Most people are sharing this a16z stablecoin stack as a map of modern financial infrastructure.

It is one of the most complete views of how capital moves today:

• On/off-ramps

• Liquidity providers

• Orchestration layers

• Compliance systems

• Applications

It shows how we coordinate value at global scale.

But it assumes something critical:

That the underlying data is correct.

The carbon removal market has a scale problem, but not the one most people think.

Everyone's asking which pathway can absorb the most CO2. That's the wrong question.

The real question is: which pathways can prove they're actually doing what they claim?

Forestry projects dominate the market today, not because they remove the most carbon, but because they're the easiest to finance under current verification standards. Most rely on modeled baselines and infrequent audits. When a project gets challenged, the credits collapse.

Direct air capture gets funding because it's measurable at the point of capture. But scaling means building industrial infrastructure faster than we've ever built anything.

Enhanced weathering and ocean-based approaches have massive theoretical potential. They also have regulatory uncertainty, ecological unknowns, and zero continuous verification at deployment scale.

Here's the actual ceiling: it's not physics. It's trust architecture.

Without real-time, cryptographically signed data proving what's happening in the soil, the water, or the atmosphere, every pathway is just a model with a confidence interval.

The market keeps debating which solution scales best. The real constraint is which solutions can be verified at scale.

That's the infrastructure gap Mālama is built to close. #CarbonRemoval #ClimateInfrastructure #dMRV

