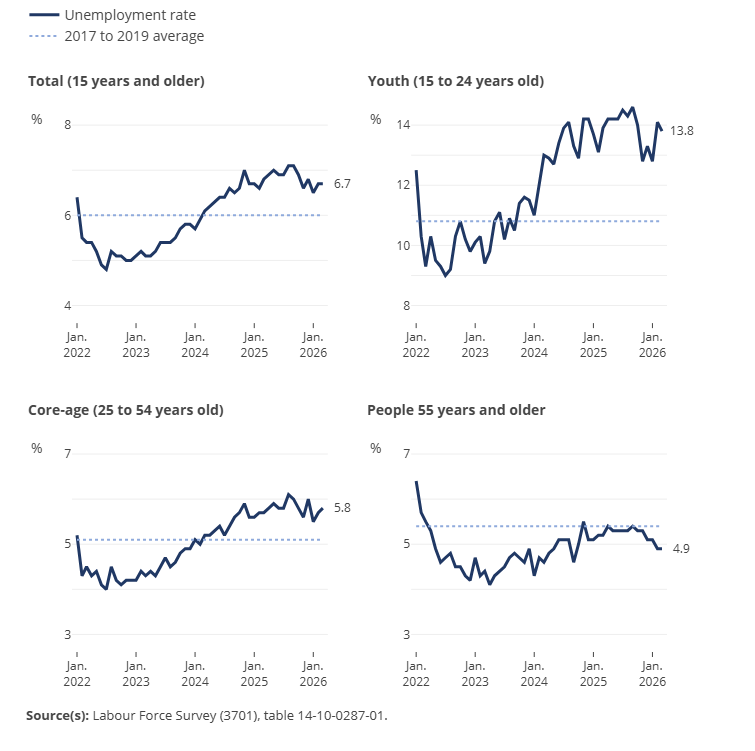

BREAKING NEWS: StatsCan reports Canada employment surges by 88,000 in May, a big rebound from a tough start to the year. The gains were driven by a monster 154k increase in full-time employment. The unemployment rate falls to 6.6% from 6.9%.

https://t.co/YNO6w5scHu

Given there is a lot of debate out there on whether Canada is in a recession or not. I thought I'd weigh in with a couple of thoughts, and a bit of history.

Two straight quarterly contractions is usually a good INDICATOR of a true recession, but not always. Canada’s economy wasn’t in a recession in 1970, even though output contracted in the first two quarters of that year. Nor did we have a recession in 2015, even though Canada experienced back-to-back quarters of falling GDP that year.

There have also been times, such as 1974 and 1960, when the country fell into recession without two quarterly declines in output.

Plus, the declines in GDP this year are so small that revisions could easily cast the story in an upward direction.

It’s just too early to conclude a recession occurred over the past six months, and the final tally may not be known for another year or two. I'm sure the C.D. Howe Business Cycle Council, the authority of these things in Canada, will weigh in at one point.

My opinion. Given that household spending has been rising, even with a massive slowdown in population growth, the economy does not look recessionary to me. I don't think there's been any instance of a recession with rising household spending.

BREAKING NEWS: Canada's economy is still struggling to find growth. StatsCan data out today shows zero growth in first quarter (more precisely, the numbers show a minuscule contraction). The weak reading in first quarter of 2026 comes after a small contraction in fourth quarter of 2025.

Consumption remains solid, but business investment continues to shrink. Non-residential business investment has fallen for three of the last four quarters and is now at the lowest in two years.

Some will be quick to characterize this as a "technical recession". But we need to be careful here since data will get revised. Best way to describe this is an economy that has been essentially stagnant over past six months, in large part because of weak business investment.

After slowing down sharply in 2025, we see a rebound of Canadian foreign direct investment into the U.S. in the first quarter of this year, according to the latest data released today by Statistics Canada.

