JUST IN: 🇮🇷🇺🇸 Iranian state media confirms deal with the US and says it includes lifting sanctions, withdrawing US military from around Iran, and ending the naval blockade.

Biggest IPO in history to trade today @CNBC 🇺🇸 states US$350 billion chased the US$75 billion IPO prices at $135 with greenshoe to US$86 billion likely

25 leveraged ETF funds linked to @SpaceX said waiting to buy to meet their mandate as tracker funds

Let’s see how this listing goes given all the hype & puffery

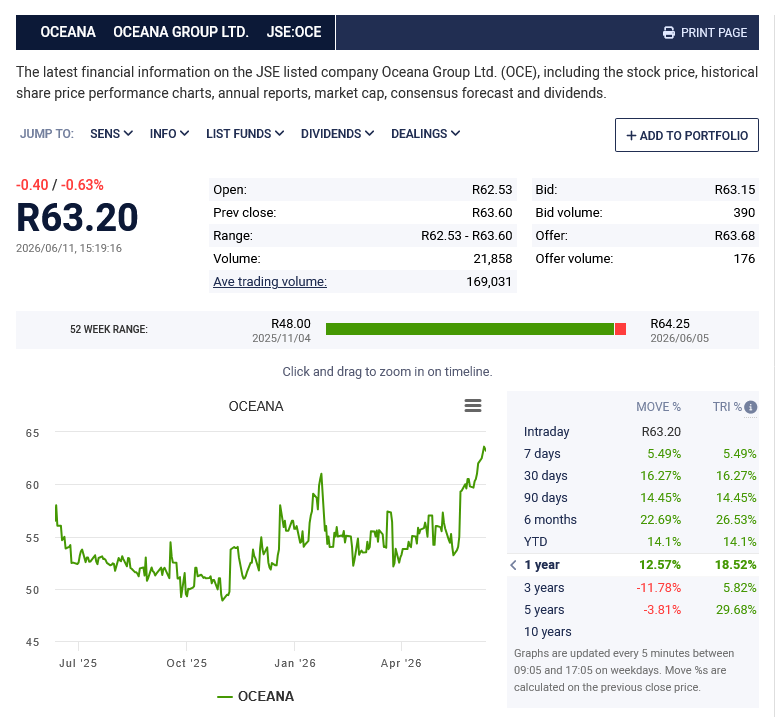

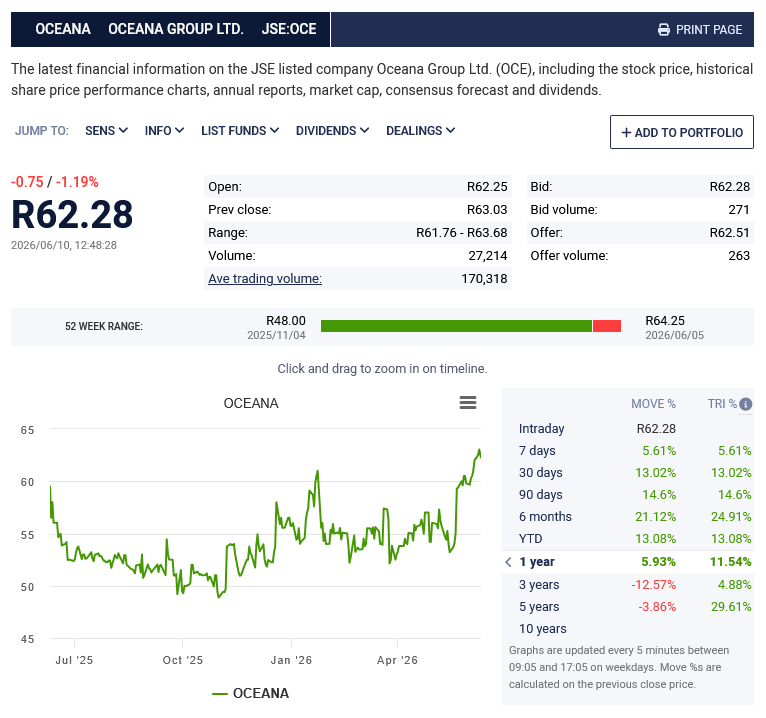

$JSEOCE Oceana CEO and CFO step into the market and buy shares as #OCE trades near 52-week highs

CEO Neville Brink buys 20,000 shares for R1,253m

CFO Zaf Mahomed buys 6,006 for R375,272

Maybe they see what I see - better prospects from large US subsidiary Daybrook adding lustre to #OCE results

Breaking news: The European Central Bank has become the first central bank in the G7 to increase borrowing costs in response to the Middle East energy shock https://t.co/hM6Fu0T0K3

