📈 Portfolio Update – February 17, 2026 📈

Real money swing trading results since inception (April 5, 2021):

TomALPHA: +338.12%

SPY: +67.77%

-Asymmetric risk/reward focus: fintech, payments, and undervalued growth.

- Real brokerage screenshots on every fill. Patient through drawdowns.

- Portfolio currently hedged with 3 written SPY PUT options for downside protection. No hype, no noise.

🔥 Top 7 positions by weight:

• $PYPL – 12% (target $80 → +99%)

• $S – 10% (target $28 → +102%)

• $EEFT – 8% (target $165 → +143%)

• $ZAL – 8% (target €34 → +57%)

• HKG:0175 (Geely Auto) – 8% (target HK$24 → +41%)

• $BABA – 7% (target $215 → +36%)

• $DIDIY – 7% (target $7 → +52%)

Highest conviction upside plays right now: $EEFT (+143%), $S (+102%), $PYPL (+99%), and several others with 60-140% potential.

Continuing to average down selectively on multi-year lows where fundamentals remain strong and valuations are historically attractive.

Which of these looks most compelling to you? Best risk/reward? 👇

Not financial advice. Past performance no guarantee of future results. Investing involves substantial risk of loss.

Full portfolio breakdown, deeper models & real-time updates → https://t.co/a3gH4E1BKp

#Fintech #SwingTrading #ValueInvesting #Payments

🚨 $WIX just crushed Q4 profitability while building the AI platform of the future

Revenue in line, EPS massive beat, Base44 already scaling to $100M ARR run-rate. Mid-teens guidance for 2026.

TomALPHA quick breakdown of the print 🧵

1/ 📊 The Beat

• Revenue: $524.3M (+14% YoY) → in line with ~$527M consensus

• Bookings: $534.5M (+15% YoY)

• Total ARR: $1.836B (+14% YoY)

• Non-GAAP EPS: $1.81 vs $1.47 est → **+23% BEAT**

• Non-GAAP Op Income: $81.2M (15.5% margin) → beat by 6%

• Partners Revenue: $203.2M (+21% YoY, 39% of total revenue)

• FCF: $155.6M (30% margin)

GAAP net loss -$0.73/share due to one-time Base44 earnout (excluded from non-GAAP).

2/ 📈 Key Trends

• Creative Subscriptions revenue +12%, Business Solutions +18%

• Base44 (acquired <9 months ago): already $59M ARR, on track to ~$100M

• New users +5.6M in 2025 (total >304M)

• ACPS up 14%, 10-year cohort value >$20B (+14% YoY)

• Core Wix gross margins stable >70%, Business Solutions +200bps YoY

AI products (Wix Harmony + Base44 vibe-coding) outperforming expectations.

3/ 🎯 2026 Outlook = Clean

• Revenue & Bookings: mid-teens % growth (both FY and Q1)

• $2B share repurchase program announced (aggressive execution)

• FCF margin: low-to-mid 20s% (investments in hyper-growth Base44)

Wall Street was sleeping on the AI pivot. This print shows it’s working.

Short-term margin pressure = long-term rocket fuel.

Bullish or still waiting?

Reply **BULL** or **BEAR** + one reason why. Best takes get reposted 🔥

#WIX #Earnings #AI #Fintech #Stocks

Europe gas prices +50%. Qatari LNG halt just vaporized the "energy stability" thesis for 2026. ⚡️

The market is pricing in a bidding war for US cargoes. Expect massive margin compression across EU industrials as input costs decouple from last week's projections.

Alpha Plays:

- Long $SHEL / $TTE (Capturing the LNG arbitrage)

- Short $DAX / $EWG (Manufacturing overhead is now unsustainable)

- Long $BOIL / $UNG (US export demand proxy)

Inflation isn't dead; it just found a new catalyst.