Link to the numbers is here: https://t.co/pFxNN4FpVL

Canadian FDI into the U.S. jumped to $24 billion in Q1, which is about the total for all of 2025 and the most in any one quarter since Q1 2024. Last year's investment numbers into the U.S. were the lowest in more than a decade.

While some will worry this is a comeback of the "capital exodus" story we hear so much about, I'm actually relieved to see Canadian businesses investing, any where. This is a sign of health, with the added benefit that it shows confidence in the outlook for the Canada-U.S. economic relationship.

GDP numbers out tomorrow will show us whether Canadian businesses are ramping up investments at home as well.

U.S. FDI into Canada was $16 billion in Q1, which is slightly down from Q4 2025, but remains well above historical averages.

So FDI flows back and forth between our two countries is healthy. This is a good thing.

For what it's worth, the NY Times (with Basu and LeBrun writing) has much much much better coverage of the Canadiens' run than any Canadian paper not based in Quebec. Just an observation.

BREAKING NEWS: Canada unexpectedly lost 18k jobs in April, with the jobless rate rising to 6.9% from 6.7%. The details are even worse. Canada lost 47k full-time jobs in April, which was only partly offset by rising part-time. Canada has seen employment drop 112k so far in 2026.

Canadian inflation is on the rise again thanks to the war in Iran. Gasoline prices jumped by 21% on the month, according to Statistics Canada, the largest one-month increase on record. Underlying inflation (what are known as core measures) was little changed, which suggests spillover effects remain contained for now.

https://t.co/RmadmOmslC

Faced with the option of an approximately $30 billion pipeline, tied to a $20 billion carbon capture project, with entrenched political opposition, and a ban on oil tankers, rational economic actors did what anyone could have predicted they would do, which was to find cheaper and easier sources of egress.

There’s no doubt in my mind that Canada’s strategic interests would be best served by a new NW BC pipeline.

Inexplicably, we made it the most expensive, contentious, and risky.

The result? We’re getting a private proponent-led pipeline but it’s sending more barrels to the USA.

https://t.co/xajGUx4IjH

BREAKING NEWS: Canada added a net 14.1k jobs in March, in line with expectations. The unemployment rate was unchanged at 6.7%. It's the first employment gain in three months and partly offsets a decline of 109k jobs in the first two months of the year. Still, it's a small gain and all the gains last month were part-time. Full-time employment was little changed. Labour demand remains anemic.

https://t.co/NnufQFyD1E

Canada's financial sector has a long history of doing business in China. And Finance Minister Francois-Philippe Champagne's trip to the Asian country, along with Bank of Canada Governor Tiff Macklem and financial sector executives, is not the first such delegation.

In the summer of 2009, Finance Minister Jim Flaherty took Mark Carney, then Bank of Canada Governor, and a swath of bank and insurance executives to China to tout the stability of Canada's financial system and do some business. That too was a time of relationship rebuilding between Canada and China.

Flaherty was one of five ministers who traveled to China that year. Others included Trade Minister Stockwell Day, Foreign Affairs Minister Lawrence Cannon and Transport Minister John Baird. They paved the way for a trip to China for Prime Minister Stephen Harper.

The only difference this time is that the prime minister went first.

There's been much discussion about whether Canada could actually benefit from the recent war-induced spike in oil prices. It's a compelling idea, but Canadians should be wary of it.

In fact, I would argue it's unambiguously negative overall, and the costs to us will rise the longer the shock persists.

Higher oil prices will boost export income, profits, and government revenues, particularly in energy‑producing regions. But they will squeeze consumers and non‑energy businesses. They will reduce real disposable income and raise costs economy‑wide. And there are serious distributional and regional impacts, which will create social cohesion and other political challenges.

It will tilt increasingly negative over time as higher energy prices act as a net drag on global growth, even as it drives global inflation and interest rates higher.

Which is why the Bank of Canada has been cautious about highlighting the positive aspects of the crisis.

