I am not a licensed financial advisor and as such, I do not post financial advice. All X are my thoughts and opinions, solely information and entertainment.

“with foresight, the excitement was palpable.”

bonds. by the time everyone else realizes GameStop will not have to deplete 88% of their balance sheet cash, excitement will be off the charts.

bonds are not notes.

$GME

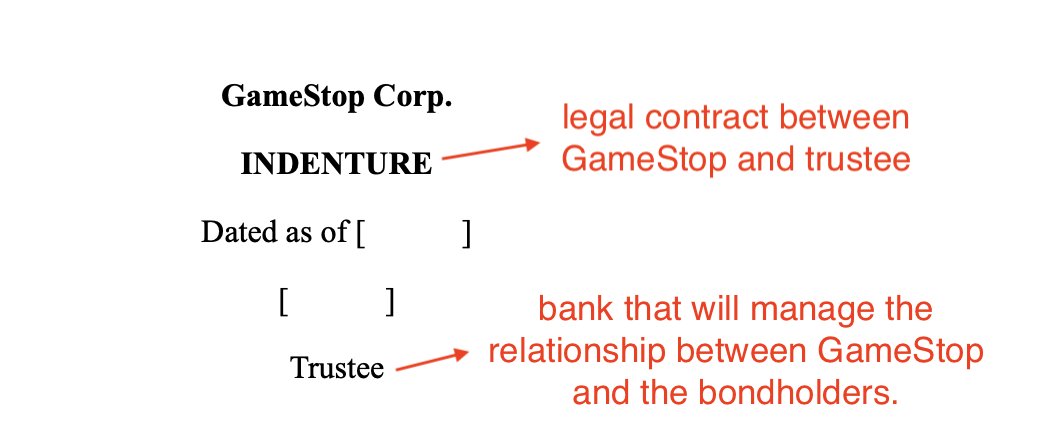

after RC's interview with the WSJ it really looks like all the pieces are starting to fit together for $GME. quoted to this post is my observation about GameStop filing a templated bond indenture back in October with the modified S-3 from the warrants.

so now we have:

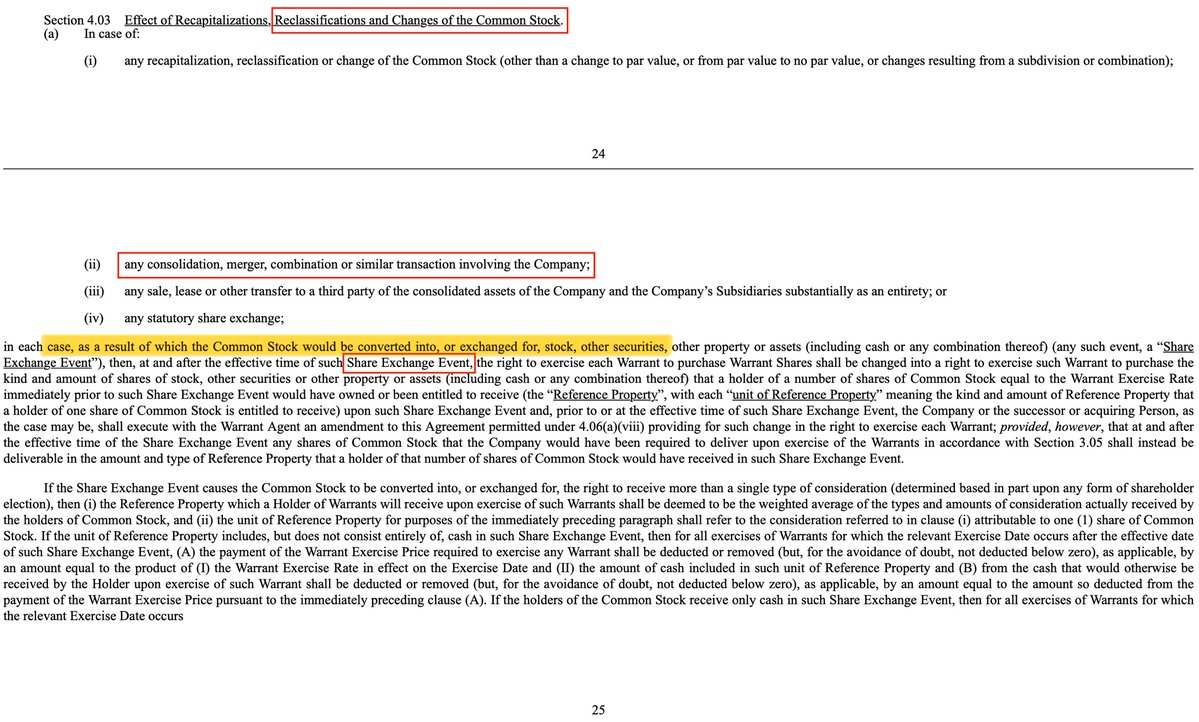

• a warrant agreement that outlines a "Share Exchange Event" if there were to be a merger or acquisition, a new class of shares, etc. (section 4);

• a ready-to-go bond indenture;

• the GameStop board announcing a compensation package for RC;

• big dog himself telling the WSJ that he is looking to make a large acquisition.

who needs forward guidance when the roadmap is this clear!

the bond indenture is a finalized, execution-ready document. there is just no way that they filed this as a "just in case" and it became painfully obvious after the interview article. you don't file detailed indenture documents unless bond issuance is part of a concrete capital plan. that's when it clicked.

when the compensation package was revealed it whimsically (read: intentionally) did not have a set shareholder vote date set and just said "sometime in March or April". none of it is coincidence I believe all of it is planned around the Company's annual earnings release and they are going to issue bonds to help fund their big acquisition(s). the only question is in what order?

I thought to myself, for someone who never "telegraphs their strategy", why is RC saying that they are ready to utilize the investment policy and make an acquisition? what purpose does it serve? then it hit me. are they doing the bond roadshow right now?

here's the thing. almost half of GME's cash is from the convertible notes and if they just went and marketed a bond raise it could face significant skepticism and demand weak pricing, maybe even get a lacklustre credit rating. investors might push for a higher yield premium for their risk.

but if big dog is talking to the main M&A writer for the Wall Street Journal, well, that changes everything. bond markets like certainty and RC just gave out his plan for all of them to hear. I think he is providing a use of proceeds narrative and creating the business rationale that bond investors like to hear.

here I thought that the vote on the compensation package was going to be first but it may be the last piece. in my opinion this unfolds in one of two ways:

one:

