Pleased to be in Bangkok for the IMFER Conference, co-hosted by @IMFNews and @BankofThailand. Looking forward to discussing how shifts in trade, investment, technology, and finance are reshaping the global economy and geoeconomic policymaking. https://t.co/F6NSbNDmmq

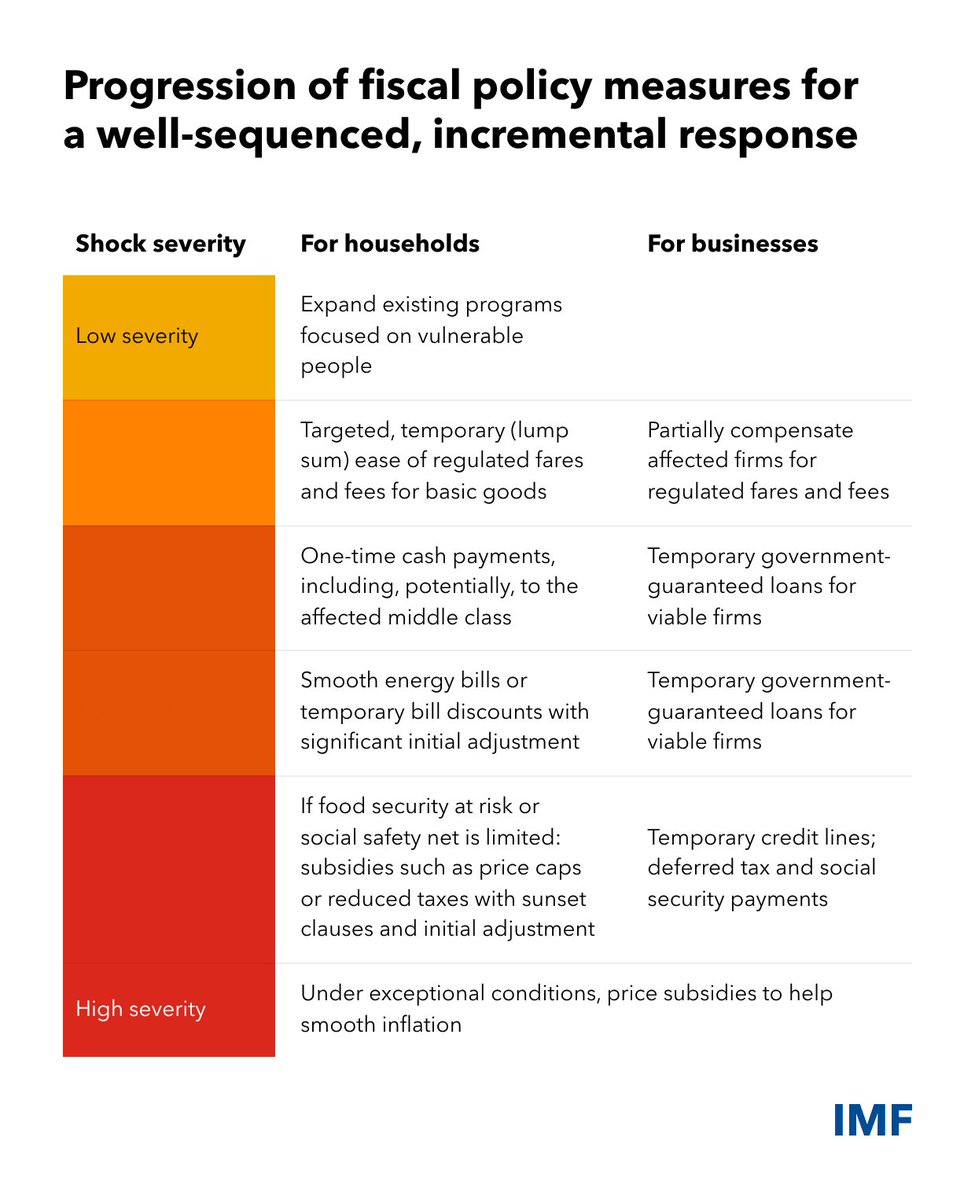

Governments can respond to energy and food price shocks in ways that help vulnerable people and keep businesses open without further straining public finances. See our blog.

https://t.co/iNWfO0ucXm

Throughout I have been so impressed with the quality of the people I worked with. Research assistants, junior and senior economists, support staff, colleagues, IMF management and country authorities. My heartfelt thanks to everyone. https://t.co/79o1EYpL9y

The time has come. Starting July 1, '26, I will be returning to @UCBerkeley. I am immensely grateful to @IMFNews for my time there as Chief Economist. In the last 4.5 years we have experienced a pandemic, inflation, war in Europe and the Middle East, tariffs, and energy crises.