Positioning for a structural shift or calling this a 48-hour fluke? 👇

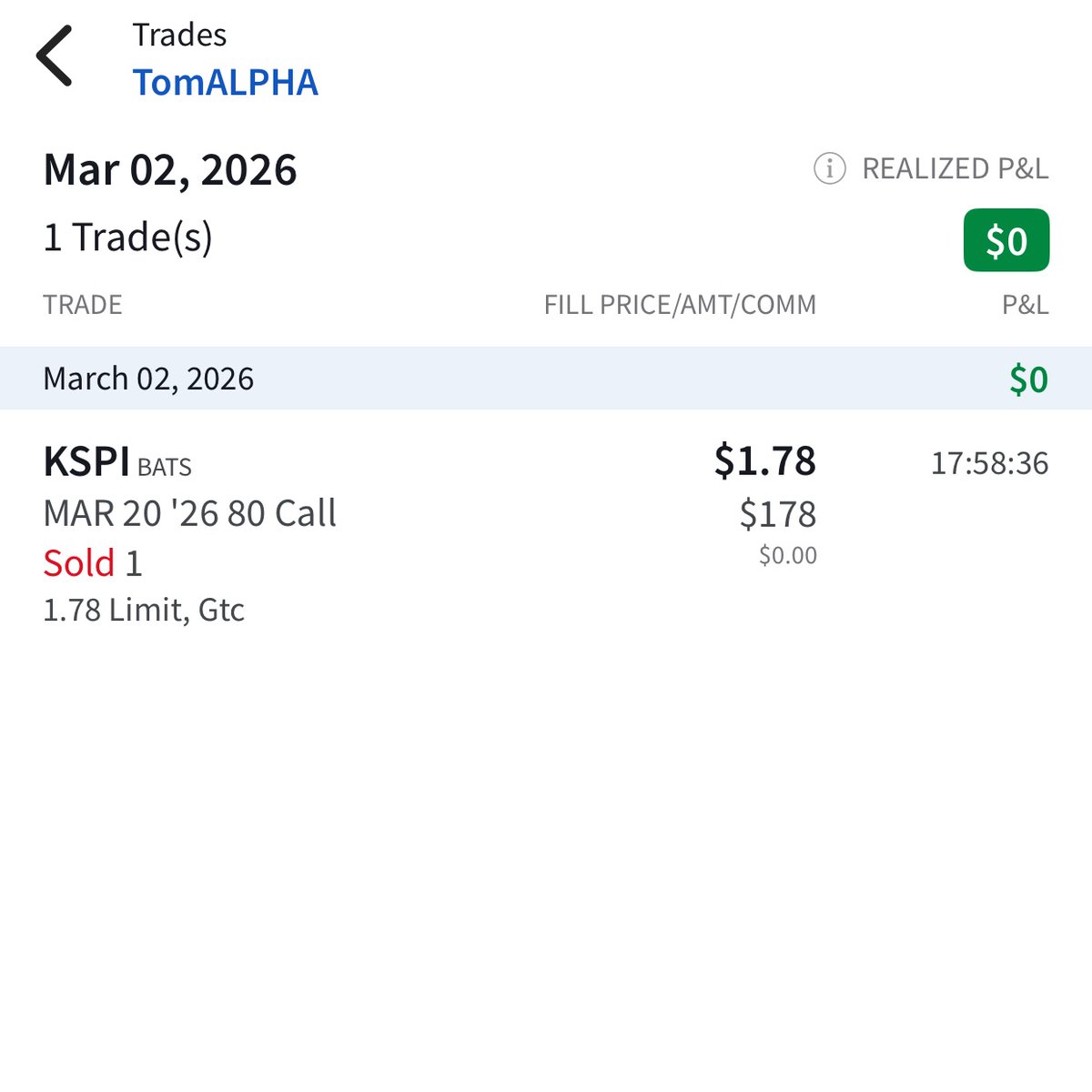

🚨 TRADE ALERT: Covered Call on $KSPI after strong Q4 run-up (+9% today!)

Just sold 1 contract MAR 20 '26 80 Call at $1.78 (limit fill).

This hedges part of my position while collecting premium after the sharp post-earnings rally.

Still holding the majority of shares — Q4 was excellent (revenue +19% YoY, net income +10%, TPV +19%, GMV +11%), dividends returning, Turkey accelerating.

But 2026 guidance was conservative (EBITDA +5%, higher taxes/reserves in Kazakhstan) → market took it as "sell the news" initially, I used the vol spike to write the call.

Core conviction remains high long-term.

