It's pretty astonishing to see how RWA vaults went parabolic while the rest of DeFi was affected by attacks.

It makes sense, since assets in DeFi are composable across protocols as collateral, which creates a domino effect. In situations like what we saw in April, or the Bybit attack last year, composability was more of a 'curse' than a feature.

That said, we strive to create composability for RWA assets as well, from an interoperability perspective. And the one and only, most important x factor for this type of growth is SECURITY.

Projects must prioritize security over hype, marketing, and team growth. If you're in DeFi and you want to attract institutional players, you must rethink your priorities wisely. The growth numbers, when you prioritize correctly, speak for themselves, and we've seen this throughout the smart moves risk curators and DeFi asset managers have been making over the last year.

One of the movements that's been exciting me lately is the rise of local blockchain talent here in Israel.

I had the privilege of being invited to speak about Neo-Finance at Blockchain B7, a student organization at Ben-Gurion University of the Negev, one of Israel's "Ivy League" institutions.

I met a group of seriously talented people who've decided they want to understand blockchain deeply, and with their entrepreneurial, innovative mindset, they've built an ecosystem of forward-thinkers aiming to push Israel ahead in this industry.

Thank you again to Amit Shilo, Noam Jehoshua, and Ben Etedgi for taking on this incredible endeavor, for inviting me, and for being that rare intersection of kindness and brilliance. It was a pure pleasure and an amazing experience.

SEC Commissioner Hester Peirce just clarified that tokenization rules will only apply to real, asset-backed securities.

No synthetic stock tokens.

No fake representations.

Regulated tokenized markets are getting closer.

By the end of the day, the cleanest way for tokenizing real-world assets is to tokenize assets that have a financial structure that makes sense.

What makes sense? deep liquidity, security, and easy redemption. liquid assets make more sense because they are compatible on the blockchain and can be utilised in defi. And that's what makes the real difference.

Any asset class that is not liquid enough is currently under wishful thinking till we figure out the right financial and legal structure to make them more 'tradable'.

Different categories of tokenized assets have scaled at very different rates.

Asset-backed credit hit $1 billion in market cap in just 185 days. Specialty finance crossed the same threshold in under two years.

At the other end of the spectrum, venture capital took more than seven years to reach $1 billion, while active strategies took nearly as long.

More complex structures with longer time horizons take more time.

@emilylai@kaledora@Ostium An incredible project to join. met the founders back in 2025 at the RWA summit in NY, and they are definitely a rare combination of geniuses who also understand people and growth mechanisms. Best of luck!

America should lead the future of finance, not watch innovation move offshore.

The CLARITY Act gives digital assets clear rules, protects consumers, and keeps the U.S. the financial center of the world.

Now let’s pass it on the Senate floor and send it to @POTUS’s desk.

The SEC's tokenized stock exemption is reportedly out this week, and it already exposed something the headlines are mostly missing.

Everyone's reading this as "crypto wins, stocks go onchain." Fine. But the real argument is between two groups who both want tokenization and disagree on one thing: does the company being tokenized get a say?

@Securitize say yes. Their argument, via Securitize's president Brett Redfearn: if a third party can tokenize Apple or Amazon without the issuer involved, there's no cap on how many versions of that company exist at the same time, and investors stop knowing what a share is even worth.

The crypto-native side says no. The point of this whole thing is cutting out middlemen, DTCC included. Issuer consent is just the old permission structure wearing a new outfit.

I think the crypto-native side is right about the goal and wrong about the mechanism. Here's the part of their argument that doesn't hold:

They treat "no DTCC" and "no issuer consent" as one fight. There are two. DTC's own pilot already settles transfers directly on the investor's chosen chain, atomically, around the clock. Atomic settlement, self-custody, 24/7, all of it works inside a consented model.

So when they defend permissionless issuance, they aren't defending faster/better settlement.

They already have that. They're defending the right to mint a claim on a company that never agreed to it.

Strip the "freedom from middlemen" framing away, and that's what's actually left on the table. It's a much weaker thing to plant a flag on.

And watch what the regulator is doing.

The draft reportedly forces third-party tokens to carry real voting rights and dividends, or get delisted.

Read that closely.

The SEC is patching the wrapper problem before the thing even ships. You don't write that rule if permissionless wrappers were clean.