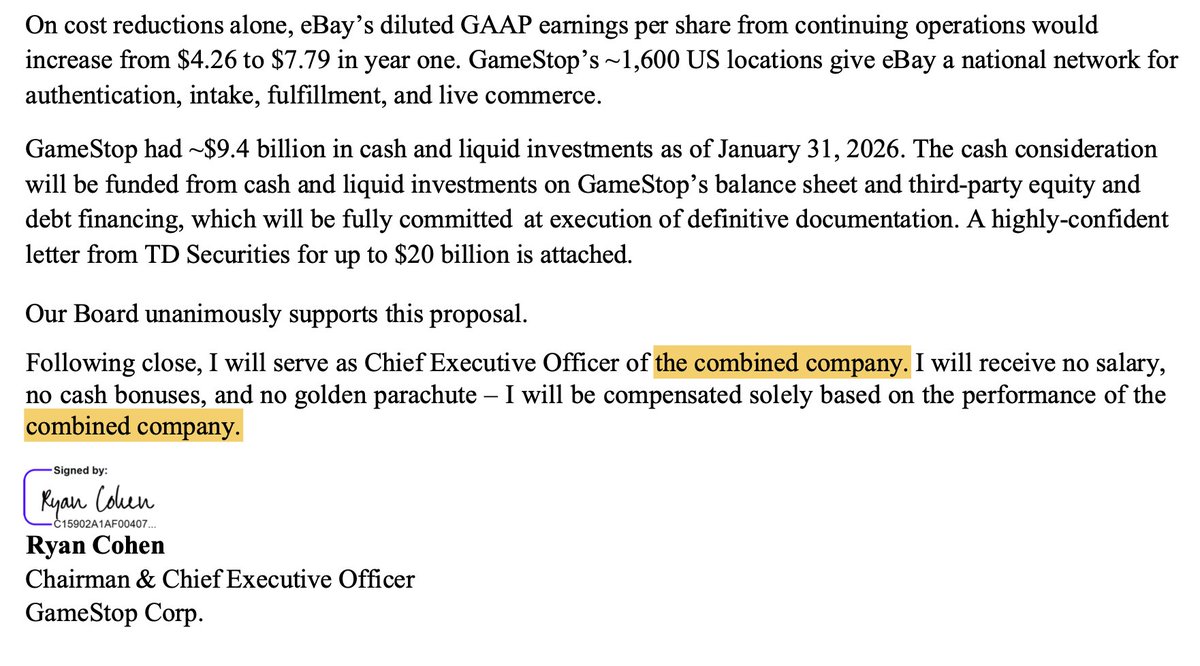

• first will come the annual earnings to give an up-to-date financial baseline before major strategic moves. this will show credibility with institutional investors before asking them to evaluate a major acquisition;

• make an acquisition announcement in hopes of boosting the stock price and creating momentum heading into the shareholder vote on the pay package;

• issue the bonds to offset the cost, fill a funding gap or if the acquisition is announced with some lead time, get the financing in order before closing.

• shareholders can evaluate big dog's strategy and vision ahead of the vote to approve the pay package.

I think the pay package and its astronomical targets might create stock price volatility that could complicate bond pricing so I think no matter what, it happens last. (this places all other events before or inside of "March or April").

two:

• earnings first for up-to-date financials;

• everything else from the first point stays the same but the acquisition and bond issuance announcements are bundled together to signal confidence into the stock price (against the price of an acquisition);

• pay pack vote last to show the vision and get approval.

remember, the bond indenture was filed back in October 2025 so every step has been planned out for a long time. they have probably engaged with the Investment banks for months already. same goes for anchor investor(s) (maybe this is how Mr. Almadeed fits into the picture in all this).

three:

• things are happening really quickly, the bonds are about to be marketed or are right now and this is why big dog gave the interview to WSJ.

• earnings will come afterwards because "things are moving fast" for whatever reason.

the biggest signal of this option happening will be an earnings pre-release like there was in May 2024 before the first ATM offering.

I believe that the second option is the most likely. RC communicating the plan to the news was a bit of a curve ball on the timeline, but maybe it is to negotiate attractive bond pricing and have investors lined up well ahead of time, just like they did with the templated indenture.

it makes the most sense to announce the acquisition and financing together as a complete and strategic plan because it will make everyone happy. the bond investors hear about specific use of proceeds and a clear business rationale; equity investors will be happy because it avoids the uncertainty of announcing an acquisition without explaining how it will be paid for. that will absolutely insulate downward pressure on the stock if it is known the current cash pile won't be depleted. you tell the market one comprehensive story. bond buyers can see the complete transaction, (maybe even giving GME leverage to negotiate better pricing?), create some excitement and momentum from a major announcement that could drive stock price acceleration ahead of the pay pack vote.

the really exciting thing about the bond indenture is it opens the flood gates for how big the GameStop Board could be thinking.

rocket. wee. genesis. isn't it obvious?

I’m excited about the share buyback authorization like everyone else but in my opinion, I don’t think it will be utilized now. lowering the balance sheet cash would make it more difficult to conduct the bond roadshow, both in the ability of how much can be raised and would result in higher interest rates from fixed-income investors based on risk. you want to look strong when marketing yourself for investment.

if a genie granted me a wish the ideal series of events would be to raise a ton of corporate debt, have the market sink the stock price to middle earth on this news (“oh no, huge leverage! they’re going bankrupt!”), buy back down there, note holder arbs go super long, the stock price explodes, present the tender offer to eBay shareholders at that price with the goal of dipping into authorized shares as little as possible.

we’ll see.

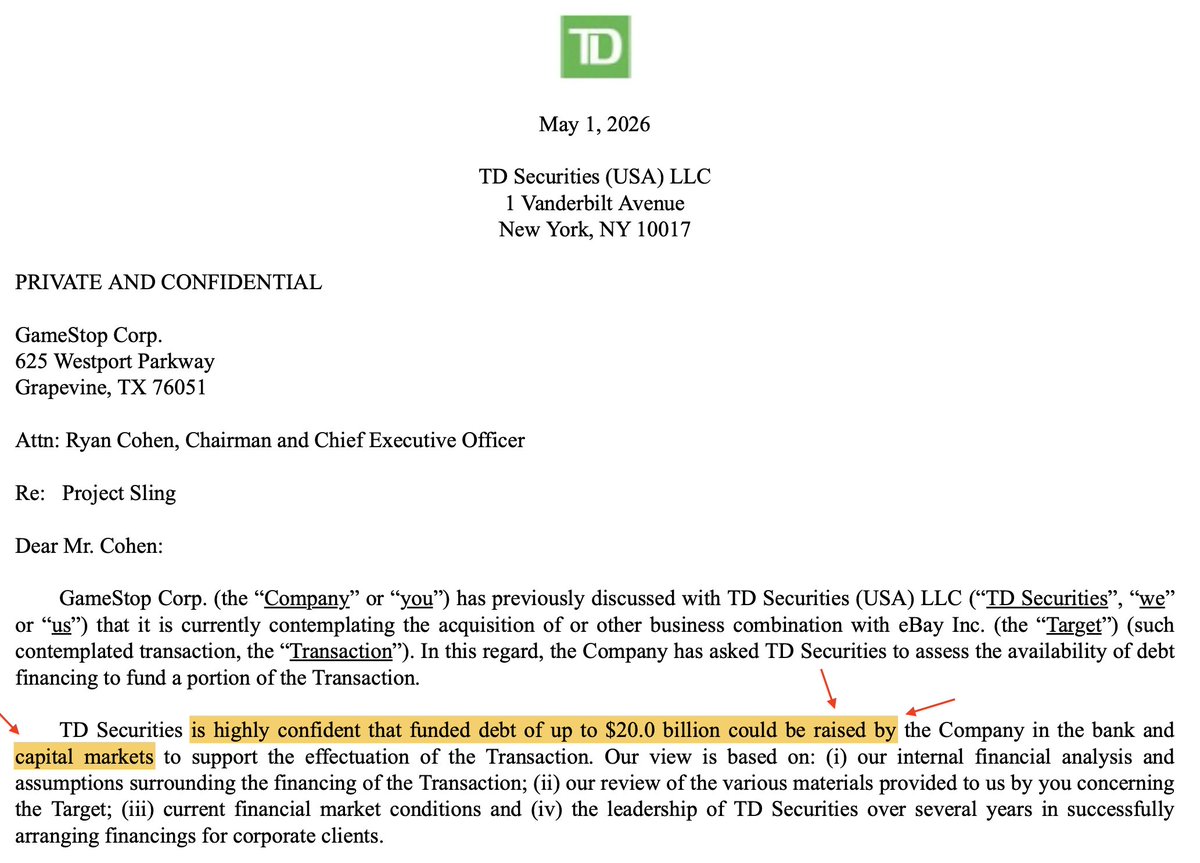

@bobdole08923509 my hope would be that the bond offering was oversubscribed and they raised more than 20b, maybe even 28 and wouldn’t have to use any cash on hand for the eBay deal, or maybe an investor group comes alongside the fixed-income investors and tops it up.

