$1.3 trillion wiped from the AI capital cycle on Friday.

The entire AI infrastructure complex sold as one correlated trade: semis, copper, uranium, lithium, rare earths, nuclear, robotics, space. When correlation goes to one, it tells you the market is repricing the cost of capital, not the demand for what that capital is building.

The SOX was technically stretched at 73% YTD. Broadcom and NFP were the triggers, not the cause. $755bn in hyperscaler capex is locked. Memory is constrained. Hormuz is still shut.

The physical layer has the last word. New Weekly Outlook live

https://t.co/aK7ENW7fNM

#AI #Semiconductors #MacroTrading

Friday's semi selloff isn't an AI story. It's a cost-of-capital story wearing AI clothes. Yields broke higher, multiples compressed, and a sector priced for perfection got repriced for merely reiterating guidance.

The physical layer didn't blink. The financial layer did. That's the divergence that matters.

https://t.co/YFBgdVwWvn

#AISupercycle #Semiconductors

SpaceX begins its IPO roadshow this week: approximately $75 billion at a $1.75 to $1.8 trillion valuation, with just 4.3 per cent of the company entering the public float.

This is not just a launch company going public. SpaceX is building the only vertically integrated stack that could plausibly support orbital compute at scale: the rockets, the broadband network, and the ambition to host AI workloads beyond the Earth's surface.

The full framework is in our latest In the Spotlight.

https://t.co/m2Xhm59BM8

#SpaceXIPO #OrbitalCompute #AIInfrastructure

Hyperscaler capex for 2026 has crossed $725 billion across the Big Four, up 77% year on year. The semiconductor-led rally has framed it as confirmation.

The harder question: whether the physical layer can absorb it. The financial layer moved. The physical layer did not.

New In the Spotlight from QF-MI:

— What the April/May rally settled, and what it left open

— The three binding constraints now pricing the cycle — Why the Rio Tinto/Amazon deal matters more than the capex headline

https://t.co/2XV3D3L1Fd

#AI #DataCentres #Capex #Uranium

Semis at all-time highs through an active war, headline inflation at a three-year high, and a fragile ceasefire that the White House has declined to confirm. The tape is ignoring all of it.

New Market Pulse out on the AI scarcity trade, the wedge in today's PCE, the curve doing the reading on Hormuz, and why the BofA Fund Manager Survey just captured the most crowded trade reading on record. The semis are defying gravity because the gravity has changed.

https://t.co/1UVarY0Wke

The two-layer split widened again this week.

The physical-constraint layer keeps tightening: DRAM prices up 60% in Q2, Micron committing $100bn to US capacity that won't deliver until 2030, copper concentrate showing the textbook signs of supply scarcity, uranium in correction-beyond-the-mean inside a structural bull.

The financial-asset layer is pricing a Hormuz deal that doesn't yet exist, with strikes resuming the morning after the headline framework was announced. PCE on Thursday will tell us which layer the market is listening to.

The QF-MI Weekly Outlook provides a full analysis and base case.

https://t.co/kvsZfsL5Lz

#AISupercycle #AIInfrastructure

The AI trade is splitting into two different markets.

One is the physical buildout: HBM memory, copper, power, transformers, nuclear infrastructure.

The other is the pricing mechanism: flows, positioning, momentum, narrative, liquidity.

This week, they diverged sharply. Nvidia’s fundamentals accelerated. The stock sold off. Memory names rallied.

Today's Market Pulse explains why the gap between what is being built and what is being priced may now be the most important signal in the AI supercycle.

https://t.co/Mm7OElQBIO

#AISupercycle #AIInfrastructure #HBM

The oil market is telling two stories at once.

The spot narrative says shortage in weeks. Record draws at 8.7 mb/d in May, inventories at 101 days of forward cover, an eight-year low. Tank-bottom scenarios for the US around early July.

The Brent curve says something materially different. Front month at $107, December at $89, June 2027 at $81, late 2027 in the high $70s. Steep prompt decay, then a long-end clearing price that has reset roughly $15 above pre-war levels.

The prompt premium decays. The post-war world reprices structurally higher. Both halves matter, and most commentary catches only one.

https://t.co/dLe7ZcL69c

#AISupercycle #BrentCrude #AICapex

NVDA earnings tonight are not really about the headline beat. The Street is quietly modelling a supply ceiling into the back half of the year, while positioning data is pricing the opposite. That divergence is the real signal.

This is no longer a pure semiconductor story. It is now a physical constraint story: HBM. Packaging. Power. Allocation. The financial layer and the physical layer are starting to diverge again.

That matters far beyond Nvidia.

Today’s Market Pulse provides deeper analysis.

https://t.co/xWr2zPKVse

#AISupercycle #Semiconductors #NVDA

The AI memory bottleneck is increasingly an allocation problem, not a spot-pricing problem.

Most meaningful HBM capacity is already committed across hyperscalers and accelerator platforms while advanced packaging, CoWoS, and wafer supply remain constrained.

That is why the recent semiconductor pullback matters less than many assume. The equities repriced. The physical shortage hasn't.

Meaningful incremental supply relief still appears limited before 2027.

#AISupercycle #Semiconductors #HBM

The AI supercycle’s two layers are diverging again.

The financial asset layer is repricing ahead of Nvidia earnings. The physical constraint layer is not.

HBM remains allocation-bound, packaging constrained, and meaningful incremental supply remains limited before 2027.

The drawdown repriced equities. It hasn't repriced the shortage.

https://t.co/NK5NfdiZQX

#AISupercycle #Nvidia #Semiconductors

The largest US electricity deal since AI reshaped capital allocation landed this morning: NextEra is acquiring Dominion for roughly 67 billion dollars.