Here's my actual read, and why I hold it:

A natively issued token is the share. A third-party wrapper is a separate instrument: a claim on the share, with counterparty risk tied to whoever minted it, and redemption terms that can differ from the next platform's wrapper of the same stock.

Those are not the same assets. An institution can take the first onto its books with one legal answer to "what is this?" The second forces it to price extra risk for zero extra return. So mostly, it just won't.

That matters because of who tokenization is actually courting. This isn't a retail story.

The capital in play is institutional, and that capital does not buy ambiguity.

It's not theoretical either.

Securitize already tokenizes funds for BlackRock, Apollo, and VanEck, with BlackRock's $BUIDL the largest tokenized real-world asset in the world.

Those names didn't show up for "permissionless." They showed up because the claim is clean and the issuer is in the room. That's the tell.

The model that wins isn't the one with the best decentralization story. It's the one a treasury desk can underwrite without guessing what it owns.

Fair counterpoint, and I won't skip it: permissionless issuance means building without asking anyone, and that's genuinely produced most of crypto's good ideas. A consent regime does hand licensed incumbents a gate, and that's a real cost.

But this launches as a limited pilot with guardrails, and whatever model works under those conditions becomes the default for the next decade.

My bet is on the consented model.

Because it's the only version institutional money can actually trust.

April 2026 was the bloodiest month in crypto hacks history.

In my video, I break down what happened and what it means if you're in DeFi, a fintech, or a bank moving into digital assets.

The facts:

→ April saw the highest number of separate exploits DefiLlama has ever recorded in a single month, with losses above $600M .

→ Two attacks drove most of it: Drift ($285M) and KelpDAO ($292M).

→ TRM Labs attributes 76% of all 2026 crypto-hack losses to North Korea, money the UN and US Treasury have long documented as funding the regime's weapons programs.

DPRK's cumulative crypto theft now exceeds $6B since 2017.

According to TRM Labs, North Korea has moved from hunting code vulnerabilities to hunting people’s vulnerabilities, running months of social engineering against the humans who hold the keys.

The responses from the involved projects and the DeFi community are worth your attention.

There was no government bailout. A coalition led by @aave , called 'DeFi United' and including @LidoFinance , @ether_fi , @Consensys , and others, coordinated the recovery, and by mid-May, the backing was being progressively restored.

And the infrastructure to defend against different attack vectors already exists: real-time detection (Hypernative), blockchain intelligence and tracing alongside law enforcement (Chainalysis, TRM Labs), and incident response and fund recovery (zeroShadow).

On regulation: on May 14, 2026, the CLARITY Act cleared the US Senate Banking Committee, a step toward holding digital-asset firms to anti-money-laundering standards comparable to banks.

The takeaway for operators: if you're building in crypto, your weak point isn't just your code, it's your people and who can move funds.

If you're a bank or fintech entering digital assets, the question isn't "is crypto safe," it's whether your exposure has the same detection, intelligence, and response solutions you already run everywhere else.

April wasn't proof that crypto is broken. It was proof of what gaps need to be closed to make the bridge between TradFi and DeFi safe to cross.

The defining crypto story of the last two weeks didn't come from a crypto company.

It came from a 79-year-old Wall Street asset manager.

Franklin Templeton acquiring 250 Digital and launching Franklin Crypto.

The detail most missed: Franklin is paying partially in BENJI, its own tokenized US Government Money Fund. Wall Street M&A settled on-chain.

That's one half of the story.

The other half is that three major financial regulators moved on stablecoin rules in the same window:

→ The FDIC published the framework for stablecoin issuers under the GENIUS Act

→ The HKMA issued Hong Kong's first stablecoin licenses, one to Standard Chartered, one of only three banks authorized to issue Hong Kong's paper currency

→ UBS, PostFinance, and a consortium of major Swiss banks launched a live sandbox for a regulated Swiss franc stablecoin

Distribution, supervised product, and regulated infrastructure all got built simultaneously.

On the 8th of April, 3 things happened on the same day:

→ Iran's Hormuz toll became public via FT, payable in Bitcoin, stablecoins, or yuan. Anything except actual US dollars.

→ Morgan Stanley launched the first spot Bitcoin ETF from a major US bank.