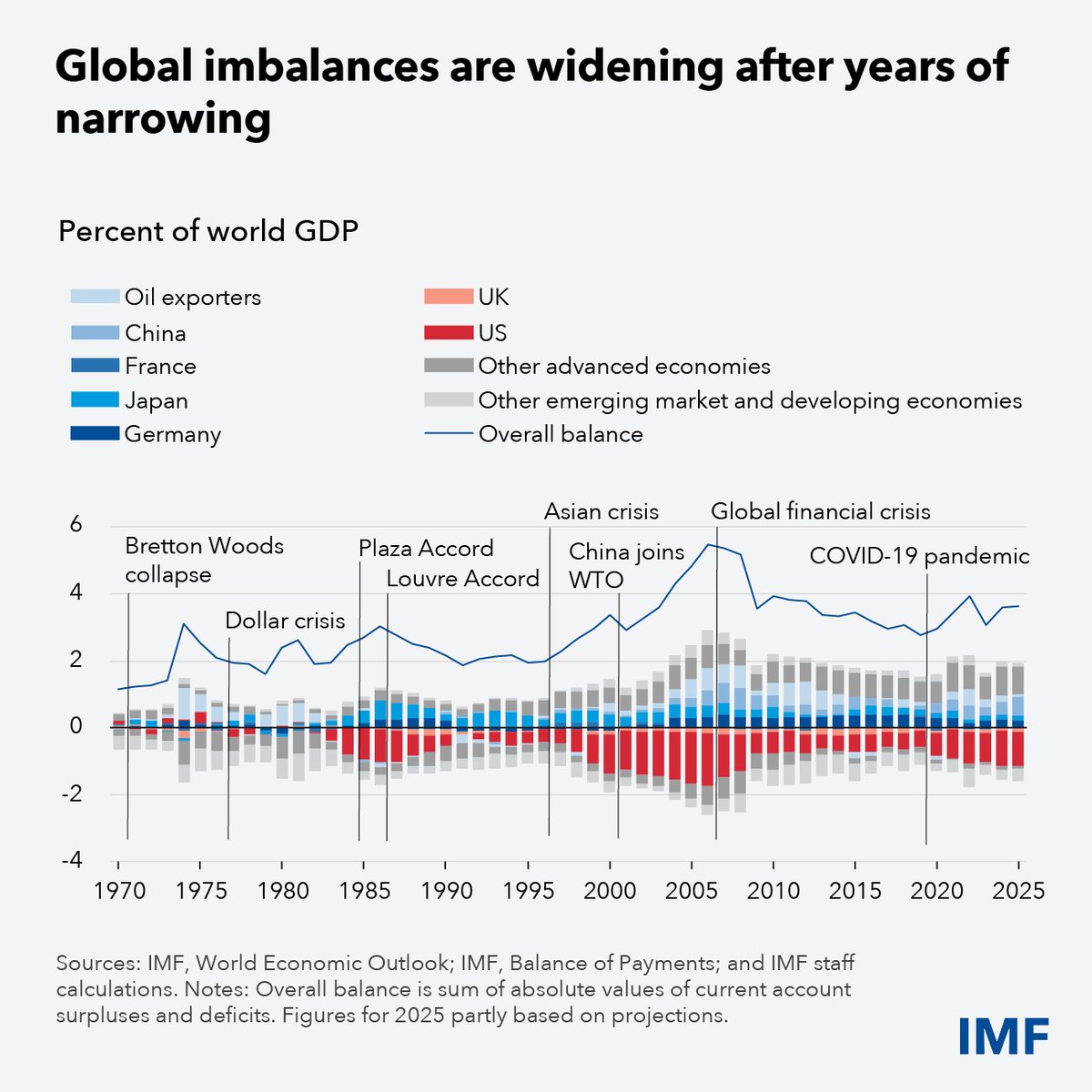

America’s big fiscal deficits are a political choice not an economic necessity. The causes of global imbalances are not, then, as clear as some commentators allege https://t.co/TJUn5fgev0