Breaking news

More positive news for Oceana’s Daybrook

Peru has extended its anchovy fishing ban with no date set for its removal, adding further uncertainty to global fishmeal and fish oil supplies. The ban on fishing has been in place since late-April

The suspension, which had been due to expire on June 10th, remains in place across much of Peru’s northern and central coastline

Authorities said the restrictions could be lifted fully or gradually following further scientific assessments by Government Fishing Bodies

The ban remains in force amid ongoing Coastal El Niño conditions and concerns over a high proportion of juvenile fish in the stock

Peru is the world’s largest producer of fishmeal and fish oil, making developments in its anchovy fishery closely watched by aquaculture feed markets

Only 24% of the first season’s TAC of 1.9 million tons was landed before the ban started. The first season fishing traditionally ends in mid-to-late June and the on-going ban on fishing raises concerns that the first season will be cancelled echoing the 2023 El Nino issue that slammed Peruvian fish meal and fish oil production and caused prices to spike

Just in May, when Peru initially had a mini ban, then a mega ban (that was extended to June 10th) fish oil prices have run from $3,500 to $7,000 a ton (+100%) and fish meal from $2,340 to $2,940 a ton (+25.6%). I am awaiting my data points for June to update

On this ban extension it is likely prices, where stocks are said to be globally tight, will run further ahead.

Just off the $JSEMTH Motus pre-close call for year end results to June 2026. The tonality reflected the challenges in some market segments (UK, Australia, used cars) but also indicated that #MTH was holding its own and even gaining in some areas

#MTH started the year well with the stock running hard to a peak of R132.50 then from March slumped -24% to the current price of R100.76 as the rampant charge of the Chinese and Indian vehicles rampaged through the sales landscape

#MTH indicated it had fared reasonably well in the past six months and highlighted that it expected profits growth in high teens and a -20% reduction in finance costs (past results have been driven by reduction in debt and the associated finance income saving)

On a current PE of 6.5x with a better reporting period ahead I'd wager that #MTH has probably reached its bottom with support around R100.00

Any movement from here will be sentiment directed on expectations on new vehicle sales given the recent rise in interest rates and the soaring price of fuel. This may temper investor interest in #MTH until guidance on results are seen in September

Here is a link to this morning's presentation

https://t.co/xBzmRahc6r

@Meatman_WP@Agrimark_ZA The Stanford cheap diesel branch is owned by Overberg Agri the unlisted co-op based in Caledon controlled by investment fund Acorn Agri (not) KAL Group

They also have even cheaper diesel at their branch in Caledon

All eyes on this today and what will be the next move in the world's largest fish meal and fish oil producer

Peru's Ministry of Production (PRODUCE) is in the middle of a 30-day extended industrial anchovy fishing suspension in the north-central zone. Running from May 27 through June 10, 2026, the ban was enacted due to persistent El Niño conditions and a high concentration of juvenile fish

Prices have risen strongly since May as the fishing ban started and there was a tightening of supply of the key aqua ingredients globally

Will the extended ban be pushed out from June 10th?

Granular but highly important early data as the harvest for 2026 comes off the fields

The Crop Estimates Committee has estimated a record commercial maize harvest for the year at 17,064 million tons

Yellow maize 7,885m tons

White maize 9,179m tons

Soya 2,911m tons

Year to date prices remain benign

Yellow maize -5.57% to R3,238 a ton

White maize -9.26% to R3,302 a ton

Soya +2.2% to R6,800 a ton

Though the harvest remains in play looking at the @sagis_info weekly yield data its very encouraging

White maize grade 1 (WG1) is at 94.6% but on 5% of harvest collected

Yellow grade 1 (YM1) is at 95.7% on 10% of harvest collected

The % of WG1 is highly encouraging given the crop in 2025 was at 64-65% thus South Africa will have ample supplies of quality maize for domestic use and export

Klerksdorp agricultural giant @SENWES issues a trading update for its year ended April 2026 which indicated earnings would be 20% higher than the prior period

NHEPS in FY2025 were 399.1 (-18%) as the impact of drought and weak sales of agricultural equipment weighed

Given the timing of planting and the harvest, Senwes's earnings lag what occurs in the sector, thus the record 2026 commercial maize and soya harvest will only start to benefit the company into its new financial year (May to October 2026) as record volumes of product pass through their system

FY2026 saw an improvement in mechanisation (Germany has heavily loss-making in 2025) and the Senwes retail cluster in the year performed better

Senwes trades on the company's own platform with the stock steady for an extended period at R19.40 a share (there is an on-going share buyback upto R20.00)

On a PE of 4x with NAV nearer R30.00, @SENWES is an appealing play in the sector though highly illiquid for those who prefer a steady play in the sector

Results are due July 3rd

Getting back to my old self after an extended period of sickness and fever from this nasty cold/flu going around

Live on @cnbc today at 4.45pm playing catch up on the small-to-mid cap sector and top stocks of 2026

H1 2026 results from asset manager $JSESygnia were pleasing depending on your base comparative

No H1 presentation just financials.

