@bradloncar I love my new term - " unburdened by what has been" statistical method - we don't really care what the real # is like because the patient was discontinued for treatment- but - hey, we can project the # and never mind the discontinuation/tolerability/dropout issues... Ha!

Not much to do in this mkt - I got the stuff I like at the amazing prices - might just as well to take a step back and get some rest - .. the last wk or so been mostly metabolic side pulling the lever - now the more beaten down orphans and neuros come to join the party - slowly chipping away the bad YTD - April is clearly in the green now.. Ha!

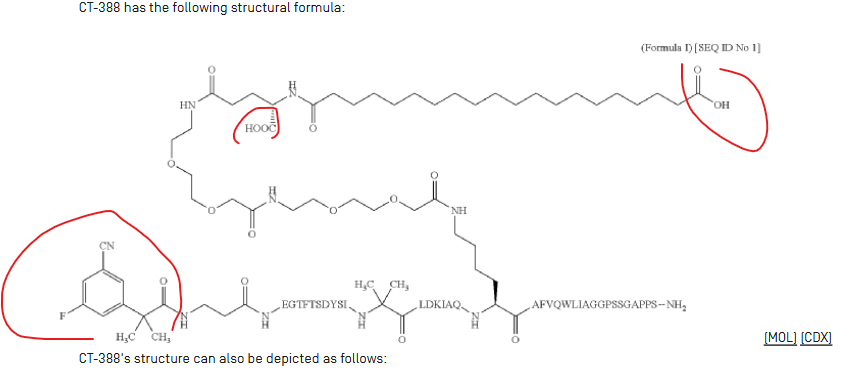

The $RHHBY CT388 modification is over the C-terminus with a "Tyrosine-like" residue - the fatty acid sidechain is still within the peptide sequence .. I have CT388 and a structure from the $VKTX patent here for comps - .. Pretty interesting with these variations of the peptide - .

$NVO Oral Sema. pills - up to 50 mg QD - Novo says it’s submitted obesity pill for FDA approval - probably using data from OASIS trials - Generally 11-15% WL at 68 wks - but focus on tolerability - 25 mg QD in OASIS 4 (lower dose vs OASIS 1) had 47% nausea and 31% vomiting - on annual consumption basis - each oral patient will consume 70X (25mg Oral QD vs 2.4 mg SC QW) - they need something to cut down that consumption rate - Ha! jmho https://t.co/qXPihyeV3n via @BioPharmaDive

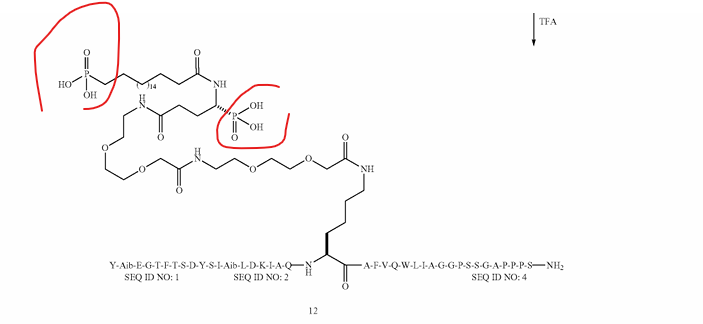

@KNielsen2000 @fluffer9 yeah - when I did the search, I looked at it more than a few times and checked if I missed something - but clearly the patent is about the phosphonated structures w/ the polypeptides - .. one of those for sure is -2735. Ha!

They certainly listed the generic structure of the polypeptide in the patent - so, not a classic "small molecule" per se - .. more importantly, the patent is over the generic structure of their modification - the usage indication is not over the claims section - .. consider this as a composition of matter type of patent - .. they definitely will have human data to do more patent filings based on the whatever they have in the clin trials using the molecules listed in this patent.

Biotech probably been shorted to the other side of the blackhole by these funds - .. interesting that it is actually doing better even w/ the interest rate headwinds - ..