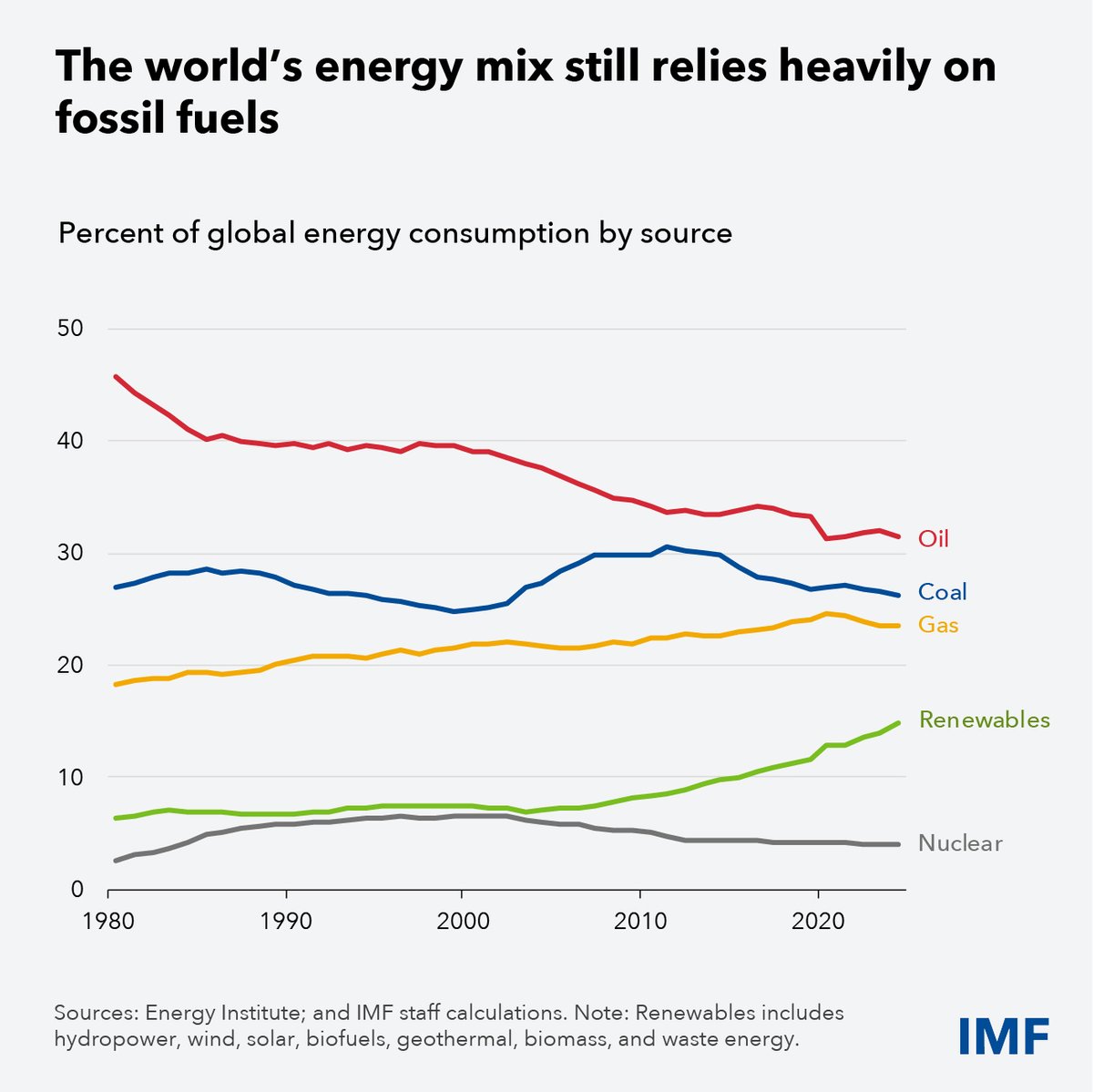

The world's energy mix still relies heavily on fossil fuels. But the war should spur faster adoption of renewable energy, strengthening resilience to energy shocks, improving energy security and supporting the climate transition.

