Hormuz era o trigger que faltava pro desinvestimento em comodities desde 2011.

Covid começou a hormuz acelerou.

O ciclo está ai, vai aposentar muita gente no EWZz

Mais informações: https://t.co/jpOZPAQOfS

Por outro lado, tudo isso está a ser um revival de old economy stocks. $NOK $CSCO até a $F em breakout mode.

Build, not bid

Depois de decadas a investir no que ja estava feito e a usufruir da infra que outroa construiram, e a contribuir para a financeirizacao da economia, por fim chega a conta para pagar. Os Hyperscalers querem construir datacenters e chegam à conclusão que nao existem objectos físicos suficientes para isso. Anos de easy money colocaram muito pouco dinheiro na economia real

https://t.co/e4FgLTjoiZ

O BRASIL ESTÁ DORMINDO NA REVOLUÇÃO!

Enquanto o Paraguai assina acordos em Taipei para atrair capital na revolução da inteligência artificial, o Brasil — a maior potência hidrelétrica do hemisfério — não estava nem na sala.

A corrida do século XXI não é por dados ou talento: é por energia limpa, abundante e barata. E nós temos tudo isso.

Três variáveis raras alinhadas pela primeira vez em gerações, uma janela geopolítica aberta, e trilhões de dólares buscando destino.

Mesmo assim, escolhemos ser espectadores. No próximo vídeo, os nomes dos responsáveis.

Porque a conta chegou e para a gente!

$BRSL Q1 2026 earnings: Superb Margin Execution, But a Balance Sheet Cliff Looms

Brightstar delivered a masterclass in cost control this quarter. While revenue was practically flat (+1% YoY) at $587M, Adjusted EBITDA surged 15% to $287M. The OPtiMa cost savings program is visibly dropping to the bottom line, expanding margins from 42.8% to 48.9%. However, investors must look past the operational beat: free cash flow fell 49% as capital expenditures ramped up, and an impending $1.67 billion Italy Lotto license payment will push FY26 operating cash flow deep into negative territory. Management is executing perfectly on what they can control, but 2026 will be a structurally messy transition year.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐌𝐚𝐫𝐠𝐢𝐧 𝐋𝐞𝐯𝐞𝐫𝐚𝐠𝐞 𝐢𝐬 𝐖𝐨𝐫𝐤𝐢𝐧𝐠 — The company proved it does not need massive top-line growth to drive earnings. OPtiMa cost efficiencies and G&A recoveries powered a 15% EBITDA jump on 1% revenue growth.

• 𝐒𝐭𝐫𝐨𝐧𝐠 𝐔𝐧𝐝𝐞𝐫𝐥𝐲𝐢𝐧𝐠 𝐒𝐚𝐦𝐞-𝐒𝐭𝐨𝐫𝐞 𝐒𝐚𝐥𝐞𝐬 — Despite headline FX headwinds, wager-based same-store sales grew in Italy (+3.1%) and the Rest of World (+5.8%), demonstrating continued player demand and product strength.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐓𝐡𝐞 𝟐𝟎𝟐𝟔 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐂𝐫𝐚𝐭𝐞𝐫 — The final €1.43B ($1.67B) payment for the Italy Lotto license in April 2026 will wipe out FY26 operating cash flow (guided to negative ~$900M) and spike leverage up to ~3.5x.

• 𝐋𝐚𝐠𝐠𝐢𝐧𝐠 𝐈𝐧𝐭𝐞𝐫𝐧𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐆𝐞𝐨𝐠𝐫𝐚𝐩𝐡𝐢𝐞𝐬 — Reported revenue in the Rest of World segment reversed to an 11% decline ($70M), and the U. K. contract transition continues to act as a sustained structural headwind on the top line.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. The core lottery engine is incredibly resilient and margins are accelerating, but the peak CapEx cycle and the massive Italy Lotto license payment will consume all near-term cash generation.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢🟢 𝐎𝐏𝐭𝐢𝐌𝐚 𝐂𝐨𝐬𝐭 𝐒𝐚𝐯𝐢𝐧𝐠𝐬 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐏𝐫𝐨𝐟𝐢𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲 [NEW]

The most important operational takeaway this quarter: Brightstar is getting leaner. The OPtiMa cost reduction program and disciplined G&A spending allowed a meager 1% increase in revenue to flow through to a 15% increase in Adjusted EBITDA. This operational leverage effectively insulates the bottom line against stagnant volume growth.