part 7: I would like to share compelling points relating to the HBC equity raise and its use to secure the position of the Holder of Interests, which forced participation in the $BBBYQ third-party release. I hope you like it.

$BBBY

(old).

a handful of comments to this post presented a counter that the participants were not friendly to $BBBYQ and they wanted to exit their investment.

this argument fails logic but it was also not possible. the Company issued restricted shares which means the investors had to hold them for a minimum of 6 months, sometimes up to a year before they could transact with them.

thank you for your comment @JuicyPabl0.

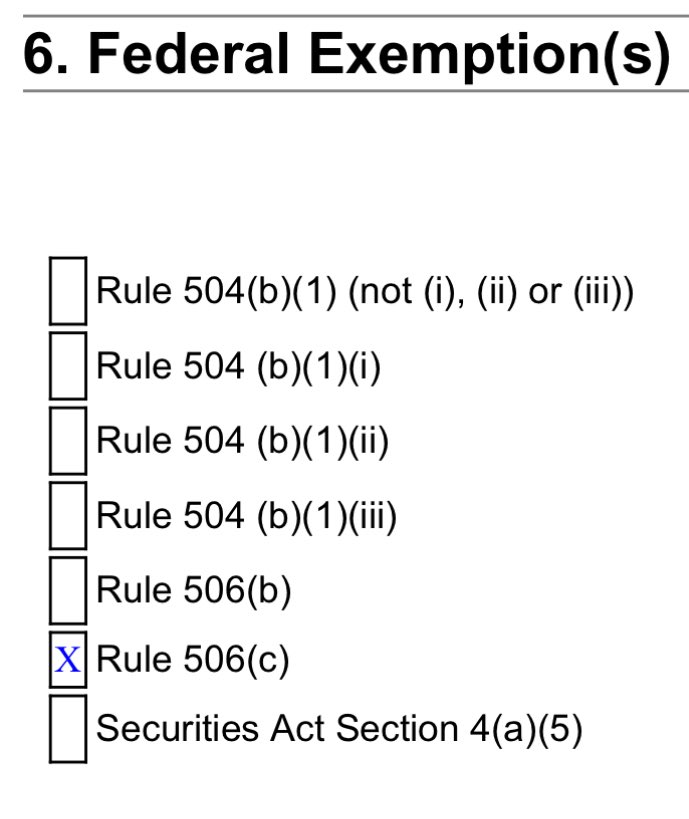

Rule 506(c): https://t.co/LtMd5K6qoB

I was reading through old $BBBYQ SEC filings and came across something that really stood out. whatever the intentions of the affiliates and/or Purchaser, the assets had to have been secured at the end of 2022 in some way.

think back to the private bond exchanges; there was first a single investor, then an institutional group that followed by retiring their bonds for shares some time between November 14 and December 6, 2022. here is what I had never caught before:

[image 1]

thanks to accounting requirements there is disclosure in the 10-Q that the exchange was performed under what is called a "troubled debt restructuring". that can only be used under very specific circumstances, say if a company discloses that it may not be able to continue as a going concern. if we dive into the math on the deal we will see that whoever participated in the exchange was friendly to the company. here's why:

[image 2]

the aggregate principal amount retired through the bond exchange:

69.0 (2024) + 15.3 (2034) + 70.2 (2044) = 154.5 million dollars worth of bond debt.

[image 3]

but investors only received:

first Form D: 2,762,444 shares which was an offering amount of 10,331,540$;

second Form D: 11,667,021 shares which was an offering amount of 40,717,903$;

10,331,540 + 40,717,903 = 51,049,443$.

[image 3]

154.5 million of debt was retired in exchange for 51 million dollars’ worth of shares. the bond holders exchanged at 0.33 on the dollar when they could have just sold them on the open market at the time for a better return plus the individual investor gave the Company another 3.5 million dollars cash for 0.9 million additional shares.

the Company obviously benefitted tremendously from this deal, recording a 94.4 million dollar gain (the net difference) on their 10-Q. who would do that? the only way it makes sense is if the former bond, then equity holders received something more than just the shares in return. the only alternative explanation is preferring to lose money over open market sales to help the Company.

[image 4]

fun little side fact, looking at the TSO from the 10-Q (which was late!) if you look at the share amount received by the institutional group they total 9.9444% ownership, just under 10% with no way to round up to 10% and be labelled an insider. two more fun facts, the Company filed that their 10-Q was going to be late on the same day the bond exchange was finally terminated with no more extensions, and, the "troubled debt restructuring" was only revealed in the 10-Q itself, over a month later.

to summarize: no investor retires their senior, secured debt instrument for junior, unsecured equity at a loss compared to open-market price to help the Company's balance sheet, unless they got something in return. this exchange retired 25% of all 2024 bonds, an imminent insolvency risk at the time.

so.. what did they get?

@m74ft1@SwamiKnows_@JuicyPabl0 it is weird and not productive keeping an imaginary score but thank you for your input I’ll have another look at it all after work. there’s nothing wrong with being wrong.

don’t take the internet so seriously.

I was reading through old $BBBYQ SEC filings and came across something that really stood out. whatever the intentions of the affiliates and/or Purchaser, the assets had to have been secured at the end of 2022 in some way.

think back to the private bond exchanges; there was first a single investor, then an institutional group that followed by retiring their bonds for shares some time between November 14 and December 6, 2022. here is what I had never caught before:

[image 1]

thanks to accounting requirements there is disclosure in the 10-Q that the exchange was performed under what is called a "troubled debt restructuring". that can only be used under very specific circumstances, say if a company discloses that it may not be able to continue as a going concern. if we dive into the math on the deal we will see that whoever participated in the exchange was friendly to the company. here's why:

[image 2]

the aggregate principal amount retired through the bond exchange:

69.0 (2024) + 15.3 (2034) + 70.2 (2044) = 154.5 million dollars worth of bond debt.

[image 3]

but investors only received:

first Form D: 2,762,444 shares which was an offering amount of 10,331,540$;

second Form D: 11,667,021 shares which was an offering amount of 40,717,903$;

10,331,540 + 40,717,903 = 51,049,443$.