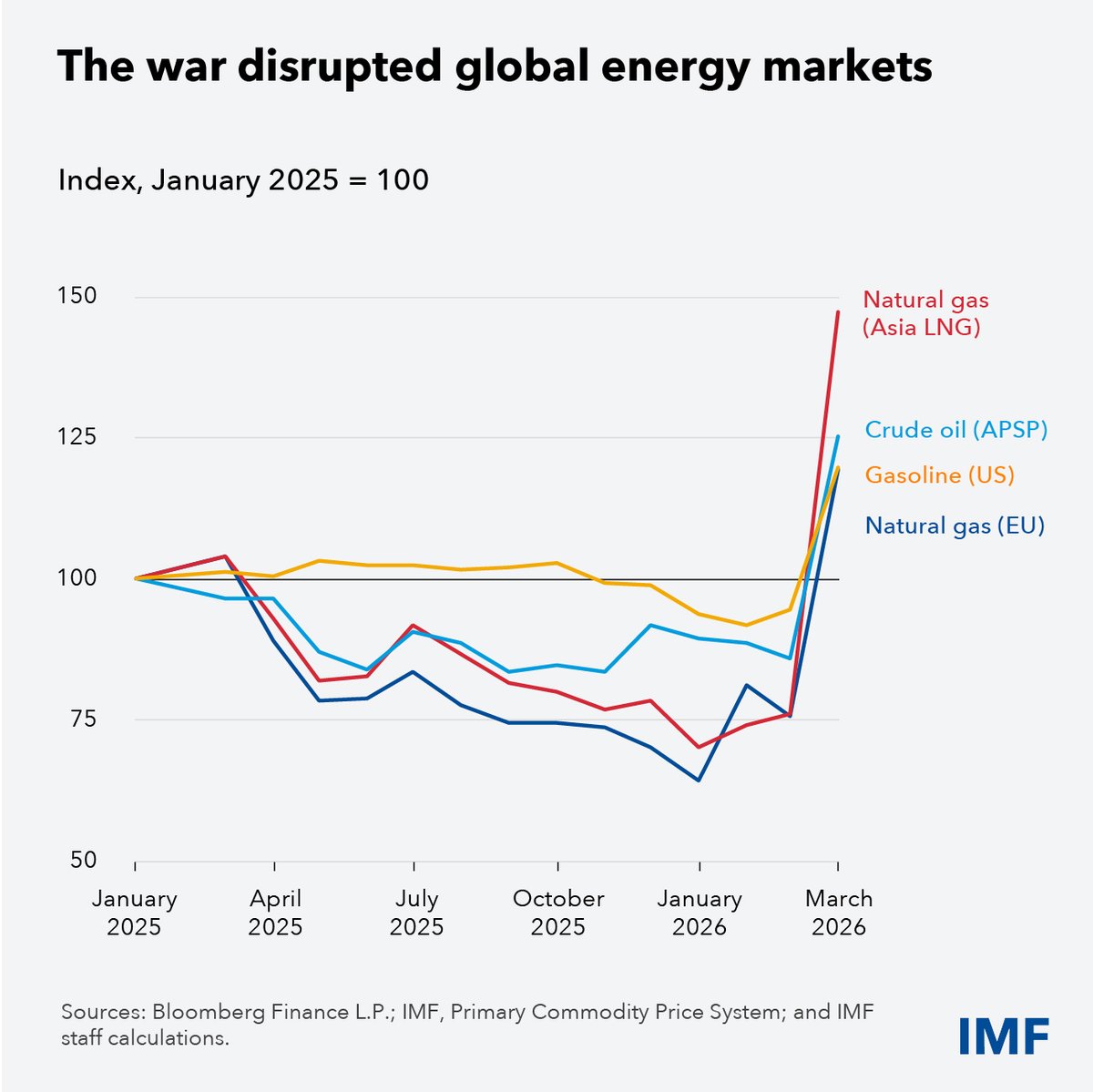

Our new WEO is out. War in the Middle East has halted the positive global momentum. The shock transmits through 3 channels: higher commodity prices; broadening inflation dynamics and rising inflation expectations; and a tightening of financial conditions that dampens demand.

Our policy message is clear: first, an early and orderly end to the war. Beyond that, central banks can afford to wait if risks to broader inflation remain contained and must be prepared to act as needed. Fiscal support needs to be targeted and temporary. https://t.co/eY0yMuk7WT

3/3 Post-conflict recoveries are slow, uneven & depend on peace. What helps a durable recovery? Early macroeconomic stabilization, debt restructuring, international support, domestic reforms to rebuild institutions, & state capacity. https://t.co/E09hL8uTPE

1/3 New analysis in our latest World Economic Outlook shows that conflicts generate large & persistent output losses in economies where the fighting occurs & nonnegligible spillovers to other countries.

2/3 In countries affected by conflict, output drops sharply, by about 3% at the onset & continues to decline, with cumulative losses of roughly 7% within five years. Output losses from conflicts typically exceed those associated with financial crises. https://t.co/eY0yMuk7WT

3/3 The takeaway: defense spending doesn’t “pay for itself.” The impact depends on how it’s financed, how long it lasts, and how much is directed at imports. Careful policy design is essential to manage trade‑offs and protect fiscal sustainability.