Total AUM +13.6% R460.8bn but unchanged from YE2025 results to September. Main kick was AUM inflows +R43.1bn in the six months

Umbrella funds +27.1% R23 billion but +12.2% from YE2025 results to September

Expenses +21.6%

PBT +25.4% R302.1m

HEPS +22.0% 138.1cps

Dividend 24.5% 122cps

Retail AUM R91.6m but only +1.3% from YE2025 results to September

Main growth areas (Revenue)

Investment management +10.9% (50.4% of revenue)

Admin fees +66.5% (27.1% of revenue)

Treasury services +43.2% (16.6% of revenue)

#SYG closed at R32.50 year-to-date -8.6% but from its late-March sell-off its ++18.1% with the stock the best performing listed asset manager over the past 12-months

Owned the stock since IPO and very happy with results performance + on-going juicy dividends

May sales data for capital equipment out from The South African Agricultural Equipment Association (SAAMA)

May tractor sales 542 units down -14.6% like on like and down a modest -1.0% month-on-month

27 combine harvesters sold -34.7%

Sales are usually soft this time of the year as farmers are busy taking the harvest off the fields

Although market sentiment remains positive, an increasing number of uncertainties are overhanging the market. Amongst others these are current summer crop yields, input costs, commodity prices, interest rates and weather prospects for the forthcoming summer cropping season

With lower year-in-year prices for key fields crops yellow & white maize and soya alongside rising production costs into the new planting season (it starts in October) equipment sales may be subdued

In chatting to $JSEOMN Omnia this morning on YE2026 results they indicated they have sufficient supplies of key nutrients and they anticipate farmers will continue to plant with some change on the margins (less maize, more sunflower and modest change in soya)

Clubbing is dead and has been replaced by fitness & wellness.

Ppl used to party to socialize and date but now they do things like HYROX, bathhouses, and running raves.

The death of clubbing is something to be studied:

— US has lost 12% of its nightclubs in the last 24 months

— 25% of US adults didn’t drink at all last year

— Gen Z drinks 30% less than Millennials did at the same age

On the flip side:

— According to Strava, the number of running clubs recorded on the platform increased 3.5x in 2025

— 72% of Gen Z go to run clubs to meet new people

— Sauna and spa market: $11.8B → $22.4B by 2034

The post-alcohol economy is gonna be a massive category.

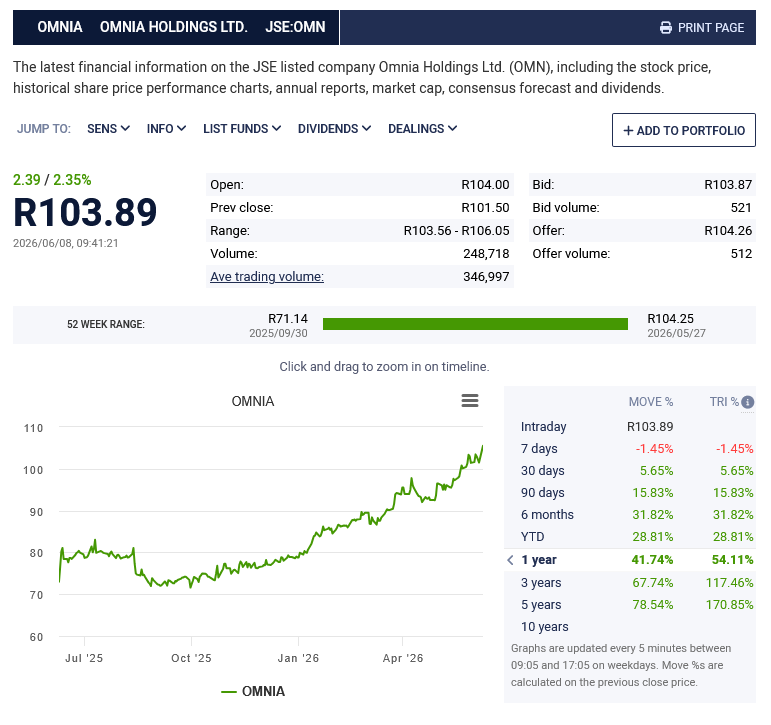

Solid results from fertilizer and explosive business $JSEOMN Omnia as the stock - on results & the dividend news - hits a new 52 week high of R103.89 a gain year-to-date of +28.8%