[image 3]

154.5 million of debt was retired in exchange for 51 million dollars’ worth of shares. the bond holders exchanged at 0.33 on the dollar when they could have just sold them on the open market at the time for a better return plus the individual investor gave the Company another 3.5 million dollars cash for 0.9 million additional shares.

the Company obviously benefitted tremendously from this deal, recording a 94.4 million dollar gain (the net difference) on their 10-Q. who would do that? the only way it makes sense is if the former bond, then equity holders received something more than just the shares in return. the only alternative explanation is preferring to lose money over open market sales to help the Company.

[image 4]

fun little side fact, looking at the TSO from the 10-Q (which was late!) if you look at the share amount received by the institutional group they total 9.9444% ownership, just under 10% with no way to round up to 10% and be labelled an insider. two more fun facts, the Company filed that their 10-Q was going to be late on the same day the bond exchange was finally terminated with no more extensions, and, the "troubled debt restructuring" was only revealed in the 10-Q itself, over a month later.

to summarize: no investor retires their senior, secured debt instrument for junior, unsecured equity at a loss compared to open-market price to help the Company's balance sheet, unless they got something in return. this exchange retired 25% of all 2024 bonds, an imminent insolvency risk at the time.

so.. what did they get?

I follow everything you’re saying here and I was not citing this but the 2014 indenture.

you are correct about secured vs. unsecured debt I should have worded that better. the original indenture had language intended to prevent anyone from asserting a lien of any kind without the bond holders getting the same, improved treatment first and had similar protections for a change in control, but the bonds were unsecured when written.

what I was trying to say was the investors traded a more senior and better protected financial instrument for a junior, completely at risk one. thanks for your keen eye man!

@SwamiKnows_ I can’t tell if you are making a joke or being serious but that’s not possible as @JuicyPabl0 kindly added yesterday. these shares were (had to be) held minimum 6 months.

after Chapter 11 started yea but the bonds were secured by liens until then and they were trading above 0.40 at the time of the deal.

I mostly agree with the rest of what you’re saying this is one of the reasons why the DIP was so contested because “enough” was put in superpriority that they obtained full control of all the assets and later ensure the possibility of a cramdown.

“I was totally going to buy this, spent hundreds of hours planning the venture, had a roadmap to 600 million revenue, recruited executive talent and then I didn’t because the IP sold for 3.5-23.5 million dollars less than what I was willing to pay.”

$BBBYQ

imagine the surprise after $EBAY formally declines the purchase offer, $GME counters with an “all-cash, no stock” deal. with the backing of a financier/investment group it would be quite an ace up the sleeve, nullifying the board’s reasons for declining and thereby cornering them into acceptance under fiduciary duty.

the coy responses about the how they can pull it off would sure start to make a lot of sense. now, imagine if plan b was plan a. the best ones are always many steps ahead.

“with foresight, the excitement was palpable.”

bonds. by the time everyone else realizes GameStop will not have to deplete 88% of their balance sheet cash, excitement will be off the charts.

bonds are not notes.

$GME

after RC's interview with the WSJ it really looks like all the pieces are starting to fit together for $GME. quoted to this post is my observation about GameStop filing a templated bond indenture back in October with the modified S-3 from the warrants.

so now we have:

• a warrant agreement that outlines a "Share Exchange Event" if there were to be a merger or acquisition, a new class of shares, etc. (section 4);

• a ready-to-go bond indenture;

• the GameStop board announcing a compensation package for RC;

• big dog himself telling the WSJ that he is looking to make a large acquisition.

who needs forward guidance when the roadmap is this clear!

the bond indenture is a finalized, execution-ready document. there is just no way that they filed this as a "just in case" and it became painfully obvious after the interview article. you don't file detailed indenture documents unless bond issuance is part of a concrete capital plan. that's when it clicked.

when the compensation package was revealed it whimsically (read: intentionally) did not have a set shareholder vote date set and just said "sometime in March or April". none of it is coincidence I believe all of it is planned around the Company's annual earnings release and they are going to issue bonds to help fund their big acquisition(s). the only question is in what order?

I thought to myself, for someone who never "telegraphs their strategy", why is RC saying that they are ready to utilize the investment policy and make an acquisition? what purpose does it serve? then it hit me. are they doing the bond roadshow right now?

here's the thing. almost half of GME's cash is from the convertible notes and if they just went and marketed a bond raise it could face significant skepticism and demand weak pricing, maybe even get a lacklustre credit rating. investors might push for a higher yield premium for their risk.

but if big dog is talking to the main M&A writer for the Wall Street Journal, well, that changes everything. bond markets like certainty and RC just gave out his plan for all of them to hear. I think he is providing a use of proceeds narrative and creating the business rationale that bond investors like to hear.

here I thought that the vote on the compensation package was going to be first but it may be the last piece. in my opinion this unfolds in one of two ways:

one:

• first will come the annual earnings to give an up-to-date financial baseline before major strategic moves. this will show credibility with institutional investors before asking them to evaluate a major acquisition;

• make an acquisition announcement in hopes of boosting the stock price and creating momentum heading into the shareholder vote on the pay package;

• issue the bonds to offset the cost, fill a funding gap or if the acquisition is announced with some lead time, get the financing in order before closing.

• shareholders can evaluate big dog's strategy and vision ahead of the vote to approve the pay package.

I think the pay package and its astronomical targets might create stock price volatility that could complicate bond pricing so I think no matter what, it happens last. (this places all other events before or inside of "March or April").

two:

• earnings first for up-to-date financials;

• everything else from the first point stays the same but the acquisition and bond issuance announcements are bundled together to signal confidence into the stock price (against the price of an acquisition);

• pay pack vote last to show the vision and get approval.

remember, the bond indenture was filed back in October 2025 so every step has been planned out for a long time. they have probably engaged with the Investment banks for months already. same goes for anchor investor(s) (maybe this is how Mr. Almadeed fits into the picture in all this).

three:

• things are happening really quickly, the bonds are about to be marketed or are right now and this is why big dog gave the interview to WSJ.

• earnings will come afterwards because "things are moving fast" for whatever reason.

the biggest signal of this option happening will be an earnings pre-release like there was in May 2024 before the first ATM offering.

I believe that the second option is the most likely. RC communicating the plan to the news was a bit of a curve ball on the timeline, but maybe it is to negotiate attractive bond pricing and have investors lined up well ahead of time, just like they did with the templated indenture.

it makes the most sense to announce the acquisition and financing together as a complete and strategic plan because it will make everyone happy. the bond investors hear about specific use of proceeds and a clear business rationale; equity investors will be happy because it avoids the uncertainty of announcing an acquisition without explaining how it will be paid for. that will absolutely insulate downward pressure on the stock if it is known the current cash pile won't be depleted. you tell the market one comprehensive story. bond buyers can see the complete transaction, (maybe even giving GME leverage to negotiate better pricing?), create some excitement and momentum from a major announcement that could drive stock price acceleration ahead of the pay pack vote.

the really exciting thing about the bond indenture is it opens the flood gates for how big the GameStop Board could be thinking.

rocket. wee. genesis. isn't it obvious?

what if the ace up the sleeve for $GME is not about the actual acquisition, but what happens after the acquisition? what if it is Delaware Law Title 8, Chapter 1, Subchapter IX. Merger, Consolidation or Conversion.

specifically §251(g)?

like many I was surprised to see RC doing the media tour and for the first time, hyping how big their plans will be. I mentioned before that a likely explanation could be they are doing a roadshow for an upcoming traditional bond offering. I also couldn’t help but worry when I read some snippets:

“it's gonna be really big. Really big. Very, very, very big," Cohen said of the size of the acquisition.”