Smart income play or too early to cap upside? 👇

$KSPI #FinTech #TradeAlert #Options

Bitcoin +5.6% to $69,393 — strongest daily move in weeks.

Decoupling from hawkish macro data (PPI/PCE), driven by ETF inflows ($1.2B+ last week), short squeeze (funding rates spiked), and risk-on rotation.

Short squeeze building + sentiment flip (fear index 65→38 in 48h) could push past $69k resistance toward $75k fast.

Early cycle strength or blow-off top? Your target? 👇

ISM Mfg Prices Paid jumped to 70.5 in Feb — highest since June 2022.

Producer inflation in manufacturing accelerating sharply again.

This is yet another hawkish data point after hotter PPI/PCE prints — disinflation narrative keeps getting challenged.

Reinforces "higher for longer" Fed stance: no rush to cut, yields should keep grinding higher.

Risk assets under short-term pressure until jobs data tomorrow shows cracks.

Markets still complacent — but this week's data cocktail is building a solid hawkish case.

More pain ahead or just noise? 👇

📥 Download the complete Nu Holdings Deep-Dive Analysis here: https://t.co/8sU1IoOSCh

What is your take on their Mexico expansion? Can they replicate the Brazilian playbook, or is the market too fragmented? Let me know your thoughts below! 👇

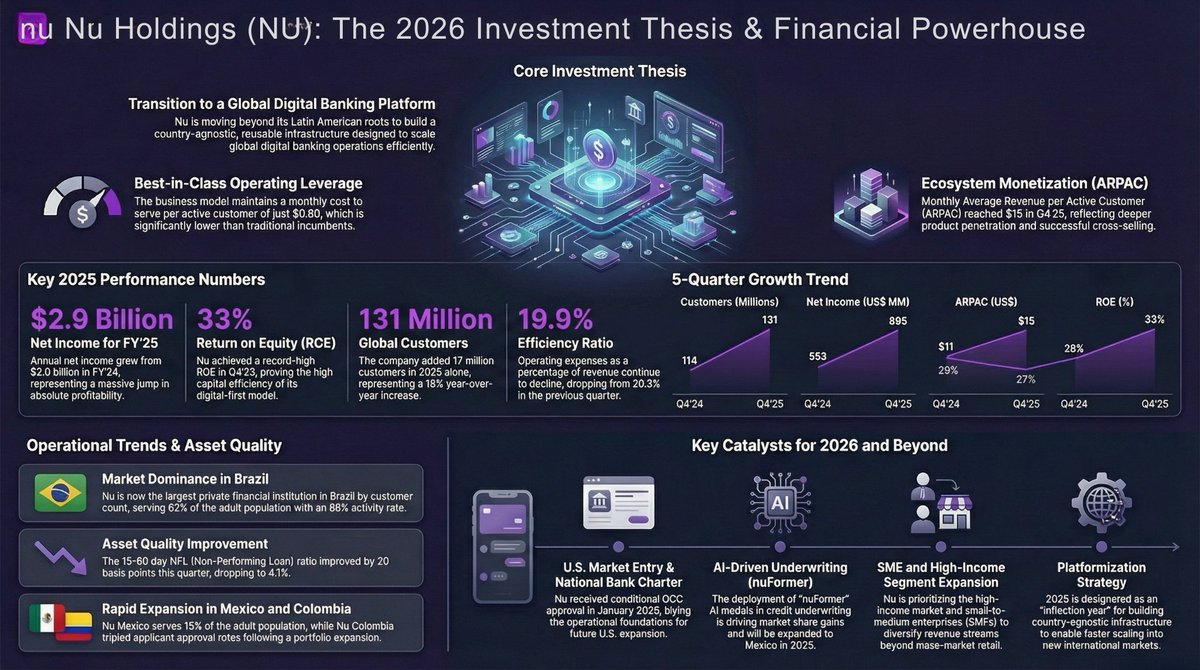

🚨 Wall Street is asleep on $NU

9.5% drop after blowout Q4? That’s not selling — that’s handing you a gift.

Market massively underprices Nu’s global banking platform shift.

Check the attached 2026 Thesis infographic 👇 – numbers speak loud.

