Most retail investors in India buy stocks based on tips, social media, or gut feel.

We do it differently.

📊 Deep-dive research on small & mid-cap stocks

🎯 Specific buy/sell updates

🔐 SEBI-registered (INH100001690)

Serious about wealth creation? → https://t.co/a6uusXFC7V

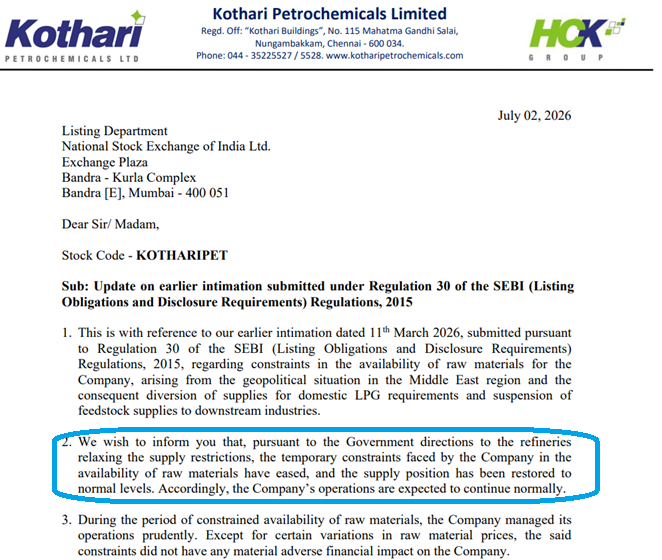

Feb 2026: Strait of Hormuz shuts. India's LPG supply collapses. Industrial feedstock suspended.

July 2026: Kothari Petrochemicals files on NSE —

"Supply position restored to normal. Operations expected to continue normally."