To be sure, we'll probably be relatively less worse off than the rest of the world. But still worse off.

Of course, one potential longer-term benefit is for the crisis to strengthen the investment case for Canadian energy. But the key factors holding back investment haven't suddenly disappeared: long project timelines, massive lump-sum nature of investment and construction; regulatory and policy uncertainty; as well as uncertainty about long‑term global demand given the potential for a major global downturn.

https://t.co/xLsEjhsReh

My latest piece for @TheHubCanada. A taking stock on the state of Canada's economy. I write how:

1) The recent data flow has tilted negative. And now with war in the Middle East, the near-term outlook has clearly worsened further

2) We’re facing multiple headwinds at once: probably weaker-than-expected growth to start in 2026; risk of renewed inflation pressures; elevated geopolitical and economic uncertainty

3) But it’s easy to overstate the weakness. The picture is more nuanced than the headlines suggest

4) This is an economy being pulled in different directions. A true “crosswinds” moment. On the downside: trade tensions with the U.S. are weighing on exports and hitting business confidence and investment. On the upside: past interest rate cuts are starting to support households; financial markets (until recently) have boosted wealth and spending; higher commodity prices are lifting incomes and profits; government spending continues to underpin demand

5) The base case hasn’t collapsed. Most economists still expect growth to return to about 2% in the second half of the year, assuming uncertainty eases

6) But risks are rising again. The Middle East conflict is a reminder of how fragile that outlook is

7) The deeper issue remains unchanged: Weak business investment is undermining the fundamentals.

The bottom line:

Canada’s economy is holding up, but is fragile. We’re stuck in a low-velocity economy. Not in recession. Not in a real growth cycle. Just waiting for some certainty.

https://t.co/C18Tvz9Cqa

News on the Canadian economic front this morning is on the sobering side for the near-term outlook.

The Bank of Canada held its policy rate at 2.25% today, as expected, but struck a notably cautious tone. It flagged downside risks for growth but also upside risks for inflation tied to higher energy prices amid war in the Middle East. In other words, an uncomfortable setup: slowing growth alongside renewed inflation pressures.