🟢 𝐔.𝐒. & 𝐂𝐚𝐧𝐚𝐝𝐚 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐋𝐞𝐚𝐝𝐬 𝐓𝐨𝐩-𝐋𝐢𝐧𝐞 𝐆𝐫𝐨𝐰𝐭𝐡

While overall revenue was sluggish, the U. S. and Canada segment provided the heavy lifting. Sales in the region accelerated, up 9% YoY to $281M, driven by favorable U. S. sales mix and reduced LMA shortfalls. It is the only geographic segment currently providing meaningful reported top-line expansion.

🔴 𝐇𝐞𝐚𝐝𝐥𝐢𝐧𝐞 𝐍𝐚𝐫𝐫𝐚𝐭𝐢𝐯𝐞 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐬 𝐑𝐞𝐩𝐨𝐫𝐭𝐞𝐝 𝐈𝐭𝐚𝐥𝐢𝐚𝐧 𝐑𝐞𝐚𝐥𝐢𝐭𝐲 [NEW]

The PR headline touts 'Revenue up on strong Italy performance.' This is highly misleading. Reported Italy revenue actually fell 4% YoY (from $246M to $236M). While wager-based same-store sales in Italy did grow 3.1% in constant currency, severe FX headwinds and higher service revenue amortization completely wiped out these operational gains on the P&L.

🔴 𝐓𝐡𝐞 𝐈𝐭𝐚𝐥𝐲 𝐋𝐨𝐭𝐭𝐨 𝐋𝐢𝐜𝐞𝐧𝐬𝐞 𝐋𝐞𝐯𝐞𝐫𝐚𝐠𝐞 𝐒𝐩𝐢𝐤𝐞

Brightstar's balance sheet is stable today (2.4x net debt leverage), but it is standing on the edge of a cliff. Management projects leverage will spike to ~3.5x pro forma following the €1.43B ($1.67B) final payment for the Italy Lotto license in April 2026. This limits capital flexibility heavily for the next 12 months.

🔴 𝐈𝐧𝐟𝐥𝐚𝐭𝐢𝐨𝐧𝐚𝐫𝐲 𝐏𝐫𝐞𝐬𝐬𝐮𝐫𝐞𝐬 𝐁𝐢𝐭𝐢𝐧𝐠 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧𝐬 [NEW]

Management explicitly flagged inflationary pressures impacting postage, freight, and other costs. While OPtiMa savings mitigated this at the EBITDA line, core service costs remain elevated. If inflation in physical ticket logistics persists, the company will have to lean even harder on digital volume to maintain margins.

🔴 𝐑𝐞𝐬𝐭 𝐨𝐟 𝐖𝐨𝐫𝐥𝐝 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠

The Rest of World segment was a distinct laggard, with revenue plunging 11% YoY to $70M (and down 18% in constant currency). The ongoing U. K. service contract transition continues to be a structural drag on international results, and management has not provided a clear timeline for when this headwind will fully roll off.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 (𝟐𝟔𝐐𝟏): $55 million

Decelerating sharply. FCF collapsed 49% YoY from $109M in 25Q1. This drop was driven by a heavy 45% increase in CapEx (up to $110M) as the company invests in contract renewals and systems, coupled with negative working capital timing.

𝐍𝐞𝐭 𝐃𝐞𝐛𝐭 (𝟐𝟔𝐐𝟏): $2.75 billion

Stable quarter-over-quarter, ticking up slightly from $2.72 billion in 25Q4. The company successfully refinanced its revolving credit facility out to March 2031 with improved terms, securing $1.6B in undrawn capacity to prepare for the massive upcoming Italy Lotto cash drain.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $2.50 - $2.55 billion

Stable. The reaffirmed guidance implies flat to ~2% YoY growth compared to FY25's $2.51B. Management noted this includes >5% organic growth, heavily offset by ~$175 million in incremental service revenue amortization related to the Italy Lotto license.