Research desk - https://t.co/WyQP2PZOrl

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

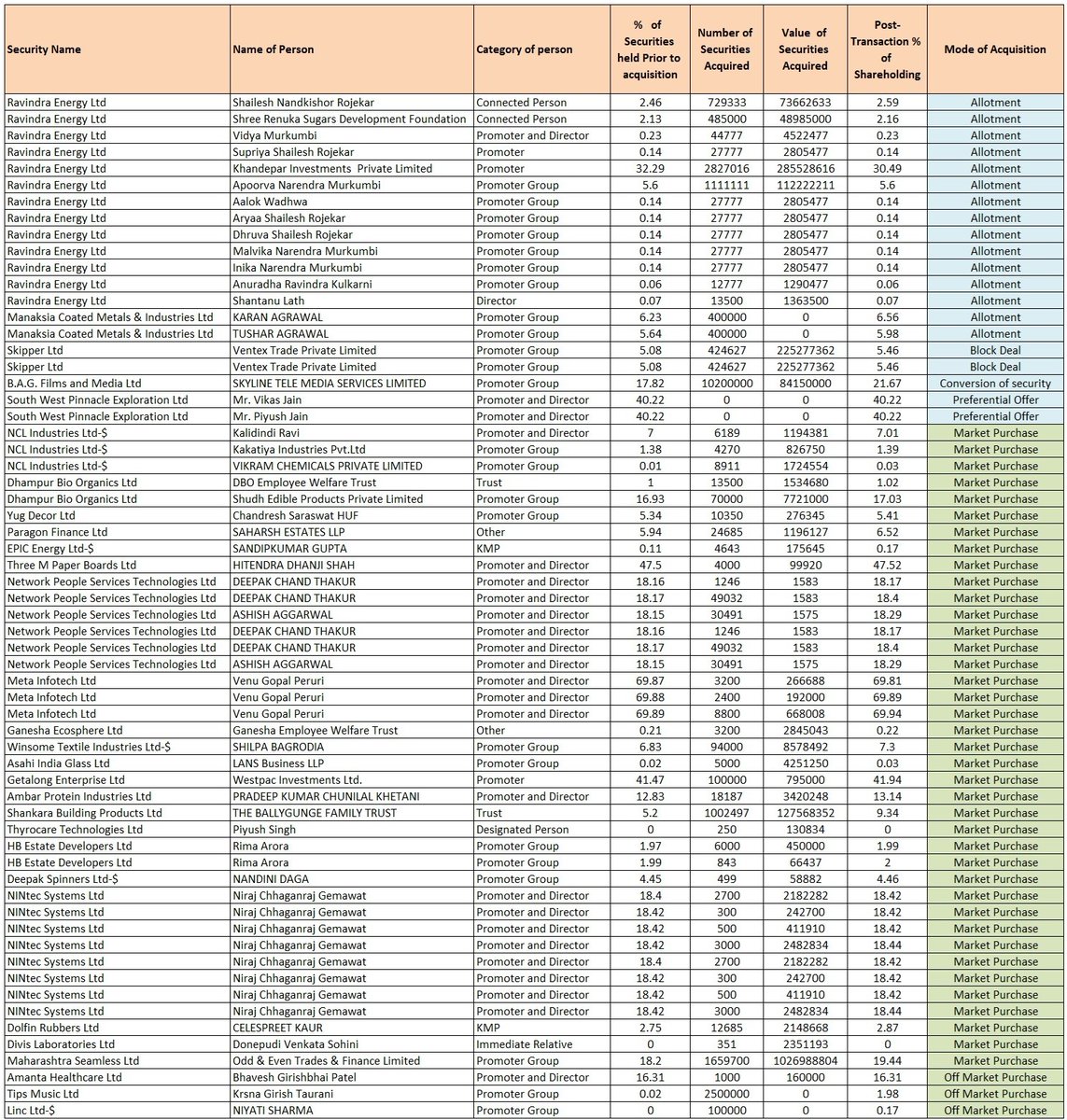

2 years ago, I tracked only open-market promoter buying

Ignored preferential allotments

Several multibaggers first signalled promoter conviction via preferential issues — long before prices moved

Tracking them early matters

Preferential allotments announced on 2nd Jul'26👇 (signals most investors overlook)

Research desk -> https://t.co/YnLe7uovTf

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

ADF Foods just disclosed something most people will scroll past: its US subsidiary received a $2.1 million (₹19.97 Cr) tariff refund from US Customs

Why? In Feb 2026, the US Supreme Court struck down Trump's IEEPA tariffs — including the 25% duty slapped on Indian exports over Russian oil purchases

The court ruled the President never had the authority to impose them in the first place. CBP is now refunding what was illegally collected — potentially $170Bn+ across all importers

Research desk - https://t.co/WyQP2Q0mgT

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

Went through today's insider buying data

A few names worth noting:

→ Ambar Protein — Promoter added 18,187 shares

→ Maharashtra Seamless — Promoter bought 16.59 lakh shares

All market purchases — open market buying

Note: Not a recommendation. Only used for filtering and further research on stocks

Research desk -> https://t.co/YnLe7up3IN

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690, BSE Enlistment No - 5114

The Cash Flow Trap Checklist

8SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690 Signs a Company's Profits Are Real — Or Aren't

1. PAT growing but Operating Cash Flow (OCF) flat or negative for 3+ years

→ The most reliable single check. Profits without cash generation = accounting, not business

2. CFO/PAT ratio below 0.5 consistently

→ For every ₹1 of reported profit, less than ₹0.50 arriving as cash. Watch over 3-5 years

3. Receivables growing 2x faster than revenue

→ Revenue is being "booked" but not collected. Classic channel stuffing sign

4. Inventory growing despite no revenue growth

→ Goods piling up. Either demand has slowed or revenue is being overstated

5. Loans & advances to subsidiaries/related parties growing every year

→ Cash leaving the company via balance sheet — not as dividends, not as capex. Red flag

6. Capitalising routine expenses as assets (intangibles rising disproportionately)

→ Expenses moved to balance sheet inflate current profit. Ask: what exactly is being capitalised?

7. Free Cash Flow negative while dividend is being paid

→ Dividends being funded by debt or asset sales. Unsustainable without external capital

8. "Other Current Assets" growing without explanation in notes

→ A parking lot for items that don't fit elsewhere. Read the notes — this line has hidden many skeletons

