Tornado Cash ran for 4 years before shutdown. During that time, it processed billions, built brand recognition, and proved the market existed.

If PrivatePay gets 4 years, they'll have:

100,000+ users

Billions in transaction volume

Partnerships with major platforms (Octopus is just the start)

Mobile apps with mainstream distribution

The Real Comp Isn't https://t.co/l3BLHjNZxd. It's Silk Road.

Silk Road wasn't just a darknet market. It was proof that anonymous online commerce could work.

Before Silk Road, people said: "Nobody will trust buying things online without seeing the seller's identity."

Silk Road proved them wrong. $1 billion+ in transactions. Escrow systems. Reputation scores. Dispute resolution.

When the FBI shut it down, the infrastructure didn't die. AlphaBay, Dream Market, White House Market — they all learned from Silk Road and improved.

PrivatePay is doing the same thing but for legal commerce.

They're proving that no-KYC payments can work for:

Buying real products (jackets, gift cards)

Paying for services (eSIMs, APIs)

Funding businesses (Octopus credits)

All without identity verification.

Most people invest in crypto projects that try to comply with regulation.

Coinbase. Circle. Visa crypto cards. All playing by the rules.

The rules are designed to kill innovation.

The real asymmetric bets are projects that ignore regulation temporarily to prove a market exists.

Uniswap did it (launched before DeFi regulations existed).

Binance did it (operated globally before licenses).

Tornado Cash did it (proved privacy tech works).

PrivatePay is doing it for payments.

And the window is right now — before regulators figure out what's happening.

@Privatepay_@AlphaSeeker21@Degen_Hardy@King_Memento

DrnF17MbiKXu7gVyfL13UydVvhFTSM7DDWN3Ui8npump

I didn't launch PrivatePay to be just another token on Solana; I launched it to solve a real problem. Winning the hackathon proved the tech is solid, and our current stats—100 users and $1.3K in volume—show that people actually need this.

Right now, you don't have to wait for a roadmap. The utility is live. You can create non-KYC virtual cards, fund them with $SOL, and spend them immediately. I've already released the Android APK so you can manage your cards from your phone, and I’m finishing up the native iOS app right now.

While the rest of the market is chasing hype, we are building a closed-loop privacy system with real payments, private poker, and a referral engine that pays you to grow the network. We are moving fast, and we are just getting started.

Check the stats, download the APK, and see the future of privacy for yourself on our site.

Website: https://t.co/GuO81OxsLx: DrnF17MbiKXu7gVyfL13UydVvhFTSM7DDWN3Ui8npump

PrivatePay Mobile: Android APK Official Launch! 📱💳

Your privacy just went mobile. We are excited to announce that the official PrivatePay Android APK is now available for download.

Now, you can manage your non-KYC virtual cards anytime, anywhere, directly from your phone.

Mobile Features:

🆕 Card Creation: Generate new Virtual Visa/Mastercards on the fly.

📊 Balance Management: Keep track of your spending and card status in real-time.

🛡 Secure Access: High-level encryption to keep your financial data private.

🔗 Integrated Ecosystem: All your card data synced perfectly with your desktop account.

Stop relying on your desktop. Take control of your financial freedom on the go. 🌍🛡

📝 CA: DrnF17MbiKXu7gVyfL13UydVvhFTSM7DDWN3Ui8npump

Note: Apk file is available on Telegram group.

#Solana #PrivatePay #Android #FinTech #Privacy #NonKYC #SolanaGems $PP

🌉 PrivatePay Bridge is LIVE 🌉

We just launched cross-chain bridging.

No KYC. No limits. No middlemen.

Bridge between Solana and Ethereum in seconds.

Swap SOL → ETH. Move your coins across chains instantly. See it happen in real-time.

Why this matters: Most bridges trap you behind identity verification. KYC forms. Waiting periods. Denied withdrawals.

Not here.

PrivatePay Bridge is: ✅ Instant - SOL to ETH in under 3 minutes ✅ Private - No KYC, no forms, no BS ✅ Transparent - Watch every step on the explorer ✅ Cheap - Competitive rates powered by Squid Router ✅ Non-custodial - You control your keys always

Supported routes (day 1): 🟣 SOL → ETH (Ethereum mainnet) 🟣 SOL → ETH (Arbitrum) 🟣 SOL → USDC (Arbitrum) 🟣 USDC → ETH (Ethereum) 🟣 USDC → ETH (Arbitrum)

More chains coming. More tokens coming. More features coming.

Try it now: Bridge at https://t.co/K3ArCdN2ag 🌉

Connect Phantom wallet. Select your swap. Confirm. Done.

Your crypto. Your way. No permission slip needed.

Ca: DrnF17MbiKXu7gVyfL13UydVvhFTSM7DDWN3Ui8npump

#DeFi #Solana #Ethereum #Bridge #CrossChain #Web3 #PrivatePay #Crypto

They ask if the cards are real. We just paid for X subscription with #PP 🛡️💳

No KYC. No bank. Just pure Solana utility. While others are talking about 'roadmap,' we’re already live and spending.

Access is officially open at 0.5% $PP. Get yours before the week starts. 🤐🚀

$PP #Solana #NoKYC #Privacy #BuildInPublic"