𝐅𝐘𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: $1.16 - $1.19 billion

Accelerating. Improving from $1.12B in FY25. Revenue growth and OPtiMa cost savings are expected to more than offset approximately $50 million of new investments in growth initiatives.

𝐅𝐘𝟐𝟔 𝐍𝐞𝐭 𝐂𝐚𝐬𝐡 𝐟𝐫𝐨𝐦 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐨𝐧𝐬: Negative ~$900 million

Reversing violently. The baseline business expects to generate ~$750M in operating cash, but the $1.67 billion (\u20ac1.43 billion) final payment for the Italy Lotto license completely overwhelms organic generation, causing a massive optical cash burn for the year.

𝐅𝐘𝟐𝟔 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐄𝐱𝐩𝐞𝐧𝐝𝐢𝐭𝐮𝐫𝐞𝐬: $450 - $475 million

Accelerating. A peak CapEx cycle continues, driven by contractual obligations tied to recent contract wins and system extensions. This elevated spend will further pressure standard Free Cash Flow metrics.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐏𝐨𝐬𝐭-𝐋𝐨𝐭𝐭𝐨 𝐃𝐞𝐥𝐞𝐯𝐞𝐫𝐚𝐠𝐢𝐧𝐠 𝐏𝐚𝐭𝐡

With leverage guided to spike to 3.5x after the April 2026 Italy Lotto payment, what is the specific timeframe and mathematical path to return leverage below your 3.0x long-term target?

𝐔𝐊 𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭 𝐓𝐫𝐚𝐧𝐬𝐢𝐭𝐢𝐨𝐧 𝐑𝐨𝐥𝐥-𝐨𝐟𝐟

The UK service contract transition remains a persistent drag on the Rest of World segment. In what specific quarter do you expect these difficult YoY comps to fully roll off?

𝐋𝐨𝐠𝐢𝐬𝐭𝐢𝐜𝐬 𝐚𝐧𝐝 𝐈𝐧𝐟𝐥𝐚𝐭𝐢𝐨𝐧 𝐌𝐢𝐭𝐢𝐠𝐚𝐭𝐢𝐨𝐧

You highlighted postage and freight inflation as an offset to EBITDA growth. Are you structurally redesigning your physical distribution networks, or simply relying on OPtiMa G&A cuts to subsidize these variable cost increases?

$VNOM: Viper is shaping up as a “defensive growth” Permian royalty vehicle, capturing revenue off the top with 80%+ cash margins and minimal cost inflation exposure. Q3 showed scale benefits post-Sitio, with a big adjusted EPS beat and strong CAFD-driven payouts. A $670M non-Permian sale could speed deleveraging toward the $1.5B target and a 100% CAFD payout trigger. With 2026 oil and water-disposal rules looming, is the risk/reward mispriced?

🎯 Get the free VNOM deep-dive (with audio):

https://t.co/DTNqyzsm8k

O mercado olha para a Warrior e vê uma empresa cara e eu diria que está a olhar para os números errados.

Em 2024 e 2025, a Warrior estava a construir o Blue Creek... uma mina de 1B de dólares, financiada inteiramente com cash flow operacional, sem um cêntimo de dívida. O resultado? Os números reportados ficaram distorcidos durante todo o período de construção. FCF aparentemente baixo. Múltiplos aparentemente elevados. Tudo contabilisticamente correcto. Tudo analiticamente enganador.

O FCF real de 2024, ajustando o capex de crescimento do Blue Creek, foi positivo em mais de 260 milhões... um yield de mais de 10% ao preço atual.

Com o Blue Creek agora operacional, a produção sobe 75%. Os custos descem. O capex de crescimento desaparece. E a Warrior, com o carvão metalúrgico nos 220 dólares e produção guiada para 13 megatoneladas em 2026, pode gerar mais de 500 milhões em cash flow operacional... com volume de negócios acima dos 2B. Face a uma capitalização de 4,5B, o cash flow yield implícito é muito relevante.