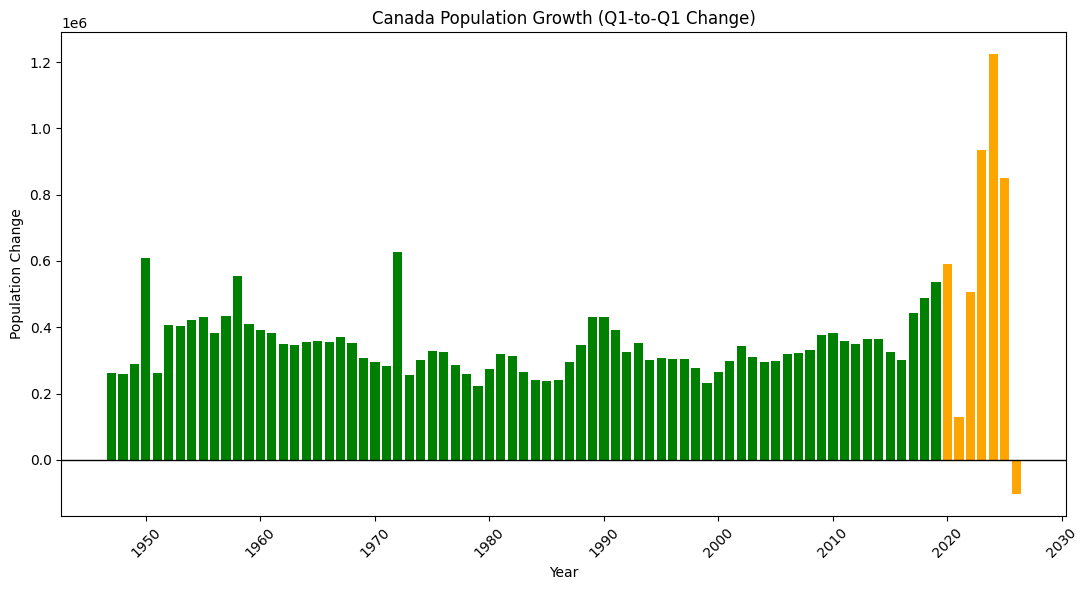

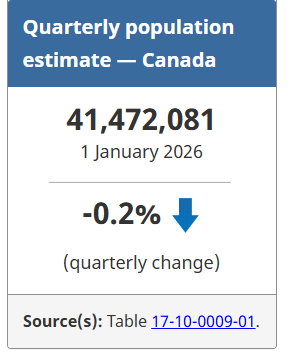

Separately, new data from Statistics Canada points to a meaningful shift in another key driver of growth: population.

Canada’s population declined in 2025 for the first time on record, falling by just over 100,000.

The government’s effort to scale back immigration is clearly having an effect. That should help ease pressure on housing and tighten labour markets, the intended objective.

But it also removes an important source of economic momentum.

Put it together, and the picture is one of an economy facing multiple headwinds: weaker growth in the near term, renewed inflation risks, heightened uncertainty, and a structural slowdown in population growth.

The margin for error for policymakers is narrowing.

It's official. Canada's population fell for the first time on record in a calendar year. Statistics Canada estimates population declined by just over 100k in 2025, to just under 41.47 million on Jan. 1. Canada took in 394k permanent residents last year, the lowest number since 2020. The population of non-permanent residents dropped by 462k last year.

https://t.co/VkHYVoUawc

BREAKING NEWS: Bank of Canada leaves its overnight policy rate unchanged at 2.25%. Central bank warns of short-term inflation and growth risks from Middle East conflict. It also acknowledges the higher inflation/lower growth dynamic puts it in a bit of a bind. Key excerpt from the rate statement:

"Relative to our January forecast, risks to economic growth are tilted to the downside. Near-term growth looks weaker than expected and the review of the Canada-United States-Mexico Agreement is a big unknown. At the same time, risks to inflation are tilted to the upside, because of the sharp increase in energy prices. Economic weakness combined with rising inflation is a dilemma for central banks. Raising interest rates to slow inflation could further weaken the economy. Easing interest rates to support growth risks pushing inflation well above target."

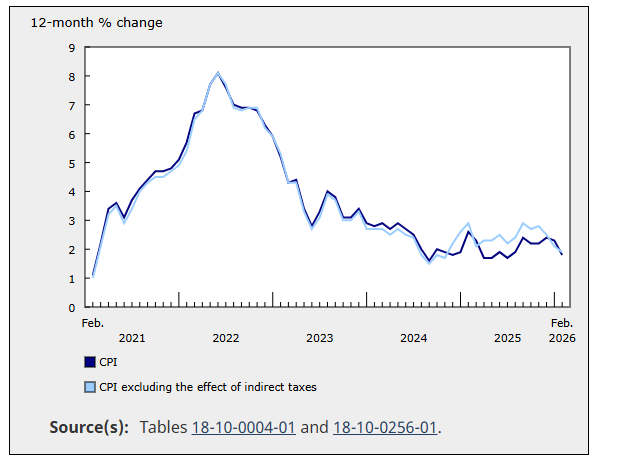

For those keeping a closer eye on food prices. Food inflation was 5.4% in February. That's down from 7.3% in January. Since Feb. 2021, food prices have increased about 29% versus 19% for the overall consumer price index.

BREAKING NEWS: Canadian inflation continued to ease in February, with consumer prices up 1.8% from year ago. That's down from an annual rate of 2.3% in January. Core price metrics - a better gauge of inflation pressures - also eased and are hovering at just over 2%. All-in-all a benign inflation picture before war erupted in the Middle East.

https://t.co/TfebfxI5X1