“this is something that really has never been done before within the history of the capital markets.”

“it has the "potential to make [GameStop] worth several hundreds of billions of dollars.”

..because no matter what the Board was planning, the market could make this the largest sell-the-news event in history to try and curb their momentum and sentiment around the pivot of GameStop into a holding company.

why would big dog do that? why would he not say basically anything for 5 years then suddenly risk shooting himself in the foot by making grandiose claims about their first acquisition? lets not overlook that in the CNBC article he claims this one acquisition could propel the market cap of the company to the extent his entire pay package vests..

it got me thinking about why he would be so confident. then I found §251(g):

“Delaware General Corporation Law Section 251(g) allows a corporation to reorganize into a holding company structure without requiring a stockholder vote. This statutory provision facilitates mergers with a wholly-owned subsidiary, ensuring the holding company has the same charter provisions as the original corporation, often used for corporate restructuring or, historically, for adopting anti-takeover measures.”

emphasis mine. it is mainly used to create a new, top-level holding company where the original parent corporation used to be. That old parent co becomes a subsidiary and shareholders receive identical shares in the new holding company.

“Section 251(g) facilitates a holding company reorganization merger where outstanding shares of the original corporation are automatically converted into equivalent shares of the new holding company upon the merger’s effective time, provided all statutory conditions are met (e.g., identical rights and no tax recognition). This conversion is seamless and does not require surrendering or recalling physical certificates or shares,..”

hang on.. I know exactly what I thought of when I read that. do you remember this?

this sure provides a convenient explanation. oh, I can already hear the naysayers.. upon the merger's effective time. do you now remember what happened immediately before September 2024? the Board closed their credit facility and less than one month later, a pre-negotiated, pre-settled agreement was filed by the FTC.

I wrote at the time that I believed the Company applied to the FTC for a pre-merger certificate, hence why the settlement came out when it did and that the issuance of the certificate occurred after the second, 30-day review period following the filing of RC's settlement of the FTC violation. that is why he tweeted "yolo" exactly 60 days after the application for the certificate, because he got it.

OK back on topic. guess what else?

if they want to, a company can reissue shares under §251(g) as tokenized shares even if they weren’t tokenized before, as long as the tokenized shares are identical in all the important respects like rights, voting powers, etc. to the original shares. this is explained in §251(g)(2).

“Since §251(g) allows for a holding company reorganization where the new parent issues shares that mirror the originals, the holding company can adopt a blockchain-based stock ledger for its issuance process. This doesn’t violate the “identical” requirement because the form of record-keeping (traditional vs. blockchain) is administrative, not substantive—much like switching from certificated to uncertificated shares, which Delaware law expressly supports.”

hang on now.. do you remember the S-3 that was filed in May 2024, defining digital assets inside of the sale agreement contract between GME and Jefferies? for their share offering?

GameStop’s current corporate structure looks like this: GameStop Corp (parent) holding company → GameStop Inc (subsidiary) that manages retail operations. the shares are issued for ownership of the parent company. important to understand that the legacy business is managed by a subsidiary.

what if in the future GameStop wanted to maintain the brand identity for their retail business as the premier destination for how to spend your leisure time, but wanted to have a new name for their investment behemoth diversified holding company.. like Teddy?

they could:

• acquire a company that they find undervalued or owning an asset they would want;

• place it as a subsidiary of GameStop Corp;

• perform a Section 251(g) corporate reorganization;

• and name it whatever they want.

then it becomes Teddy (probably) → GameStop Corp → GameStop Inc.

you may be wondering why? ..well, tell me why shares of GME were labelled new class in 2024? kidding aside, this allows GameStop Corp to keep its current roles: strategic oversight, capital allocation, governance.. the investment policy.., and allows a new parent corporation to be formed to hold all of the acquisitions made by a dying, brick and mortar retailer-turned-investment fortress, managed by big dog and friends. and! it does not require a shareholder vote.

that could explain Section 4 of the warrant agreement, specifically why they chose to include legal definitions around a “Share Exchange Event” in the event of a reorganization:

it would explain the “new class” anomaly observed in September 2024 (or it was a private placement);

it would explain why the ATM agreement would require GME and Jefferies to have explained digital assets in a contract only to do with selling of their shares;

and lastly, it could explain why RC is so confident in his interviews with the news media.

talk about exciting times.

n.b.—this is just my personal opinion and fun speculation.

![jake2b's tweet photo. I was reading through old $BBBYQ SEC filings and came across something that really stood out. whatever the intentions of the affiliates and/or Purchaser, the assets had to have been secured at the end of 2022 in some way.

think back to the private bond exchanges; there was first a single investor, then an institutional group that followed by retiring their bonds for shares some time between November 14 and December 6, 2022. here is what I had never caught before:

[image 1]

thanks to accounting requirements there is disclosure in the 10-Q that the exchange was performed under what is called a "troubled debt restructuring". that can only be used under very specific circumstances, say if a company discloses that it may not be able to continue as a going concern. if we dive into the math on the deal we will see that whoever participated in the exchange was friendly to the company. here's why:

[image 2]

the aggregate principal amount retired through the bond exchange:

69.0 (2024) + 15.3 (2034) + 70.2 (2044) = 154.5 million dollars worth of bond debt.

[image 3]

but investors only received:

first Form D: 2,762,444 shares which was an offering amount of 10,331,540$;

second Form D: 11,667,021 shares which was an offering amount of 40,717,903$;

10,331,540 + 40,717,903 = 51,049,443$.

[image 3]

154.5 million of debt was retired in exchange for 51 million dollars’ worth of shares. the bond holders exchanged at 0.33 on the dollar when they could have just sold them on the open market at the time for a better return plus the individual investor gave the Company another 3.5 million dollars cash for 0.9 million additional shares.

the Company obviously benefitted tremendously from this deal, recording a 94.4 million dollar gain (the net difference) on their 10-Q. who would do that? the only way it makes sense is if the former bond, then equity holders received something more than just the shares in return. the only alternative explanation is preferring to lose money over open market sales to help the Company.

[image 4]

fun little side fact, looking at the TSO from the 10-Q (which was late!) if you look at the share amount received by the institutional group they total 9.9444% ownership, just under 10% with no way to round up to 10% and be labelled an insider. two more fun facts, the Company filed that their 10-Q was going to be late on the same day the bond exchange was finally terminated with no more extensions, and, the "troubled debt restructuring" was only revealed in the 10-Q itself, over a month later.

to summarize: no investor retires their senior, secured debt instrument for junior, unsecured equity at a loss compared to open-market price to help the Company's balance sheet, unless they got something in return. this exchange retired 25% of all 2024 bonds, an imminent insolvency risk at the time.

so.. what did they get?](https://pbs.twimg.com/media/HJQ4-CDXMAASput.jpg)

![jake2b's tweet photo. I was reading through old $BBBYQ SEC filings and came across something that really stood out. whatever the intentions of the affiliates and/or Purchaser, the assets had to have been secured at the end of 2022 in some way.

think back to the private bond exchanges; there was first a single investor, then an institutional group that followed by retiring their bonds for shares some time between November 14 and December 6, 2022. here is what I had never caught before:

[image 1]

thanks to accounting requirements there is disclosure in the 10-Q that the exchange was performed under what is called a "troubled debt restructuring". that can only be used under very specific circumstances, say if a company discloses that it may not be able to continue as a going concern. if we dive into the math on the deal we will see that whoever participated in the exchange was friendly to the company. here's why:

[image 2]

the aggregate principal amount retired through the bond exchange:

69.0 (2024) + 15.3 (2034) + 70.2 (2044) = 154.5 million dollars worth of bond debt.