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

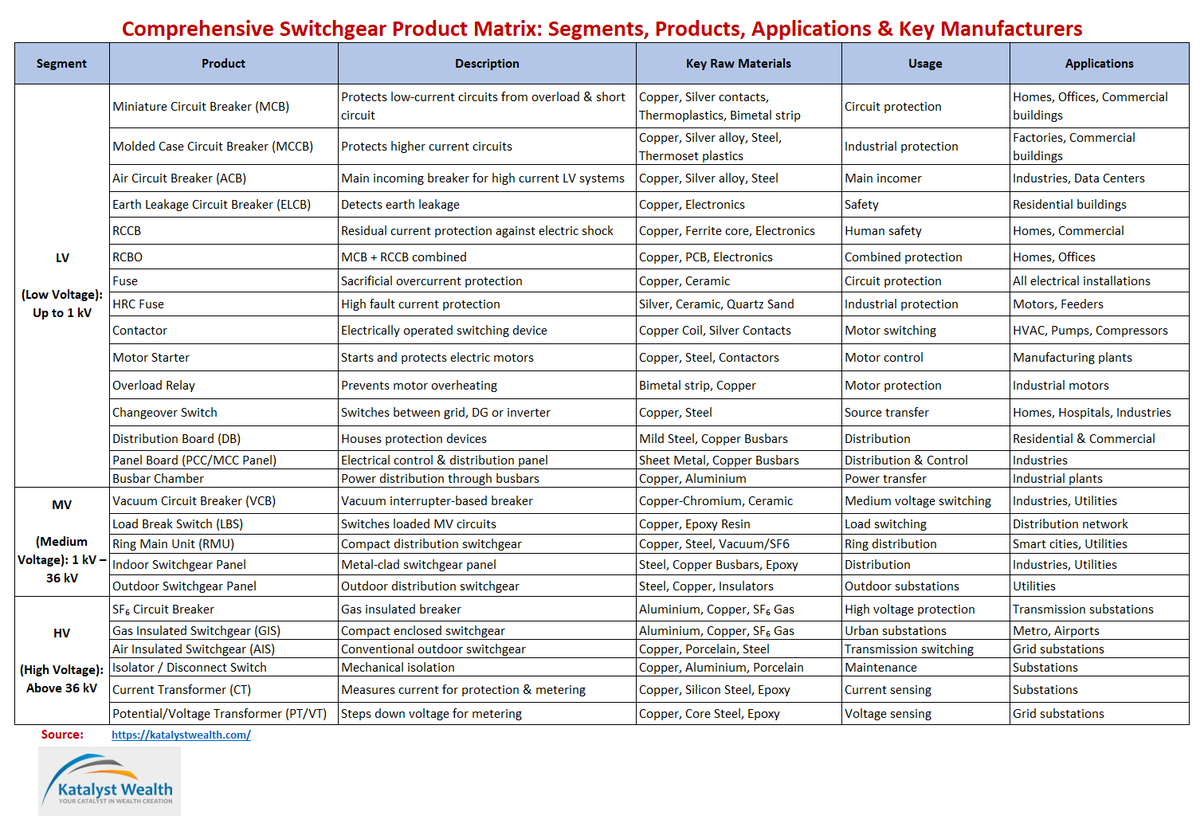

Everyone talks about power generation. Few pay attention to companies that actually control, protect and distribute electricity

From homes and factories to solar plants, data centers and metros—nothing runs without switchgear

Let's decode India's switchgear opportunity

(1/n)

Weekly wrap 🧵...2 small cap stock ideas Health X Platform and Pennar Industries

1) Health X Platform

India's pharma brands charge ₹107 for a tablet that costs ₹42

Health X Platform's private label JITO sells the same molecule at 60% discount — with 30-40% gross margins for itself

Just launched. ₹30 lakh/month in month 2

Watching this closely

Full notes - https://t.co/xCMigxv6dk

2) Pennar Industries

↗ Revenue: ₹3,666 Cr (+12%)

↗ PAT: ₹139 Cr (+16%)

↗ PAT margin: 3.83% (was 2% four years ago)

Management committed to 20% PAT growth in FY27

One thing to watch though — debt has crept up

Full notes: https://t.co/boehwmsTE5

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

Pennar Industries FY26:

↗ Revenue: ₹3,666 Cr (+12%)

↗ PAT: ₹139 Cr (+16%)

↗ PAT margin: 3.83% (was 2% four years ago)

Management committed to 20% PAT growth in FY27

One thing to watch though — debt has crept up

Full notes: https://t.co/boehwmsTE5

Went through today's insider buying data

A few names worth noting:

→ M K Exim — Promoter group added 89,000 shares

→ Best Agrolife — Promoter bought 89,582 shares

All market purchases — open market buying

Note: Not a recommendation. Only used for filtering and further research on stocks

Research desk -> https://t.co/YnLe7up3IN

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690, BSE Enlistment No - 5114

We have released detailed update on the following 2 stocks:

- Everest Kanto

- Panama Petrochem

Can check update (requires access) @ https://t.co/f1L2pLgm9f

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

India's pharma brands charge ₹107 for a tablet that costs ₹42

Health X Platform's private label JITO sells the same molecule at 60% discount — with 30-40% gross margins for itself

Just launched. ₹30 lakh/month in month 2

Watching this closely

Full notes - https://t.co/xCMigxv6dk

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

8 Signs Promoter Selling Is a Warning — Not Routine

This week: Check promoter shareholding across 4-8 quarters

It takes 10 minutes and free on BSE/NSE, Screener

If you find 3+ signs below → Dig deeper before the next quarterly result

1. Promoter stake down 2-3%+ in 12 months without open offer or buyback

→ Routine tax planning is 0.5-1%. Consistent reduction is a signal

2. Stake sold in small tranches — ₹5-10 crore each, every quarter

→ Designed to stay below block deal disclosure thresholds, stealth exit

3. Promoter pledging >50% of promoter holding

→ Already leveraged against shares they own. Margin calls = forced selling

4. Pledge % increasing every quarter even as stock price rises

→ Rising price should reduce pledge ratio. If it's still rising, new loans are being taken