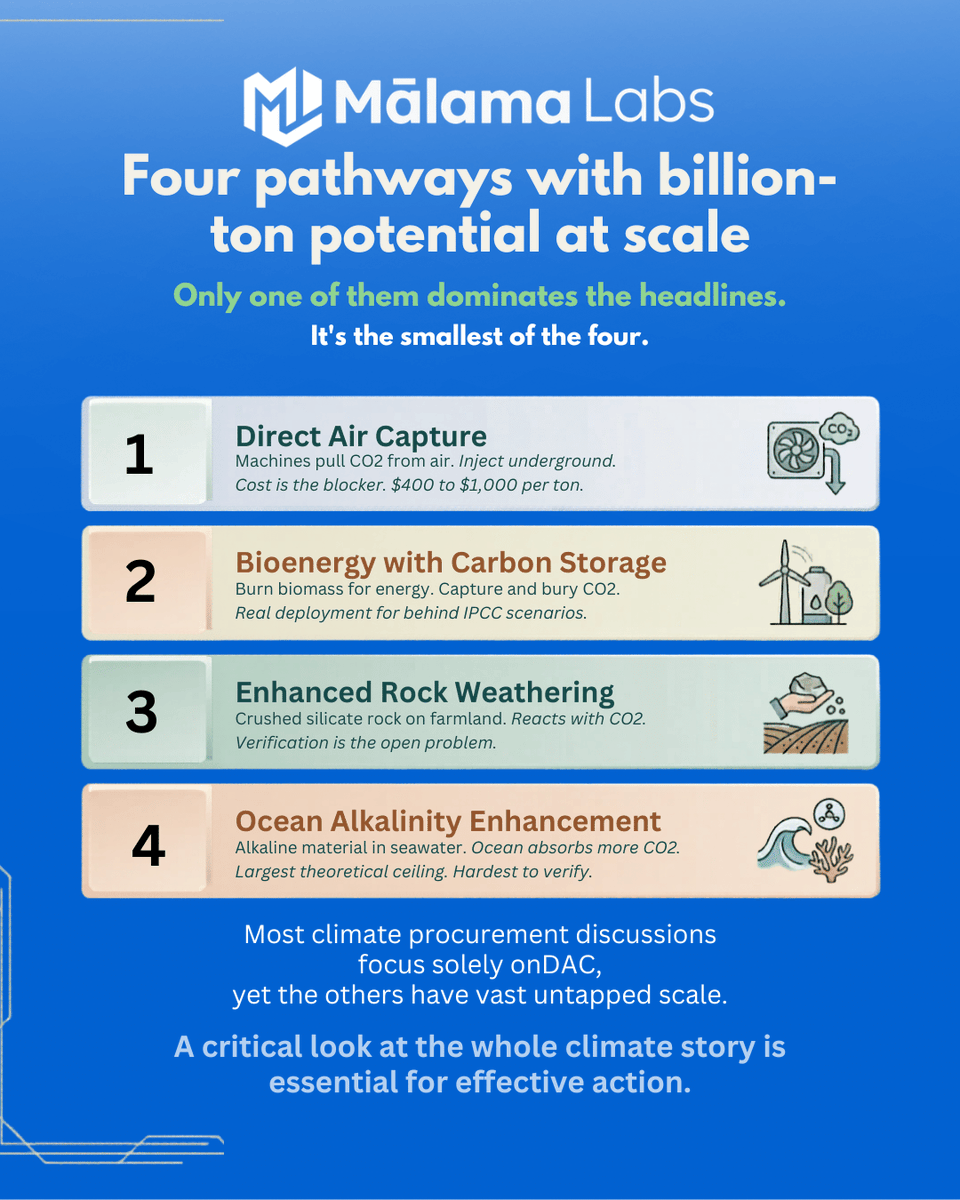

The carbon removal market is ignoring three pathways with billion-ton-per-year potential because they can't be verified yet.

Direct air capture gets all the oxygen in the room. Machines pull CO2 from the air, inject it underground. The science works. The verification works. Cost is $400 to $1,000 per ton. Procurement teams love it because it's auditable.

But DAC has the smallest theoretical ceiling of any major removal pathway.

Bioenergy with carbon storage. Grow biomass, burn it for energy, capture the CO2, sequester it underground. The IPCC's 1.5°C scenarios rely heavily on this. Real deployment is nowhere near model projections.

Enhanced rock weathering. Spread crushed silicate rock on agricultural land. CO2 reacts with the rock in soil moisture and mineralizes into stable carbonate. The geology is planetary in scale. Verification is the bottleneck.

Ocean alkalinity enhancement. Add alkaline material to seawater so the ocean pulls more CO2 from the atmosphere. Largest theoretical capacity of any pathway. Also the hardest to measure.

The market isn't ignoring these pathways because they don't work. It's ignoring them because carbon markets require proof, and proof requires measurement infrastructure that doesn't exist at scale yet.

That's not a science problem. It's a data infrastructure problem.

And data infrastructure problems are solvable.

For years, crypto has been criticized for building financial abstractions disconnected from real economic activity.

Then DePIN showed up.

Unlike most blockchain sectors, many DePIN projects are generating actual revenue from real-world services: connectivity, compute, mapping, storage, geospatial data, AI infrastructure, sensors, and energy.

A few examples (30d annualized revenue):

• Helium: $16.1M

• https://t.co/TkjDpDRZWk: $9.8M

• GEODNET: $8.0M

• Chutes: $5.6M

• Glow: $1.8M

• Akash: $1.4M

• Filecoin: $983K

• Render: $890K

• Hivemapper: $177K

The difference is simple:

Traditional crypto:

Token → speculation → hope utility arrives later

DePIN:

Hardware/service → customers → revenue → token incentives (sometimes)

The strongest DePIN networks increasingly look less like meme economies and more like infrastructure businesses with blockchain coordination layers.

This matters because markets eventually ask uncomfortable questions:

Who has users?

Who has paying customers?

Who has defensible infrastructure?

Who survives when speculation disappears?

The answer is not all DePIN projects. Revenue multiples are still wildly disconnected in places. Some networks trade at 500x+ revenue while others trade below 10x.

But something important is happening:

Crypto is slowly moving from “What token do you hold?” to “What economic activity does your network produce?”

That transition changes everything.

Source data: DePIN revenue leaderboards

Carbon removal procurement is splitting into two markets.

The first is what we have today. High volume, rising scrutiny, prices under pressure. Buyers offsetting emissions with credits whose integrity is increasingly questioned.

The second is forming under regulatory pressure. EU AI Act enforcement opens in August. CSRD reporting cycles are tightening. Corporate procurement teams are starting to ask a harder question: will these credits survive an external audit?

For most current credits, the honest answer is maybe.

The category that wins the compliance market isn't just about durability. It's about traceability. Carbon you can point to, with a measurement trail that goes back to the moment of capture, on infrastructure that auditors can independently verify.

This isn't a technology problem. Enhanced weathering works. Biochar works. Direct air capture works at commercial scale.

What's missing is the verification layer that makes carbon removal legible at audit time. The infrastructure that turns a field sensor or a DAC facility into an auditable data trail that can't be disputed three years later.

That layer gets built over the next ten years.

Most of the value won't accrue to whoever removes the most carbon. It will accrue to whoever proves it best.