[image 3]

but investors only received:

first Form D: 2,762,444 shares which was an offering amount of 10,331,540$;

second Form D: 11,667,021 shares which was an offering amount of 40,717,903$;

10,331,540 + 40,717,903 = 51,049,443$.

[image 3]

154.5 million of debt was retired in exchange for 51 million dollars’ worth of shares. the bond holders exchanged at 0.33 on the dollar when they could have just sold them on the open market at the time for a better return plus the individual investor gave the Company another 3.5 million dollars cash for 0.9 million additional shares.

the Company obviously benefitted tremendously from this deal, recording a 94.4 million dollar gain (the net difference) on their 10-Q. who would do that? the only way it makes sense is if the former bond, then equity holders received something more than just the shares in return. the only alternative explanation is preferring to lose money over open market sales to help the Company.

[image 4]

fun little side fact, looking at the TSO from the 10-Q (which was late!) if you look at the share amount received by the institutional group they total 9.9444% ownership, just under 10% with no way to round up to 10% and be labelled an insider. two more fun facts, the Company filed that their 10-Q was going to be late on the same day the bond exchange was finally terminated with no more extensions, and, the "troubled debt restructuring" was only revealed in the 10-Q itself, over a month later.

to summarize: no investor retires their senior, secured debt instrument for junior, unsecured equity at a loss compared to open-market price to help the Company's balance sheet, unless they got something in return. this exchange retired 25% of all 2024 bonds, an imminent insolvency risk at the time.

so.. what did they get?](https://pbs.twimg.com/media/HJQ4-CCXoAEYha8.jpg)

![jake2b's tweet photo. I was reading through old $BBBYQ SEC filings and came across something that really stood out. whatever the intentions of the affiliates and/or Purchaser, the assets had to have been secured at the end of 2022 in some way.

think back to the private bond exchanges; there was first a single investor, then an institutional group that followed by retiring their bonds for shares some time between November 14 and December 6, 2022. here is what I had never caught before:

[image 1]

thanks to accounting requirements there is disclosure in the 10-Q that the exchange was performed under what is called a "troubled debt restructuring". that can only be used under very specific circumstances, say if a company discloses that it may not be able to continue as a going concern. if we dive into the math on the deal we will see that whoever participated in the exchange was friendly to the company. here's why:

[image 2]

the aggregate principal amount retired through the bond exchange:

69.0 (2024) + 15.3 (2034) + 70.2 (2044) = 154.5 million dollars worth of bond debt.

[image 3]

but investors only received:

first Form D: 2,762,444 shares which was an offering amount of 10,331,540$;

second Form D: 11,667,021 shares which was an offering amount of 40,717,903$;

10,331,540 + 40,717,903 = 51,049,443$.

[image 3]

154.5 million of debt was retired in exchange for 51 million dollars’ worth of shares. the bond holders exchanged at 0.33 on the dollar when they could have just sold them on the open market at the time for a better return plus the individual investor gave the Company another 3.5 million dollars cash for 0.9 million additional shares.

the Company obviously benefitted tremendously from this deal, recording a 94.4 million dollar gain (the net difference) on their 10-Q. who would do that? the only way it makes sense is if the former bond, then equity holders received something more than just the shares in return. the only alternative explanation is preferring to lose money over open market sales to help the Company.

[image 4]

fun little side fact, looking at the TSO from the 10-Q (which was late!) if you look at the share amount received by the institutional group they total 9.9444% ownership, just under 10% with no way to round up to 10% and be labelled an insider. two more fun facts, the Company filed that their 10-Q was going to be late on the same day the bond exchange was finally terminated with no more extensions, and, the "troubled debt restructuring" was only revealed in the 10-Q itself, over a month later.

to summarize: no investor retires their senior, secured debt instrument for junior, unsecured equity at a loss compared to open-market price to help the Company's balance sheet, unless they got something in return. this exchange retired 25% of all 2024 bonds, an imminent insolvency risk at the time.

so.. what did they get?](https://pbs.twimg.com/media/HJQ4-CCWAAEw0k4.jpg)

![jake2b's tweet photo. what if the ace up the sleeve for $GME is not about the actual acquisition, but what happens after the acquisition? what if it is Delaware Law Title 8, Chapter 1, Subchapter IX. Merger, Consolidation or Conversion.

specifically §251(g)?

like many I was surprised to see RC doing the media tour and for the first time, hyping how big their plans will be. I mentioned before that a likely explanation could be they are doing a roadshow for an upcoming traditional bond offering. I also couldn’t help but worry when I read some snippets:

“it's gonna be really big. Really big. Very, very, very big," Cohen said of the size of the acquisition.”

“this is something that really has never been done before within the history of the capital markets.”

“it has the "potential to make [GameStop] worth several hundreds of billions of dollars.”

..because no matter what the Board was planning, the market could make this the largest sell-the-news event in history to try and curb their momentum and sentiment around the pivot of GameStop into a holding company.

why would big dog do that? why would he not say basically anything for 5 years then suddenly risk shooting himself in the foot by making grandiose claims about their first acquisition? lets not overlook that in the CNBC article he claims this one acquisition could propel the market cap of the company to the extent his entire pay package vests..

it got me thinking about why he would be so confident. then I found §251(g):

“Delaware General Corporation Law Section 251(g) allows a corporation to reorganize into a holding company structure without requiring a stockholder vote. This statutory provision facilitates mergers with a wholly-owned subsidiary, ensuring the holding company has the same charter provisions as the original corporation, often used for corporate restructuring or, historically, for adopting anti-takeover measures.”

emphasis mine. it is mainly used to create a new, top-level holding company where the original parent corporation used to be. That old parent co becomes a subsidiary and shareholders receive identical shares in the new holding company.

“Section 251(g) facilitates a holding company reorganization merger where outstanding shares of the original corporation are automatically converted into equivalent shares of the new holding company upon the merger’s effective time, provided all statutory conditions are met (e.g., identical rights and no tax recognition). This conversion is seamless and does not require surrendering or recalling physical certificates or shares,..”

hang on.. I know exactly what I thought of when I read that. do you remember this?

this sure provides a convenient explanation. oh, I can already hear the naysayers.. upon the merger's effective time. do you now remember what happened immediately before September 2024? the Board closed their credit facility and less than one month later, a pre-negotiated, pre-settled agreement was filed by the FTC.

I wrote at the time that I believed the Company applied to the FTC for a pre-merger certificate, hence why the settlement came out when it did and that the issuance of the certificate occurred after the second, 30-day review period following the filing of RC's settlement of the FTC violation. that is why he tweeted "yolo" exactly 60 days after the application for the certificate, because he got it.

OK back on topic. guess what else?

if they want to, a company can reissue shares under §251(g) as tokenized shares even if they weren’t tokenized before, as long as the tokenized shares are identical in all the important respects like rights, voting powers, etc. to the original shares. this is explained in §251(g)(2).