Any small chges in the modifications could have an impact - .. that's why I care about these patent applications when I see one - trying to get a picture on what makes the new molecules different - .. for example - the Metsera patent has the lipidation done at the N-terminus - they add a Lysine there - then some molecules with even more amino acid residues added - then lipidate there - and the T 1/2 they have w/ these molecules were staggering - .. but like you say - chging these could impact potency - affinity bindings etc - .. all a fine balance to work thru.. jmho.

$VKTX They definitely mentioned in the patent on the opposite vs expectation based on BSA binding - .. one could only speculate the reasons - cpd 4 and 12 structures were listed - and it is pretty simple phosphonate cpds w/o further modifications - .. maybe have to do with the peptidase activity side w/ the degradation of the parent cpd? Either way - it's an interesting patent - I'd bet they will cover the modifications of the phosphonate - too obvious someone will just take this work and modify from there. jmho

@GilaMonstrum@fluffer9 Probably via higher affinity w/ albumin - .. and we don't know the precise structure of -2735.. further modification of the phosphonate grp[s] - say forming a cyclic ring, altering the hydrophobicity - will all have an impact - ..

@houndcl@LY4101174@TheBiotechBear Pretty kool - I didn't gig up the mfging patent for orfor - just by looking at it with the chiral centers - and the multiple segments - is a fun molecule for MedChem Grad school final exam Q - and with no cheating on AI search etc.. Ha!

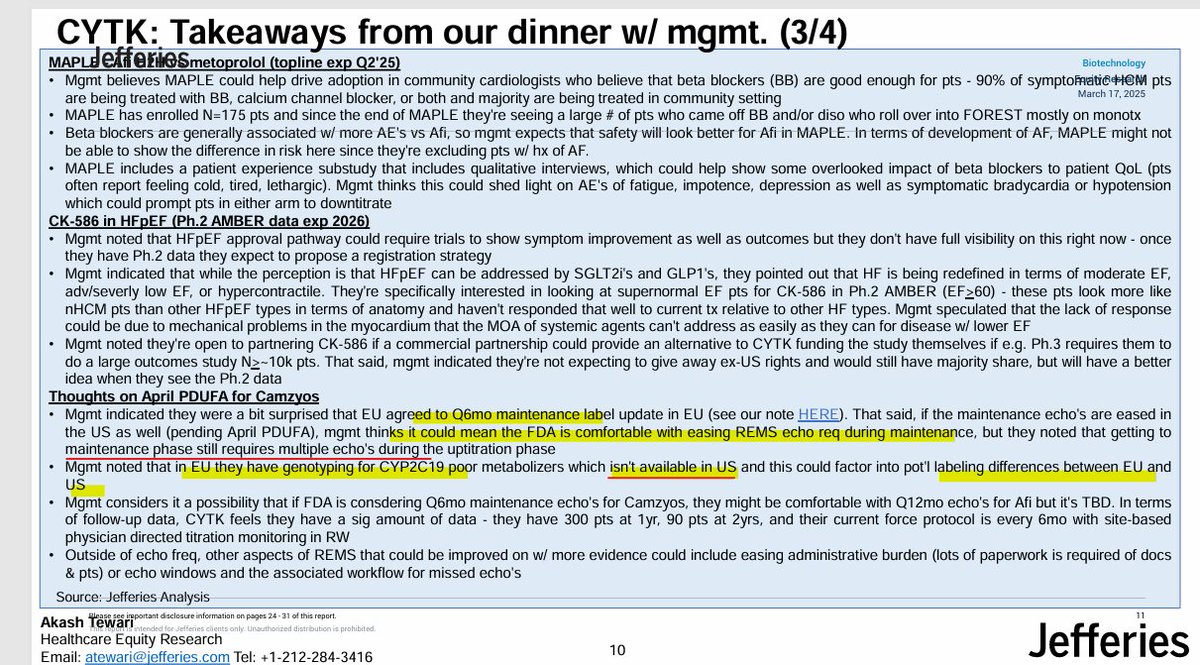

Think the $BMY Camzyos REMS/label update is pretty much in line with this $CYTK mgmt disczn w/ Jefferies in March - ..MAPLE P3 readout next - maybe 2HMay?? jmho.