TomALPHA just dropped our updated model. 3 reasons $NU looks extremely mispriced 🧵

1/ 🏦 Cash machine on fire

• FY25 Net Income: $2.9B

• Q4: $895M + 33% ROE (record)

• 131M customers (+18% YoY)

• $0.80/month cost per active user

Legacy banks are toast.

2/ 📈 2026 “OpEx spike” = rocket fuel, not risk

→ Mexico & Colombia exploding

→ US national charter approval secured (Jan 2025)

→ nuFormer AI underwriting already lifting margins

This is high-ROI spend to own multi-$B TAM. Wall Street misreads it.

3/ 🎯 Price Target: $20.50

Conservative DCF (full expansion costs + LatAm premium) → fair value $20.50

At ~$15 → market prices global flywheel at basically $0.

Huge disconnect.

Grab our full Equity Research deck FREE ⬇️

Link in first comment 👇

Bullish or bearish on $NU?

Reply “BULL” or “BEAR” + one reason why.

Best takes get reposted 🔥

#NU #Fintech #Investing

China is well-positioned if Iran flows get disrupted: 90% of Iran's crude goes there, but independent refineries have ample near-term stocks, oil in transit covers ~5 months, and strategic reserves provide ~200 days of import cover (boosted by discounted Iranian/Russian barrels).

Bottom line: manageable impact even in a worst-case scenario. No panic in Beijing — this is why oil spikes tend to fade fast on geopolitical noise.

Eurozone traders have priced out nearly all ECB rate cuts for 2026 — odds for Dec cut collapsed from ~40% Friday to just ~8% now.

Fastest sentiment flip in months. After hotter data prints, markets now expect no easing.

Tightening financial conditions could spill to US → higher global yields, EUR/USD pressure, less liquidity for risk.

Fed path just got trickier. Hawkish global alignment strengthening.

Overreaction or correctly priced? 👇

JPMorgan: "Buy the dip on Iran escalation" – classic Wall Street contrarian call.

They see it as temporary noise: oil spike fades fast, inflation stays contained, tech/AI repricing mostly done, limited further downside.

Favor international, EM and Eurozone equities over US for now.

After weeks of geopolitical fear premium, this is a reminder that real wars rarely last long in markets — dips like this often become the best entries.

Global debt exploding: +$29T in 2025 to record $348T — biggest annual jump since 2020.

Governments +$10T (US/China/Euro Area leading), corporate non-financial to $101T (AI capex boom), EM debt $117T with 235% debt-to-GDP (record).

Unprecedented leverage everywhere → structural "higher for longer" rates, fiscal dominance risk, EM vulnerability.

Bond yields face upward bias from supply flood. Markets still complacent, but this is the ultimate anchor.

Bubble or modern monetary reality? 👇

This is a massive policy reversal in real time. Potential refunds create sudden fiscal hole → higher deficits → more Treasury issuance → upward pressure on yields.

Supply chains rerouted during tariff era may never fully revert — permanent cost increases baked into many sectors.

Markets pricing "trade normalization" but real alpha is spotting which industries stay structurally changed long-term.

Bond bears love it; risk assets face volatility spikes as cases drag on for years.

Massive unwind opportunity or just headline noise? 👇

PPI hotter than expected: headline 2.9% YoY (vs 2.6%), core 3.6% YoY (vs 3.0%) – highest core since July 2025.

Another disinflation stall signal after last week's PCE. Reinforces "higher for longer" Fed narrative: March cut odds near zero, June under pressure.

10Y yields grinding toward 4.6–4.7%, risk assets face short-term headwinds.

Markets shrugging for now, but hawkish data tilt building fast. Bulls need tomorrow's jobs to show no cracks.

Inflation trap or just noise? 👇

🚨 TRADE ALERT: Re-entering $TUI1 – Standard Position Size

Just bought 1,700 shares of TUI AG (TUII) at average €8.086 (filled across TGATE/EUDARK/EUDARK1)

This is a standard position size → represents ~6% of the TomALPHA portfolio.