“Since §251(g) allows for a holding company reorganization where the new parent issues shares that mirror the originals, the holding company can adopt a blockchain-based stock ledger for its issuance process. This doesn’t violate the “identical” requirement because the form of record-keeping (traditional vs. blockchain) is administrative, not substantive—much like switching from certificated to uncertificated shares, which Delaware law expressly supports.”

hang on now.. do you remember the S-3 that was filed in May 2024, defining digital assets inside of the sale agreement contract between GME and Jefferies? for their share offering?

GameStop’s current corporate structure looks like this: GameStop Corp (parent) holding company → GameStop Inc (subsidiary) that manages retail operations. the shares are issued for ownership of the parent company. important to understand that the legacy business is managed by a subsidiary.

what if in the future GameStop wanted to maintain the brand identity for their retail business as the premier destination for how to spend your leisure time, but wanted to have a new name for their investment behemoth diversified holding company.. like Teddy?

they could:

• acquire a company that they find undervalued or owning an asset they would want;

• place it as a subsidiary of GameStop Corp;

• perform a Section 251(g) corporate reorganization;

• and name it whatever they want.

then it becomes Teddy (probably) → GameStop Corp → GameStop Inc.

you may be wondering why? ..well, tell me why shares of GME were labelled new class in 2024? kidding aside, this allows GameStop Corp to keep its current roles: strategic oversight, capital allocation, governance.. the investment policy.., and allows a new parent corporation to be formed to hold all of the acquisitions made by a dying, brick and mortar retailer-turned-investment fortress, managed by big dog and friends. and! it does not require a shareholder vote.

that could explain Section 4 of the warrant agreement, specifically why they chose to include legal definitions around a “Share Exchange Event” in the event of a reorganization:

it would explain the “new class” anomaly observed in September 2024 (or it was a private placement);

it would explain why the ATM agreement would require GME and Jefferies to have explained digital assets in a contract only to do with selling of their shares;

and lastly, it could explain why RC is so confident in his interviews with the news media.

talk about exciting times.

n.b.—this is just my personal opinion and fun speculation.](https://pbs.twimg.com/media/HAQNxnxXkAAqAtk.jpg)

![jake2b's tweet photo. what if the ace up the sleeve for $GME is not about the actual acquisition, but what happens after the acquisition? what if it is Delaware Law Title 8, Chapter 1, Subchapter IX. Merger, Consolidation or Conversion.

specifically §251(g)?

like many I was surprised to see RC doing the media tour and for the first time, hyping how big their plans will be. I mentioned before that a likely explanation could be they are doing a roadshow for an upcoming traditional bond offering. I also couldn’t help but worry when I read some snippets:

“it's gonna be really big. Really big. Very, very, very big," Cohen said of the size of the acquisition.”

“this is something that really has never been done before within the history of the capital markets.”

“it has the "potential to make [GameStop] worth several hundreds of billions of dollars.”

..because no matter what the Board was planning, the market could make this the largest sell-the-news event in history to try and curb their momentum and sentiment around the pivot of GameStop into a holding company.

why would big dog do that? why would he not say basically anything for 5 years then suddenly risk shooting himself in the foot by making grandiose claims about their first acquisition? lets not overlook that in the CNBC article he claims this one acquisition could propel the market cap of the company to the extent his entire pay package vests..

it got me thinking about why he would be so confident. then I found §251(g):

“Delaware General Corporation Law Section 251(g) allows a corporation to reorganize into a holding company structure without requiring a stockholder vote. This statutory provision facilitates mergers with a wholly-owned subsidiary, ensuring the holding company has the same charter provisions as the original corporation, often used for corporate restructuring or, historically, for adopting anti-takeover measures.”

emphasis mine. it is mainly used to create a new, top-level holding company where the original parent corporation used to be. That old parent co becomes a subsidiary and shareholders receive identical shares in the new holding company.

“Section 251(g) facilitates a holding company reorganization merger where outstanding shares of the original corporation are automatically converted into equivalent shares of the new holding company upon the merger’s effective time, provided all statutory conditions are met (e.g., identical rights and no tax recognition). This conversion is seamless and does not require surrendering or recalling physical certificates or shares,..”

hang on.. I know exactly what I thought of when I read that. do you remember this?

this sure provides a convenient explanation. oh, I can already hear the naysayers.. upon the merger's effective time. do you now remember what happened immediately before September 2024? the Board closed their credit facility and less than one month later, a pre-negotiated, pre-settled agreement was filed by the FTC.

I wrote at the time that I believed the Company applied to the FTC for a pre-merger certificate, hence why the settlement came out when it did and that the issuance of the certificate occurred after the second, 30-day review period following the filing of RC's settlement of the FTC violation. that is why he tweeted "yolo" exactly 60 days after the application for the certificate, because he got it.

OK back on topic. guess what else?

if they want to, a company can reissue shares under §251(g) as tokenized shares even if they weren’t tokenized before, as long as the tokenized shares are identical in all the important respects like rights, voting powers, etc. to the original shares. this is explained in §251(g)(2).

“Since §251(g) allows for a holding company reorganization where the new parent issues shares that mirror the originals, the holding company can adopt a blockchain-based stock ledger for its issuance process. This doesn’t violate the “identical” requirement because the form of record-keeping (traditional vs. blockchain) is administrative, not substantive—much like switching from certificated to uncertificated shares, which Delaware law expressly supports.”

hang on now.. do you remember the S-3 that was filed in May 2024, defining digital assets inside of the sale agreement contract between GME and Jefferies? for their share offering?

GameStop’s current corporate structure looks like this: GameStop Corp (parent) holding company → GameStop Inc (subsidiary) that manages retail operations. the shares are issued for ownership of the parent company. important to understand that the legacy business is managed by a subsidiary.

what if in the future GameStop wanted to maintain the brand identity for their retail business as the premier destination for how to spend your leisure time, but wanted to have a new name for their investment behemoth diversified holding company.. like Teddy?

they could:

• acquire a company that they find undervalued or owning an asset they would want;

• place it as a subsidiary of GameStop Corp;

• perform a Section 251(g) corporate reorganization;

• and name it whatever they want.

then it becomes Teddy (probably) → GameStop Corp → GameStop Inc.

you may be wondering why? ..well, tell me why shares of GME were labelled new class in 2024? kidding aside, this allows GameStop Corp to keep its current roles: strategic oversight, capital allocation, governance.. the investment policy.., and allows a new parent corporation to be formed to hold all of the acquisitions made by a dying, brick and mortar retailer-turned-investment fortress, managed by big dog and friends. and! it does not require a shareholder vote.

that could explain Section 4 of the warrant agreement, specifically why they chose to include legal definitions around a “Share Exchange Event” in the event of a reorganization:

it would explain the “new class” anomaly observed in September 2024 (or it was a private placement);

it would explain why the ATM agreement would require GME and Jefferies to have explained digital assets in a contract only to do with selling of their shares;

and lastly, it could explain why RC is so confident in his interviews with the news media.

talk about exciting times.

n.b.—this is just my personal opinion and fun speculation.](https://pbs.twimg.com/media/HAQNxnvWIAA3DqV.jpg)

![jake2b's tweet photo. I was reading through old $BBBYQ SEC filings and came across something that really stood out. whatever the intentions of the affiliates and/or Purchaser, the assets had to have been secured at the end of 2022 in some way.

think back to the private bond exchanges; there was first a single investor, then an institutional group that followed by retiring their bonds for shares some time between November 14 and December 6, 2022. here is what I had never caught before:

[image 1]

thanks to accounting requirements there is disclosure in the 10-Q that the exchange was performed under what is called a "troubled debt restructuring". that can only be used under very specific circumstances, say if a company discloses that it may not be able to continue as a going concern. if we dive into the math on the deal we will see that whoever participated in the exchange was friendly to the company. here's why:

[image 2]

the aggregate principal amount retired through the bond exchange:

69.0 (2024) + 15.3 (2034) + 70.2 (2044) = 154.5 million dollars worth of bond debt.