5. Capex guidance given but promoters selling while "expansion" is ongoing

→ Promoters selling into a fundraise story while diluting retail confidence

6. Promoter group entity transfers between related parties before public sale

→ Reorganising before exit. Watch for "inter-se transfers" followed by market selling

7. Salary + sitting fees to promoter family rising faster than PAT

→ Extraction through the P&L rather than shareholding changes

8. Promoter not participating in rights issue

→ Dilution without contribution. Lets public shareholders fund growth while they step back

Research desk -> https://t.co/WyQP2Q0mgT

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

India's Digital Revolution is creating a silent mountain of e-waste

As smartphones, EV batteries, solar panels, and electronics reach end-of-life, the next big opportunity may lie with recyclers that can recover valuable metals from tomorrow's complex e-waste

🧵

(1/n)

Weekend task:

Most investors spend more time researching which restaurant to visit than reading the annual report of a stock they've put ₹2-3 lakhs into

This weekend, flip that around — 15 minutes per holding, 10 checks, one framework

Full portfolio audit - https://t.co/Yaqv4WWOoR

In 1916, France kept sending men to die at Verdun — not because it mattered strategically, but because enough men had already died there

The dead became the argument for sending more

Investors do the exact same thing with losing stocks

Once you've averaged down twice, the sunk cost owns you. You're no longer investing — you're vindicating past decisions

Buy an initial 3-5%. Let management execute. If they do, the stock earns a bigger allocation. If they don't, let it shrink and walk away

Victory often comes from what you refuse to do

Note: Inspired from an article by Ian Cassel

Went through today's insider buying data

A few names worth noting:

→ Aeroflex — Promoter group added 100,000 shares

→ MSP Steel — Promoter bought 38,25,000 shares

→ Premier Polyfilm — 95,000 shares

All market purchases — open market buying

Note: Not a recommendation. Only used for filtering and further research on stocks

Research desk -> https://t.co/YnLe7uovTf

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

Ecoreco's management on their 5-7 year capacity target:

"100,000 metric tons is achievable."

For context, current capacity is 31,200 MTPA

That's a 3x expansion being guided on a Q1 FY25 concall

Will be interesting to track

Research desk -> https://t.co/WyQP2Q0mgT

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690

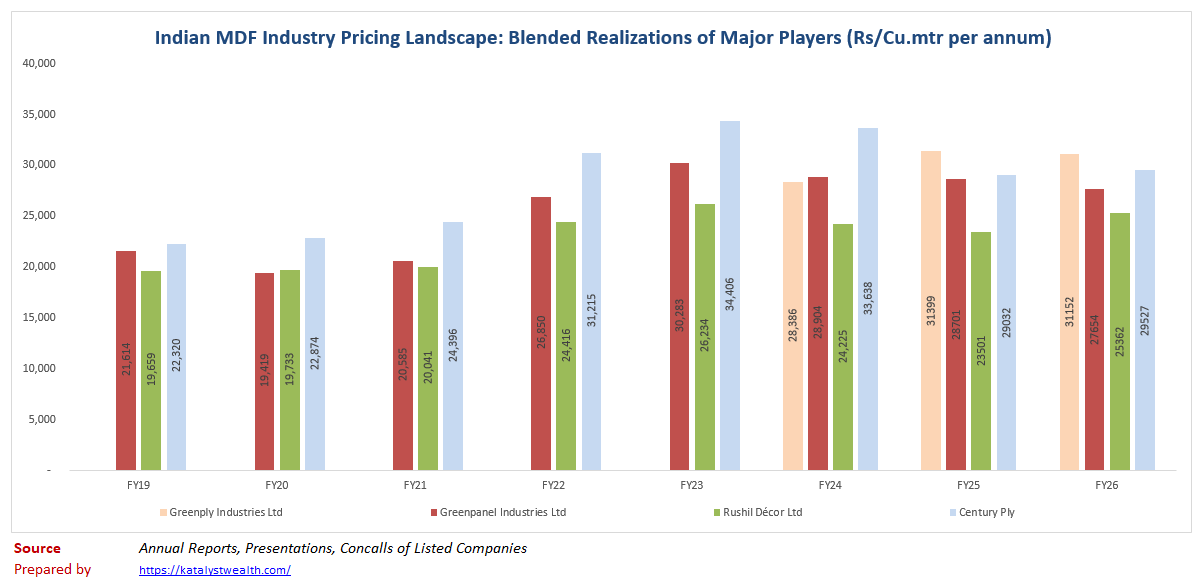

FY19: Century Ply had the highest MDF realizations among India's listed players, ₹22,320/cu.mtr

FY26: Greenply leads instead, at ₹31,152 vs Century's ₹29,527

7 years of pricing data on India's top 4 MDF makers

Chart below 👇

Research desk -> https://t.co/WyQP2Q0mgT

SEBI RA - Ekansh Mittal Proprietor Mittal Consulting, INH100001690