Most coverage will frame it as a dealmaking story. The more revealing reading: utilities this size only consolidate when the asset they sell, electricity, has become genuinely scarce.

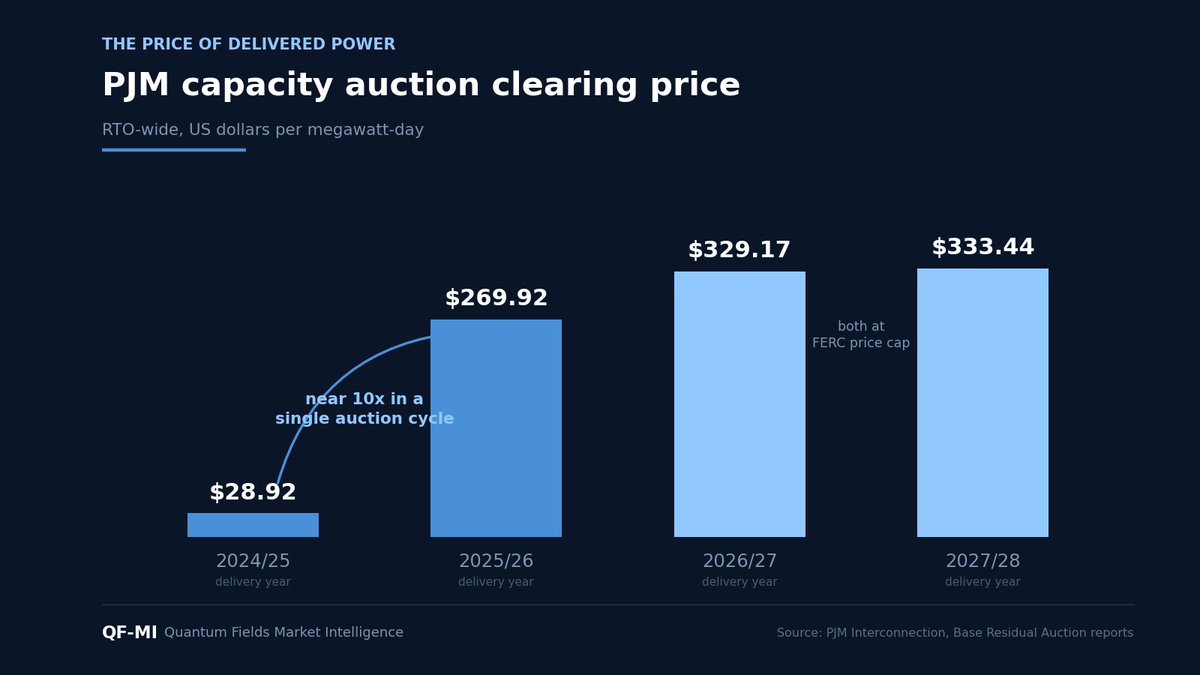

Power is now one of the binding physical constraints on AI growth. PJM's latest capacity auction failed to secure enough generation to meet its reserve margin, a first in its history. Gas turbine slots are sold out into 2030. A hyperscaler with unlimited capital still cannot conjure a transformer on demand.

When power becomes this scarce, the firms that supply it consolidate. That is what this deal reveals. Full analysis in the next In the Spotlight.

#AIInfrastructure #PowerGrid #DataCenters #Utilities

The AI supercycle gets tested on two fronts this week.

Tuesday: a reported US security meeting on Iran, Hormuz still shut.

Wednesday: NVIDIA's print into a five per cent long bond.

The physical layer is tight. The financial layer is stretched. Two binaries decide which way the gap breaks.

The Weekly Outlook goes deeper

https://t.co/HATEITXGZi

#AI #Semiconductors #Nvidia

Oil markets are pricing something equity markets haven't processed yet.

Hormuz is effectively closed. US crude inventories drew at nearly double consensus. The Brent-WTI spread remains historically elevated. And the shale elasticity that cushioned every previous tightening cycle is structurally weaker.

The physical energy system beneath the AI infrastructure stack is tightening before the AI demand wave has even arrived.

That timing mismatch is the story. Today's Market Pulse provides more analysis.

https://t.co/2bXvNZBkEN

#AIInfrastructure #EnergyConstraint #AISupercycle

The Cerebras IPO was 20x oversubscribed and priced above range, at a fully diluted valuation near $56bn.

Markets are no longer just funding AI infrastructure incumbents. They are now funding optionality around what comes after them.

That is a different phase of the cycle.

https://t.co/NpfJeBdVi2

$CBRS #AI

The market is looking through the war.

Brent near $104. Trump rejects Iran’s peace response before Beijing. Yet semis hit new ATHs.

Hyperscaler capex is at $725B. Memory is sold out through 2026.

The AI supercycle is now a balance sheet reality. https://t.co/rtSd5lcJBF

Payrolls beat consensus by 50K. Equities bid the headline. Bonds bid the wage cooling underneath it. The dollar moved on Iran, not on NFP.

Inside the AI complex: semis led, hyperscalers faded. The bifurcation hardened intraday. Full Market Pulse

https://t.co/ed3HDs6SkI

Anthropic took the full power of SpaceX's Colossus 1 in Memphis. 220,000 Nvidia processors, 300 MW within a month, plus joint interest in gigawatts of orbital AI compute. The orbital layer crossed from speculation into commercial planning.

https://t.co/17mIsRfrXC

The AI trade is splitting. Samsung surges on HBM.

AMD jumps on AI compute demand.

Infineon raises power guidance.

Anthropic reportedly commits $200B to compute capacity.

Infrastructure is repricing higher.

Software multiples are compressing.

https://t.co/VVlpdtosRt