As a March year-end, Omnia has not yet materially benefited from the Middle East conflict push in various fertilizer compounds price increases - which only started kicking in in March onwards

Given the strong cash generation, #OMN again declares fat dividends with a 470 cent ordinary dividend and a 280 cent special

HEPS for the year saw growth of +21% to 849 cents per share supported by the recovery of agriculture

Rest of Africa and the substantial completion of the chemicals restructure

Africa agriculture delivered profit of R260m from a prior loss of R62m

Chemicals moved to a profit of R4m from a prior loss of R133m

These were the main kicks to results

Overall. Agriculture profits +27.5% to R1,251m and explosives +1.4% to R1,145m

There is an 11H00 webinar on results which I am participating in to get the management unpack on results & prospects

#OMN a favoured recommendation from this desk for the past couple of years

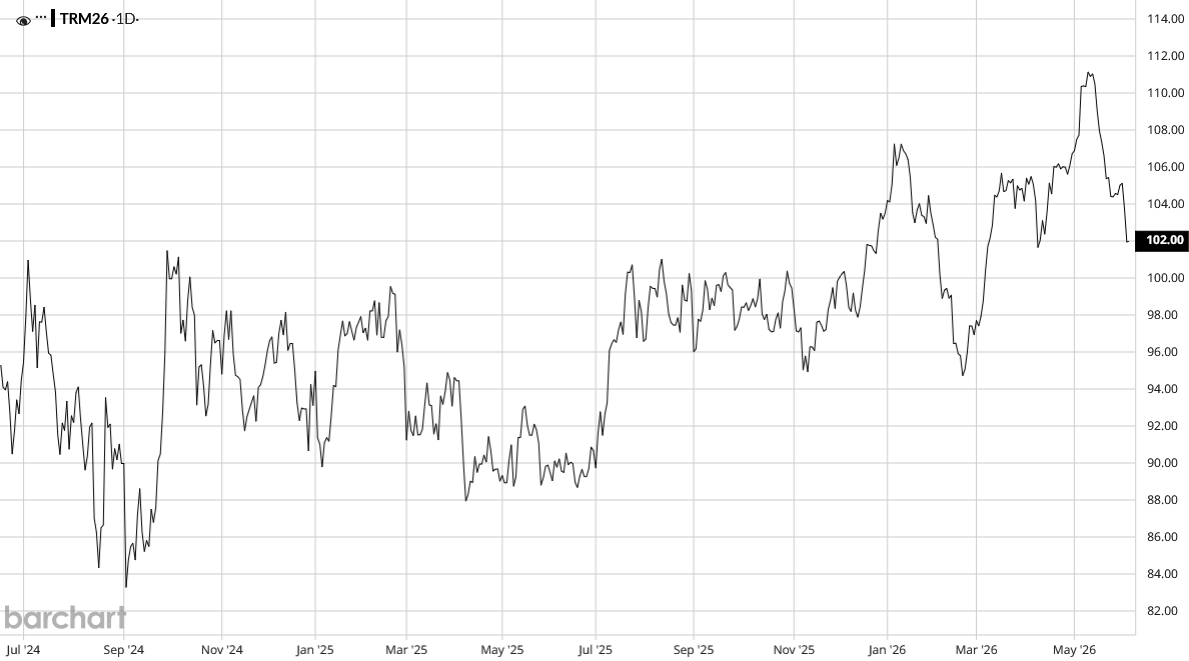

Monday data points

Iron ore trending lower on the week to US$102 a ton = R1,691 (current spot 16.58)

The world is awash with iron ore with increased production from Australia and Brazil with a significant ramp up in the giant Simandou’s mine's output

Chinese steel demand remains muted due to seasonal slowdowns and weaker profitability and the coking coal fatality. The Shanxi accident pushed domestic coking coal futures sharply higher, hitting the daily trading limit

Cocoa has also collapsed from its peaks but do you see the price of chocolate 🍫 bars falling on the shelves or reversal of shrinkflation gram sizes?

Nope, more special offers, more promotional activity but consumer goods rarely ever cut prices …. so they will be creaming profits from coffee for quite some time yet

Slightly biased as I contribute articles to the @FinancialMail but this week’s issue is a damn good read well worth my R46.50

Raymond Steyn’s article on mining scallywag Brett Kemble & @MarcHasenfuss piece on $JSEHCI are both great reads