→ Circle launched a product letting banks settle in stablecoins.

A US investment bank. A US stablecoin issuer. A sanctioned state. Same infrastructure. Same day.

Here's the part most people miss:

Tether holds $141B in US Treasury exposure, making it one of the largest non-sovereign holders of US government debt worldwide.

So when Iran collects a toll in Tether, they're being paid in an asset anchored to debt issued by the country they're at war with.

The financial system is converging on rails that don't ask permission.

The question for financial leaders is no longer whether to adopt them; it is how.

It's who builds the compliance and trust layer that makes them defensible.

That's where the next era gets defined.

The brutal summary for someone building in NeoFi:

@Mastercard <> @BVNKFinance deal is a landmark.

It confirms stablecoin infra has moved from experimental to M&A-grade strategic asset. The yield instruments ($USYC/$BUIDL) show where institutional money is actually parking.

$BTC pump is noise. The Fed decision tomorrow is the real risk variable for everything.

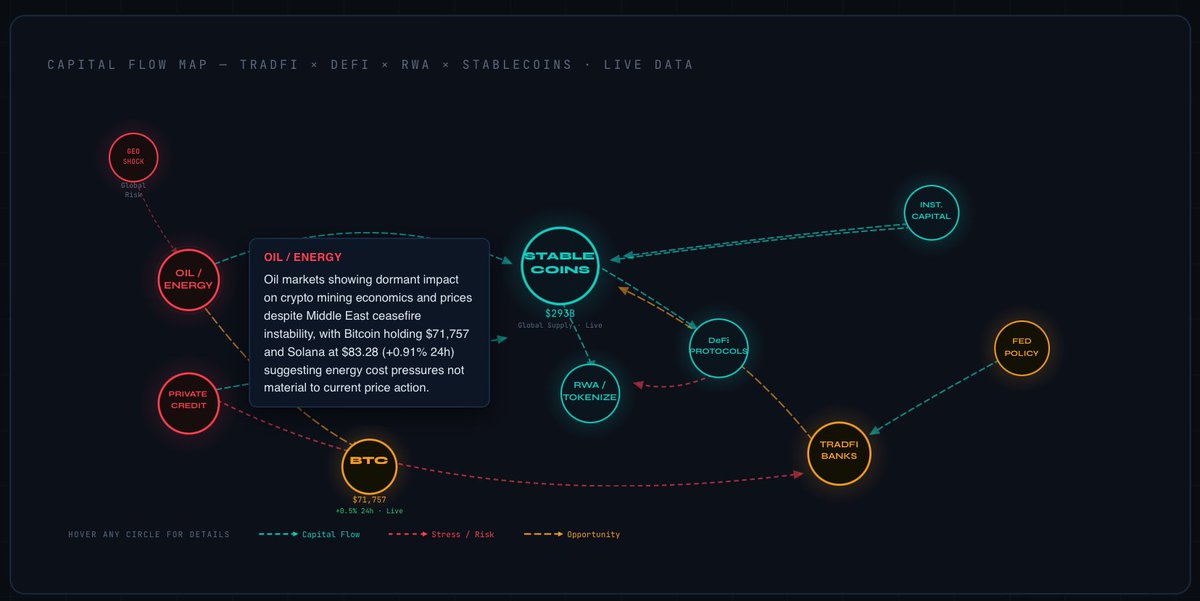

Here's what moved NeoFi in the last 24 hours:

Oil disruption > Dollar settlement cracks > on-chain dollar rails rise > Tradfi buys in (Mastercard).

The Iran war closed the Strait of Hormuz, cutting off ~20% of global oil supply and accelerating Asian buyers to settle energy trades in yuan rather than dollars (the petrodollar), cracking the payment rails that global commerce runs on.

That crack created an urgent need for a neutral, dollar-denominated alternative that moves fast and doesn't depend on traditional banking hours or geopolitical goodwill --> exactly what stablecoins are built for.

@circle's yield-bearing $USYC (tokenized money market fund backed by US Treasury bills, available only to non-US institutional investors) jumped 4.4% in a single day as money rotated into T-bill-backed on-chain instruments, and @BlackRock's $BUIDL kept growing.