Original exit: sold out at €9.09 earlier

Re-entry: ~€7.50–8.00 range (strong dip buy on weakness)

Why now:

- Q1 bookings +9%, revenue +12%, EBIT turnaround accelerating

- Debt reduction on track, liquidity solid

- Summer 2026 season shaping up strong

- Stock down -40%+ from 2025 highs → oversold on macro/travel caution

- Technicals: multi-year support + RSI oversold

Target: €15 (≈85% upside from here) – based on normalized earnings, margin expansion and debt paydown.

Scaling in gradually on weakness, full conviction on the recovery story.

Waiting for summer bookings update and debt progress. If execution continues, this could be one of the best contrarian travel plays of 2026.

What’s your view on TUI at these levels — bottom in sight or more pain ahead? 👇

$TUI1 #Travel #TradeAlert #Contrarian

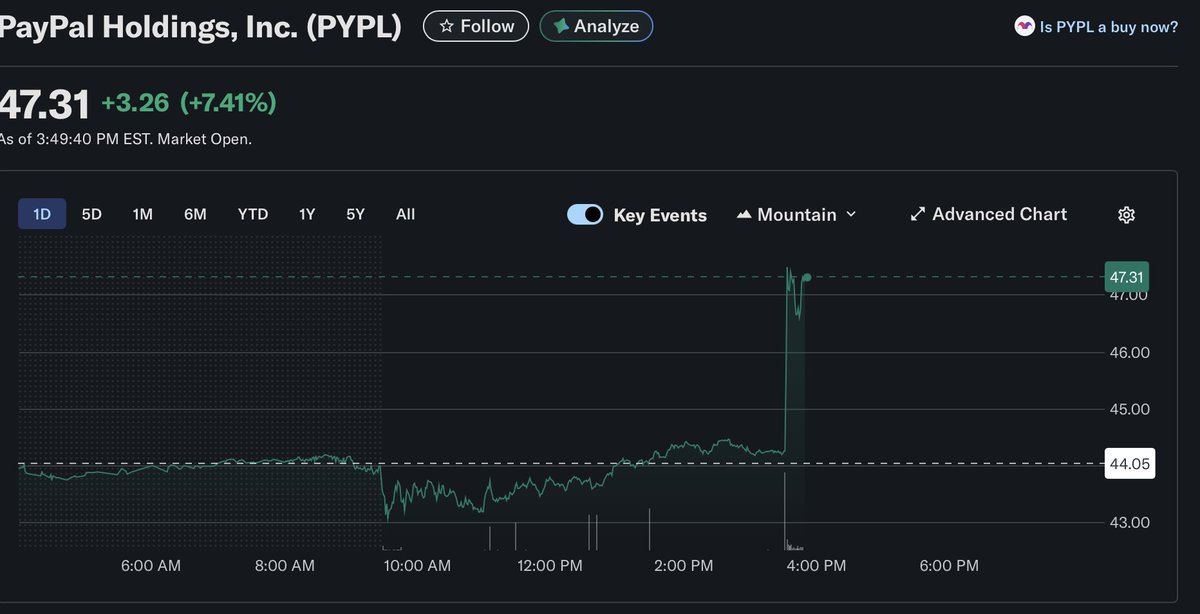

🚨 TRADE ALERT: Partial Profit-Taking on $PYPL

Just sold 100 shares of PayPal at $45.37 (filled on NASDAQ)

Original entry: $39.99 → Realized gain on this tranche: +13.46% (+$537 gross profit before fees)

Original position: 700 shares

Sold today: 100 shares

Still holding: 600 shares

PYPL has been brutally unloved for 18+ months, but recent M&A rumors (Stripe interest) sparked a nice bounce. Locking in profits on 1/7 of the position while keeping strong conviction on the core holding.

Waiting for more concrete developments on potential full acquisition or asset carve-out (Venmo/Braintree). If real deal materializes, 25–40% premium is realistic → $60–70+ per share target.

Core position remains open — will update on any fresh news.

What do you think — M&A lottery or still dead money? 👇

$PYPL #FinTech #TradeAlert #PayPal

🚨 Nubank (NU) Q4'25 Earnings: Massive Beat on Revenue & Profit 🔥 But Guidance Triggers Sell-the-News Dip 📉

Nubank delivered another blockbuster quarter with strong beats, but the stock is down ~1.3% in after-hours.