A Goldman Sachs confirma que o custo marginal do 90º percentil da produção mundial está nos 240 dólares por tonelada. Estamos no suporte estrutural do mercado... não num pico.

Análise completa no link. 👇

https://t.co/OE9erquclB

HP Inc. $HPQ is transforming from a traditional hardware manufacturer into a modern enterprise fueled by AI-integrated computing systems and high-margin printing subscriptions. The company is aggressively targeting a massive commercial hardware refresh cycle driven by the transition to Windows 11 and the rising demand for localized artificial intelligence processing. Despite facing temporary margin pressures from surging memory component costs, the underlying business remains a highly resilient powerhouse that produces roughly three billion dollars in annual free cash flow. Trading at a significant discount to historical valuation multiples while offering a dividend yield above six percent, management is consistently using this capital to repurchase its undervalued shares. Can this powerful combination of deep intrinsic value and strategic technological positioning successfully overcome the current macroeconomic headwinds and shift the broader market's bearish sentiment?

Charter Communications $CHTR operates a massive broadband and mobile network infrastructure that serves as a critical pillar of digital connectivity across the United States. The stock is currently trading at deeply discounted trough valuations as the market fixates on peak capital expenditures and near-term residential subscriber losses. However, this pessimistic sentiment ignores a massive anticipated inflection in free cash flow that is projected to materialize once the current multi-year network evolution cycle concludes. Will this aggressive pivot toward converged connectivity be enough to neutralize fierce competition from fiber overbuilders and unlock long-term shareholder value?

The S&P 500 is offering one of the lowest dividend yields in nearly 150 years.

At the same time, it’s trading at one of the richest cyclically adjusted P/E ratios in history.

Ask yourself:

What’s the actual upside you’re being compensated for at these levels?

I’d much rather Invest in LatAm equities.

Higher dividends, far more attractive valuations, and, in my view, significantly better underlying growth potential.

https://t.co/nXYpmlaw3m

H/t to @DailyReckoning

Se o sp500 cair 50% (que é totalmente plausível dado duration bizarra atual) seus retornos nele desde 2016 são apagados.

Sao 10 anos. Esse é o risco de não entender duration, e também de achar que é só magicamente comprar um índice.

O índice reduz o risco de distoar dele mesmo mas não te exime do risco dos ativos dentro dele.

Few.

@siyul You're pricing it wrong. YPF was just the icing on the cake in this case. Even losing on appeals court, $BUR is worth several times more than $4/share. The market is offering a unique opportunity for those who can see even a little ahead.