The clearest validation came from @Mastercard , which paid $1.8B(!), the largest *stablecoin* acquisition in history, not to speculate on crypto, but to own the infrastructure that bridges fiat money and blockchain rails, because they can see the world fragmenting and they want to be the plumbing regardless of which currency wins.

When one of the most influential economists in the world writes a deep dive on tokenomics, blockchain fragmentation, and stablecoins → You want to pay attention.

The paper (BIS Working Paper No. 1335 by Hyun Song Shin - Economic Adviser and Head of Research at the Bank for International Settlements) walks through why blockchains are structurally fragmented systems.

The chain of logic is: higher security requires higher validator rewards > higher rewards require congestion fees > congestion pushes users to cheaper and less secure chains > and that migration is what causes fragmentation.

It's not a design choice. It's a structural consequence of how decentralized consensus works economically.

Hyun also argues that stablecoins inherit this fragmentation directly from the blockchain rails they sit on. USDC on Ethereum and USDC on Solana are, economically, different instruments. Different validator set, different liquidity pools, no native interoperability. Bridges introduce delay, cost, and hack risk.

The singleness of money, the very institutional feature that gives fiat its social value, is absent in blockchains.

I can't disagree with the technical argument. It's rigorous and largely correct.

But his proposed solution points toward a "unified ledger" anchored by a central bank, where tokenized central bank money, tokenized commercial bank deposits, and other digital assets coexist on a programmable platform.

Essentially, his suggestion reminds a CBDC framework. And that's where I push back.

If we go down that road, we undermine the very problem blockchain was built to solve: removing the middleman.

Creating an open, programmable economic layer that anyone can participate in, including the 1.4 billion unbanked people globally.

A central-bank-anchored ledger doesn't solve financial inclusion, it just digitizes the existing power structure.

And the privacy issue is crucial. There's no meaningful value in a "stablecoin" if the central bank has full traceability of every transaction and the identity behind it, beyond standard AML requirements. ZKP could theoretically help, but not at the scale and speed that the monetary system requires.

The paper is excellent. The diagnosis is right. The prescription is where it gets uncomfortable.

The question I'm left with is:

How do we achieve interoperability without sacrificing privacy?

4 stories drove the last 24 hours today. Here's how to read the map:

>> Story 1: Iran lit the match.

The Strait of Hormuz blockade pushed oil above $100/bbl. The classic playbook says: oil spikes → inflation → risk-off → crypto dumps. That didn't happen. Instead, emerging market investors (who fear dollar depreciation and local currency collapse more than anything) poured money into dollar stablecoins. Supply hit $314.67B, up over 1% in a single week. USDC is the specific winner: its share of the stablecoin market is climbing to 27% because institutional money prefers Circle's audited, transparent reserves over Tether's opacity when things get scary.

>> Story 2: BTC broke the script.

While the S&P fell, BTC gained 0.67% to $71,384. Spot ETFs absorbed $760M in inflows week-to-date despite active war news. This is a significant repricing moment: the market is starting to treat Bitcoin as a geopolitical hedge, closer to gold than to Nasdaq. On-chain data confirms it, with whale wallets reversing six weeks of distribution at the $71k level.

>> Story 3: The Fed picked a winner, and it changes everything.

Kraken received the first-ever crypto Fed master account, the same week Custodia lost its 7-to-3 appeals court battle after five years of fighting. This is not "crypto getting access to banking." This is the Fed hand-selecting one compliant, CEX-scale player and permanently locking out a crypto-native bank with no finding of wrongdoing. The message: only institutional-grade, fully audited players get dollar settlement rails. For everyone else, the door is closed.

>>Story 4: RWA protocols absorbed the rotation.

When oil spikes, institutional LPs don't sit in cash. They rotate into fixed income. Sky (formerly MakerDAO) TVL surged 38% in March by offering exactly that: T-bill and corporate bond yields on-chain, auditable, and compliant. It's now the 4th largest DeFi protocol. BlackRock $BUIDL sits at $2.52B. The pattern is clear: in a risk-off environment, on-chain yield beats DeFi speculation.

>> The connecting thread: compliance is the new moat.

Every winner today (USDC over USDT, Kraken over Custodia, Sky over speculative DeFi) won because of transparency and regulatory compatibility, not technology superiority.