Q4'25 Key Results vs Consensus:

✅ Revenue: $4.857 billion → beat ~$4.55 billion consensus by ~7%

✅ Net Income: $895 million → beat consensus estimates

✅ ROE: 33% (all-time high)

✅ ARPAC: $15.00 (+27% YoY / +9% QoQ) → huge monetization leap

✅ Customers: 131 million (+17 million in 2025, +15% YoY)

✅ Efficiency Ratio: 19.9% (improving)

✅ Credit Portfolio: $32.7 billion (+40% YoY)

✅ Deposits: $41.9 billion (+29% YoY)

Full Year 2025 Highlights:

Revenue $16.32 billion (+45% YoY)

Net Income $2.87 billion (+51% YoY)

ROE 30%

What stands out:

🔥 Activity rate stable at 83% while ARPAC exploded → real monetization power

🔥 Cost to serve still only $0.80 per active customer → brutal operating leverage

✅ Asset quality improving (15-90 NPL down to 4.1%, 90+ NPL to 6.6%)

✅ Strong balance sheet: $38.8 billion available funding (2x net credit portfolio)

Business momentum remains insane:

🇧🇷 Brazil: 113 million customers (62% of adult population), largest private bank by customers

🇲🇽 Mexico: 15% of adult population + #1 new credit card issuer

🇨🇴 Colombia: >4 million customers, credit approvals nearly tripled

🔥 100+ new products + AI (nuFormer) driving record credit card market share gains

🇺🇸 US national bank charter: conditional OCC approval in January 2026

The Catch (Why the stock is selling off) 📉:

Management explicitly guided for near-term upward pressure on efficiency ratio in 2026 due to heavy investments in:

US expansion & national bank build-out

Platformization (country-agnostic infrastructure)

AI, SME/high-income segments, new products

Translation: short-term margin compression from big growth investments → classic "invest now, profit later" message that the market hates right now.

Bottom line: Fundamentals stronger than ever, but forward guidance created the dip. Looks like a textbook buy-the-dip setup for long-term holders.

What’s your read — overreaction or justified caution on 2026 margin outlook? 👇

$NU #FinTech #Earnings #Nubank

CME Globex halts trading in metals and natural gas futures/options due to technical issues — metals still down, nat gas reopening soon.

At the same time Jane Street just became the single largest holder of SLV ever: added a record 20.6M shares in Q4, now holding ~3.7% of the ETF (~$1.3–1.4B position).

That's one of the biggest single-quarter builds in SLV history from a quant giant known for high-frequency arb and liquidity provision. Combined with heavy options flow, this level of concentrated positioning screams potential volatility — either massive squeeze fuel or sharp unwind risk if flows reverse.

Silver bulls need to watch closely: huge leverage and engineered flows in play.

🚨 JUST IN: Stripe is eyeing a full or partial takeover of $PYPL — and the market is loving it.

According to Bloomberg, Stripe has expressed preliminary interest in acquiring the entire company or key assets (Venmo, Braintree, etc.). This comes right after PayPal’s brutal 46% stock slide over the past year and the recent CEO change.

Why this makes perfect sense:

- Stripe is now valued at ~$159B (tender offer this week)

- PayPal trades at a depressed ~$47 with massive scale (400M+ users, Venmo dominance)

- Perfect strategic fit: Stripe gets instant consumer scale, PayPal gets Stripe’s tech firepower and growth DNA

Stock reaction so far: +8–10% in two days. If a real deal materializes, analysts see a 25–40% premium possible → realistic target $60–70+ per share.

This could be the biggest fintech M&A catalyst of 2026.

What do you think — full acquisition by Stripe, asset carve-up, or just rumor fuel? 👀

$PYPL #FinTech #Mergers #Payments

Meta reportedly integrating stablecoins in 2H 2026 is huge — 3+ billion users across FB/IG/WhatsApp could drive massive on-chain volume for payments, creator payouts, and cross-border transfers.

After Diem/Libra flop, this comeback shows regulators are finally giving green light (GENIUS Act momentum). Bullish for USDC/Circle ecosystem and broader stablecoin adoption.

If executed well, this might be one of the biggest mainstream crypto catalysts of 2026. Game changer or still too early? 👀