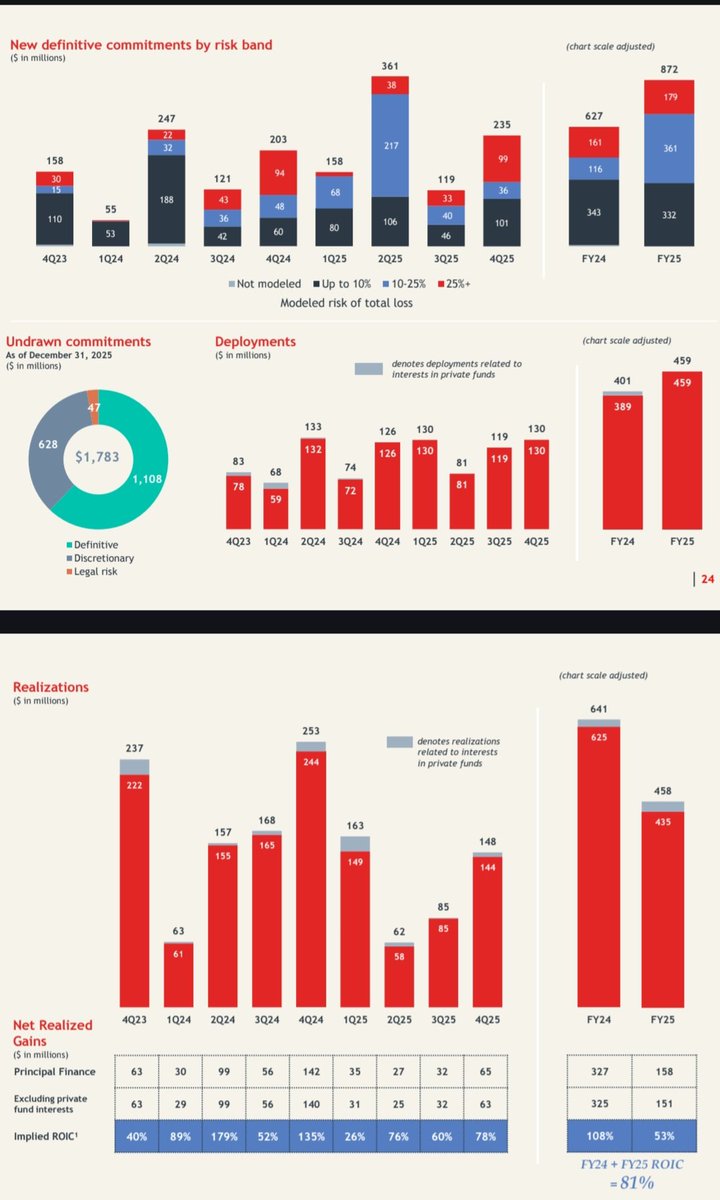

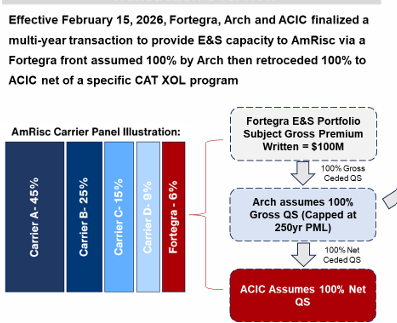

$ACIC $CB $UVE $HRTG

American Coastal buying back their stock is a great sign.

They have done the special dividend each year at the end of the year and that is my favorite use of their cash, but to buy 1% of their float in a single transaction opportunistically tells me they are now in a position to put capital to work, vs a few years ago being on the verge of death.

The easy math here is the legacy insurance firm is worth $20-$25, the new MGA is $7-$10 of value, the E&S is hard to value right now so just being cautious we will call it a $0 so, you are getting their 6% co part with AmRisc and ACES plus the MGA and half the insurance firm for nothing.

@PedroSegolin Estabilidade na moraria ( importante principalmente na velhice) e hedge do custo de moradia. Nao comprar no impulso e sem planejamento. Acrescentaria se possível. Alocar mo máximo 30/40% do PL.

![Finsee_main's tweet photo. $BRSL Q1 2026 earnings: Superb Margin Execution, But a Balance Sheet Cliff Looms

Brightstar delivered a masterclass in cost control this quarter. While revenue was practically flat (+1% YoY) at $587M, Adjusted EBITDA surged 15% to $287M. The OPtiMa cost savings program is visibly dropping to the bottom line, expanding margins from 42.8% to 48.9%. However, investors must look past the operational beat: free cash flow fell 49% as capital expenditures ramped up, and an impending $1.67 billion Italy Lotto license payment will push FY26 operating cash flow deep into negative territory. Management is executing perfectly on what they can control, but 2026 will be a structurally messy transition year.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐌𝐚𝐫𝐠𝐢𝐧 𝐋𝐞𝐯𝐞𝐫𝐚𝐠𝐞 𝐢𝐬 𝐖𝐨𝐫𝐤𝐢𝐧𝐠 — The company proved it does not need massive top-line growth to drive earnings. OPtiMa cost efficiencies and G&A recoveries powered a 15% EBITDA jump on 1% revenue growth.