[image 3]

but investors only received:

first Form D: 2,762,444 shares which was an offering amount of 10,331,540$;

second Form D: 11,667,021 shares which was an offering amount of 40,717,903$;

10,331,540 + 40,717,903 = 51,049,443$.

[image 3]

154.5 million of debt was retired in exchange for 51 million dollars’ worth of shares. the bond holders exchanged at 0.33 on the dollar when they could have just sold them on the open market at the time for a better return plus the individual investor gave the Company another 3.5 million dollars cash for 0.9 million additional shares.

the Company obviously benefitted tremendously from this deal, recording a 94.4 million dollar gain (the net difference) on their 10-Q. who would do that? the only way it makes sense is if the former bond, then equity holders received something more than just the shares in return. the only alternative explanation is preferring to lose money over open market sales to help the Company.

[image 4]

fun little side fact, looking at the TSO from the 10-Q (which was late!) if you look at the share amount received by the institutional group they total 9.9444% ownership, just under 10% with no way to round up to 10% and be labelled an insider. two more fun facts, the Company filed that their 10-Q was going to be late on the same day the bond exchange was finally terminated with no more extensions, and, the "troubled debt restructuring" was only revealed in the 10-Q itself, over a month later.

to summarize: no investor retires their senior, secured debt instrument for junior, unsecured equity at a loss compared to open-market price to help the Company's balance sheet, unless they got something in return. this exchange retired 25% of all 2024 bonds, an imminent insolvency risk at the time.

so.. what did they get?](https://pbs.twimg.com/media/HJQ4-CFW4AAl4Xu.jpg)

![jake2b's tweet photo. what if the ace up the sleeve for $GME is not about the actual acquisition, but what happens after the acquisition? what if it is Delaware Law Title 8, Chapter 1, Subchapter IX. Merger, Consolidation or Conversion.

specifically §251(g)?

like many I was surprised to see RC doing the media tour and for the first time, hyping how big their plans will be. I mentioned before that a likely explanation could be they are doing a roadshow for an upcoming traditional bond offering. I also couldn’t help but worry when I read some snippets:

“it's gonna be really big. Really big. Very, very, very big," Cohen said of the size of the acquisition.”

“this is something that really has never been done before within the history of the capital markets.”

“it has the "potential to make [GameStop] worth several hundreds of billions of dollars.”

..because no matter what the Board was planning, the market could make this the largest sell-the-news event in history to try and curb their momentum and sentiment around the pivot of GameStop into a holding company.

why would big dog do that? why would he not say basically anything for 5 years then suddenly risk shooting himself in the foot by making grandiose claims about their first acquisition? lets not overlook that in the CNBC article he claims this one acquisition could propel the market cap of the company to the extent his entire pay package vests..

it got me thinking about why he would be so confident. then I found §251(g):

“Delaware General Corporation Law Section 251(g) allows a corporation to reorganize into a holding company structure without requiring a stockholder vote. This statutory provision facilitates mergers with a wholly-owned subsidiary, ensuring the holding company has the same charter provisions as the original corporation, often used for corporate restructuring or, historically, for adopting anti-takeover measures.”

emphasis mine. it is mainly used to create a new, top-level holding company where the original parent corporation used to be. That old parent co becomes a subsidiary and shareholders receive identical shares in the new holding company.

“Section 251(g) facilitates a holding company reorganization merger where outstanding shares of the original corporation are automatically converted into equivalent shares of the new holding company upon the merger’s effective time, provided all statutory conditions are met (e.g., identical rights and no tax recognition). This conversion is seamless and does not require surrendering or recalling physical certificates or shares,..”

hang on.. I know exactly what I thought of when I read that. do you remember this?

this sure provides a convenient explanation. oh, I can already hear the naysayers.. upon the merger's effective time. do you now remember what happened immediately before September 2024? the Board closed their credit facility and less than one month later, a pre-negotiated, pre-settled agreement was filed by the FTC.

I wrote at the time that I believed the Company applied to the FTC for a pre-merger certificate, hence why the settlement came out when it did and that the issuance of the certificate occurred after the second, 30-day review period following the filing of RC's settlement of the FTC violation. that is why he tweeted "yolo" exactly 60 days after the application for the certificate, because he got it.

OK back on topic. guess what else?

if they want to, a company can reissue shares under §251(g) as tokenized shares even if they weren’t tokenized before, as long as the tokenized shares are identical in all the important respects like rights, voting powers, etc. to the original shares. this is explained in §251(g)(2).

“Since §251(g) allows for a holding company reorganization where the new parent issues shares that mirror the originals, the holding company can adopt a blockchain-based stock ledger for its issuance process. This doesn’t violate the “identical” requirement because the form of record-keeping (traditional vs. blockchain) is administrative, not substantive—much like switching from certificated to uncertificated shares, which Delaware law expressly supports.”

hang on now.. do you remember the S-3 that was filed in May 2024, defining digital assets inside of the sale agreement contract between GME and Jefferies? for their share offering?

GameStop’s current corporate structure looks like this: GameStop Corp (parent) holding company → GameStop Inc (subsidiary) that manages retail operations. the shares are issued for ownership of the parent company. important to understand that the legacy business is managed by a subsidiary.

what if in the future GameStop wanted to maintain the brand identity for their retail business as the premier destination for how to spend your leisure time, but wanted to have a new name for their investment behemoth diversified holding company.. like Teddy?

they could:

• acquire a company that they find undervalued or owning an asset they would want;

• place it as a subsidiary of GameStop Corp;

• perform a Section 251(g) corporate reorganization;

• and name it whatever they want.

then it becomes Teddy (probably) → GameStop Corp → GameStop Inc.

you may be wondering why? ..well, tell me why shares of GME were labelled new class in 2024? kidding aside, this allows GameStop Corp to keep its current roles: strategic oversight, capital allocation, governance.. the investment policy.., and allows a new parent corporation to be formed to hold all of the acquisitions made by a dying, brick and mortar retailer-turned-investment fortress, managed by big dog and friends. and! it does not require a shareholder vote.

that could explain Section 4 of the warrant agreement, specifically why they chose to include legal definitions around a “Share Exchange Event” in the event of a reorganization:

it would explain the “new class” anomaly observed in September 2024 (or it was a private placement);

it would explain why the ATM agreement would require GME and Jefferies to have explained digital assets in a contract only to do with selling of their shares;

and lastly, it could explain why RC is so confident in his interviews with the news media.

talk about exciting times.

n.b.—this is just my personal opinion and fun speculation.](https://pbs.twimg.com/media/HAQNxohWoAAxOAO.jpg)