Borrowing money and to hope for these zombies will return the cash at 90% of value - ok - .. let's see how this plays out - ..seen thru so many of these cycles - in mid 2002 - it was not uncommon to see badcos trading at 30 cents of the dollar - and those were the days where financing for the sector was super tough in the wake of the tech bust, widespread accounting scandals across sectors, and the perceived risk of the FDA uncertainty (IMCL RTF was the rude awakening for many).. so, cash zombies were there, and cash zombies will be here as well - how many will actually liquidate and return 90% of the cash asset to shareholders - I have my doubts.

$MTSR is heavily shorted - and in the Post Danu world - this is one of the obvious portfolio companies can jump start an obesity pipeline - much like Carmot did to Roche - .. and this is not a Chinese clone - and they have a big library of peptides (20,000) - and that could be the source for other future candidates - .. and the key differentiation is the ultra-long T 1/2 w/ the peptides - enabling QM dosing - also the potency of the lead cpds seems very robust - the misconception and the bear thesis on this been the high vomiting rate (60%) w/ the 1.2 mg dose (the highest) they tested in the 12 wk study - but that dosing cohort has no titration at all - the WL #s were robust - almost Trizp. like except this is a mono-GLP1 (like sema) - then the oral peptide platform - I need not repeat the same theme again - oral peptides - clean w/ tox - difficulty in the consumption side - and they acquired the D&D oral peptide platform to optimize the dose consumption - many readouts coming for the rest of the yr - .. EV at 1.3-1.4B - arguably a much better pipeline than Carmot was in Dec 2023 when it was taken for 2.7B (and 400MM future milestone payments) - it is a new IPO in this bad tape - people think it is another me-too GLP1 - but at least to me - it ranks the highest on the differentiation scale - based on 1) deep science bench 2) library of follow-on cpds w/ different MoAs - Amylin/ PYY/ GIP/ GUCR 3) longest T1/2 among the incretin peptides in commercial/development --> QM dosing 4) Oral peptide delivery platform 5) Not a Chinese clone in this tape -.. I had some posn soon after the IPO - then got more during the horrible "Tariff liberation" days at mid-teens - and took the size even higher after the Danu news at mid-upper teens - balancing out the proportions I like to have in the metabolic side of the portfolio - .. The March 4th TD Cowen presentation (at their website) is well worth listening to for those interested - I don't care what the shorts do - but in the post Danu world - they better be right or one day w/ a lightning strike - well.. that's why I don't do shorts.. jmho.

A lot is riding on the $VKTX Venture-Oral readout - 13 wk endpt with WL - .. I particularly care the high dose cohorts - and I want to see $NVO oral Amycretin like WL #s 10-12% pbo adj. (then I will comp the tolerability profile) = around the same time, we should get the $LLY orforglipron 72 wk Obesity P3 - consensus is a 15% WL - With the very high oppty cost associated w/ the $PFE Loti-Danu busts - anyone (and there are more than a few using Danu chemistry) in the oral GLP1 space gotta worry these late safety events in very large N trials - there is no room for safety mishaps - under this scenario - oral peptides would make the most sense on risk/reward basis - AS LONG AS the oral delivery side get the kinks out to get the economics to work. jmho.

I am not the worm inside $MRK - all my contacts are ex-Merckies now - .. but am I factually incorrect that the current form of Vk-2735 oral is economically not feasible w/o some sort of oral delivery platform like what MRK just did w/ Cyprumed (what they are aiming for there - again, I am not the worm inside MRK's tummy -maybe their oral pCSK9 or maybe something more) .. also - am I factually incorrect that Orforglipron is a very challenging molecule to make vs the likes of Danu/Loti-Glipron?