• 𝐒𝐭𝐫𝐨𝐧𝐠 𝐔𝐧𝐝𝐞𝐫𝐥𝐲𝐢𝐧𝐠 𝐒𝐚𝐦𝐞-𝐒𝐭𝐨𝐫𝐞 𝐒𝐚𝐥𝐞𝐬 — Despite headline FX headwinds, wager-based same-store sales grew in Italy (+3.1%) and the Rest of World (+5.8%), demonstrating continued player demand and product strength.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐓𝐡𝐞 𝟐𝟎𝟐𝟔 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐂𝐫𝐚𝐭𝐞𝐫 — The final €1.43B ($1.67B) payment for the Italy Lotto license in April 2026 will wipe out FY26 operating cash flow (guided to negative ~$900M) and spike leverage up to ~3.5x.

• 𝐋𝐚𝐠𝐠𝐢𝐧𝐠 𝐈𝐧𝐭𝐞𝐫𝐧𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐆𝐞𝐨𝐠𝐫𝐚𝐩𝐡𝐢𝐞𝐬 — Reported revenue in the Rest of World segment reversed to an 11% decline ($70M), and the U. K. contract transition continues to act as a sustained structural headwind on the top line.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. The core lottery engine is incredibly resilient and margins are accelerating, but the peak CapEx cycle and the massive Italy Lotto license payment will consume all near-term cash generation.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢🟢 𝐎𝐏𝐭𝐢𝐌𝐚 𝐂𝐨𝐬𝐭 𝐒𝐚𝐯𝐢𝐧𝐠𝐬 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐏𝐫𝐨𝐟𝐢𝐭𝐚𝐛𝐢𝐥𝐢𝐭𝐲 [NEW]

The most important operational takeaway this quarter: Brightstar is getting leaner. The OPtiMa cost reduction program and disciplined G&A spending allowed a meager 1% increase in revenue to flow through to a 15% increase in Adjusted EBITDA. This operational leverage effectively insulates the bottom line against stagnant volume growth.

🟢 𝐔.𝐒. & 𝐂𝐚𝐧𝐚𝐝𝐚 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐋𝐞𝐚𝐝𝐬 𝐓𝐨𝐩-𝐋𝐢𝐧𝐞 𝐆𝐫𝐨𝐰𝐭𝐡

While overall revenue was sluggish, the U. S. and Canada segment provided the heavy lifting. Sales in the region accelerated, up 9% YoY to $281M, driven by favorable U. S. sales mix and reduced LMA shortfalls. It is the only geographic segment currently providing meaningful reported top-line expansion.

🔴 𝐇𝐞𝐚𝐝𝐥𝐢𝐧𝐞 𝐍𝐚𝐫𝐫𝐚𝐭𝐢𝐯𝐞 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐬 𝐑𝐞𝐩𝐨𝐫𝐭𝐞𝐝 𝐈𝐭𝐚𝐥𝐢𝐚𝐧 𝐑𝐞𝐚𝐥𝐢𝐭𝐲 [NEW]

The PR headline touts 'Revenue up on strong Italy performance.' This is highly misleading. Reported Italy revenue actually fell 4% YoY (from $246M to $236M). While wager-based same-store sales in Italy did grow 3.1% in constant currency, severe FX headwinds and higher service revenue amortization completely wiped out these operational gains on the P&L.

🔴 𝐓𝐡𝐞 𝐈𝐭𝐚𝐥𝐲 𝐋𝐨𝐭𝐭𝐨 𝐋𝐢𝐜𝐞𝐧𝐬𝐞 𝐋𝐞𝐯𝐞𝐫𝐚𝐠𝐞 𝐒𝐩𝐢𝐤𝐞

Brightstar's balance sheet is stable today (2.4x net debt leverage), but it is standing on the edge of a cliff. Management projects leverage will spike to ~3.5x pro forma following the €1.43B ($1.67B) final payment for the Italy Lotto license in April 2026. This limits capital flexibility heavily for the next 12 months.