https://t.co/E09hL8uTPE

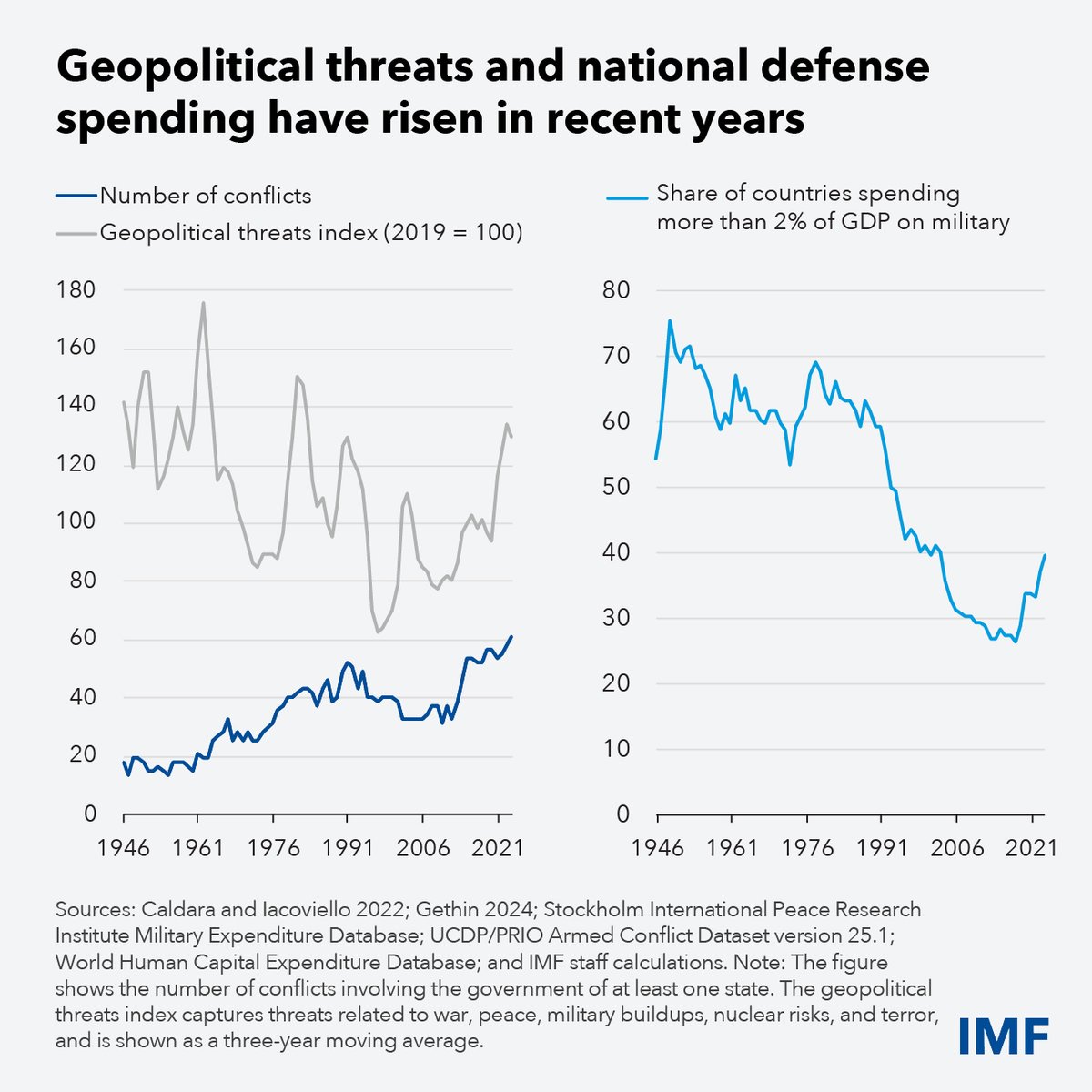

1/3 Defense spending is rising across the world as security concerns grow. Our analysis in the April 2026 World Economic Outlook shows these buildups are large—almost 3 percentage points of GDP—and mostly debt-financed.

2/3 Higher defense spending can boost economic activity in the short run. But it also tends to push up inflation, worsen budget balances, raise public debt, and weaken external positions. https://t.co/eY0yMuk7WT

Indeed, a very well-deserved John Bates Clark Medal. I am a huge fan of @ludwigstraub 's work which is highly relevant to what we do here at the @IMFNews. Congratulations Ludwig!

Global current account imbalances are widening again. History shows widening imbalances can cause sectoral dislocation, often come before financial crises or abrupt reversals of capital flows. A disorderly adjustment could be exceptionally costly. 1/7

There are no shortcuts. Durable rebalancing depends on sound domestic policies, not trade barriers. 6/7 See the full policy paper here:

https://t.co/a8kQb8Hc8k