🔴 𝐈𝐧𝐟𝐥𝐚𝐭𝐢𝐨𝐧𝐚𝐫𝐲 𝐏𝐫𝐞𝐬𝐬𝐮𝐫𝐞𝐬 𝐁𝐢𝐭𝐢𝐧𝐠 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧𝐬 [NEW]

Management explicitly flagged inflationary pressures impacting postage, freight, and other costs. While OPtiMa savings mitigated this at the EBITDA line, core service costs remain elevated. If inflation in physical ticket logistics persists, the company will have to lean even harder on digital volume to maintain margins.

🔴 𝐑𝐞𝐬𝐭 𝐨𝐟 𝐖𝐨𝐫𝐥𝐝 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠

The Rest of World segment was a distinct laggard, with revenue plunging 11% YoY to $70M (and down 18% in constant currency). The ongoing U. K. service contract transition continues to be a structural drag on international results, and management has not provided a clear timeline for when this headwind will fully roll off.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 (𝟐𝟔𝐐𝟏): $55 million

Decelerating sharply. FCF collapsed 49% YoY from $109M in 25Q1. This drop was driven by a heavy 45% increase in CapEx (up to $110M) as the company invests in contract renewals and systems, coupled with negative working capital timing.

𝐍𝐞𝐭 𝐃𝐞𝐛𝐭 (𝟐𝟔𝐐𝟏): $2.75 billion

Stable quarter-over-quarter, ticking up slightly from $2.72 billion in 25Q4. The company successfully refinanced its revolving credit facility out to March 2031 with improved terms, securing $1.6B in undrawn capacity to prepare for the massive upcoming Italy Lotto cash drain.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $2.50 - $2.55 billion

Stable. The reaffirmed guidance implies flat to ~2% YoY growth compared to FY25's $2.51B. Management noted this includes >5% organic growth, heavily offset by ~$175 million in incremental service revenue amortization related to the Italy Lotto license.

𝐅𝐘𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: $1.16 - $1.19 billion

Accelerating. Improving from $1.12B in FY25. Revenue growth and OPtiMa cost savings are expected to more than offset approximately $50 million of new investments in growth initiatives.

𝐅𝐘𝟐𝟔 𝐍𝐞𝐭 𝐂𝐚𝐬𝐡 𝐟𝐫𝐨𝐦 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐨𝐧𝐬: Negative ~$900 million

Reversing violently. The baseline business expects to generate ~$750M in operating cash, but the $1.67 billion (\u20ac1.43 billion) final payment for the Italy Lotto license completely overwhelms organic generation, causing a massive optical cash burn for the year.

𝐅𝐘𝟐𝟔 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐄𝐱𝐩𝐞𝐧𝐝𝐢𝐭𝐮𝐫𝐞𝐬: $450 - $475 million

Accelerating. A peak CapEx cycle continues, driven by contractual obligations tied to recent contract wins and system extensions. This elevated spend will further pressure standard Free Cash Flow metrics.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐏𝐨𝐬𝐭-𝐋𝐨𝐭𝐭𝐨 𝐃𝐞𝐥𝐞𝐯𝐞𝐫𝐚𝐠𝐢𝐧𝐠 𝐏𝐚𝐭𝐡

With leverage guided to spike to 3.5x after the April 2026 Italy Lotto payment, what is the specific timeframe and mathematical path to return leverage below your 3.0x long-term target?

𝐔𝐊 𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭 𝐓𝐫𝐚𝐧𝐬𝐢𝐭𝐢𝐨𝐧 𝐑𝐨𝐥𝐥-𝐨𝐟𝐟

The UK service contract transition remains a persistent drag on the Rest of World segment. In what specific quarter do you expect these difficult YoY comps to fully roll off?

𝐋𝐨𝐠𝐢𝐬𝐭𝐢𝐜𝐬 𝐚𝐧𝐝 𝐈𝐧𝐟𝐥𝐚𝐭𝐢𝐨𝐧 𝐌𝐢𝐭𝐢𝐠𝐚𝐭𝐢𝐨𝐧

You highlighted postage and freight inflation as an offset to EBITDA growth. Are you structurally redesigning your physical distribution networks, or simply relying on OPtiMa G&A cuts to subsidize these variable cost increases?](https://pbs.twimg.com/media/HIHSF14XkAAoOH-.jpg)