Interestingly, I've published Q2 delivery estimates for the past eight years, and all eight were lower than the actual number, including this latest one. Somehow, Tesla keeps outperforming expectations in Q2.

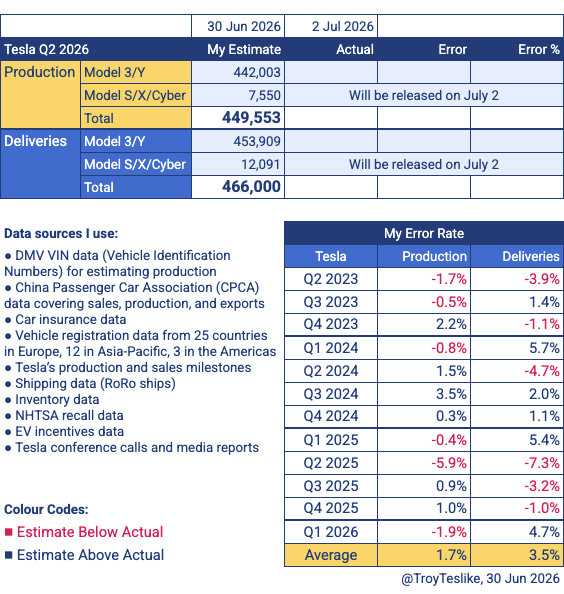

Hi everyone. Here are my Tesla delivery estimates for Q2 2026. The gap between my estimate and the analyst consensus is unusually large this time.

• My estimate: 466,000

• Analyst consensus: 406,024 (based on Tesla's survey of 22 analysts, known as the Company-Compiled Consensus, published on June 26)

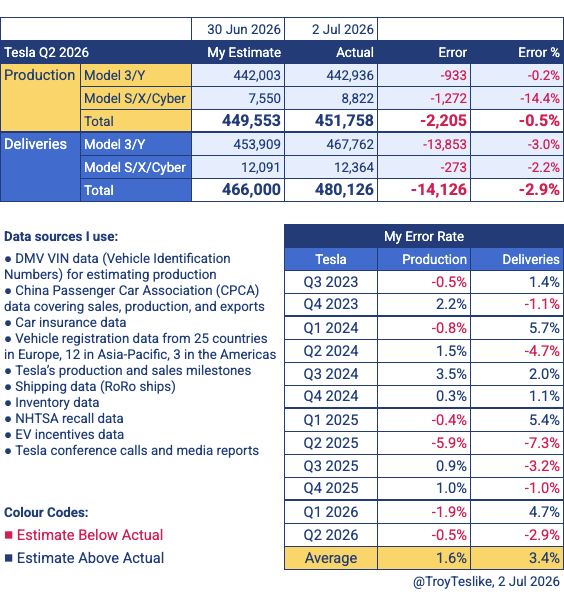

The actual numbers are in. Tesla delivered 480,126 vehicles in Q2 2026. My estimate was 2.9% too low, while the analyst consensus was 15.4% too low.

• Actual: 480,126

• My estimate: 466,000 (Error: -14,126 units or -2.9%)

• Analyst consensus: 406,024 (Error: -74,102 units or -15.4%)

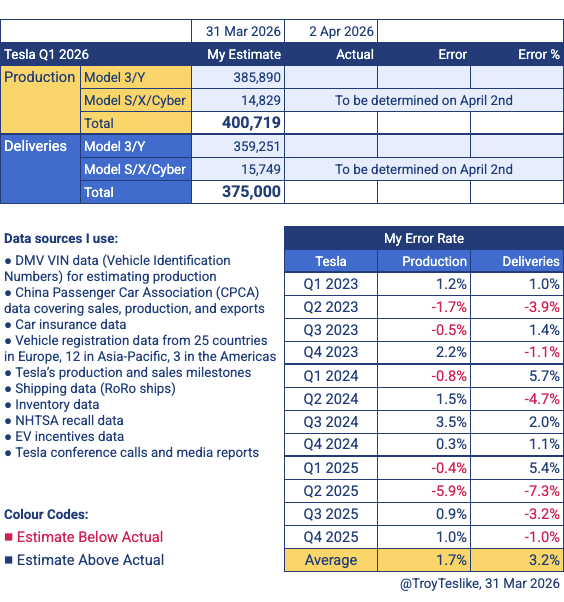

For deliveries, I was aiming for an error of less than 3%, so I'm happy with the result. My production estimate was even closer, with an error of just -0.5%. Production is easier for me to estimate thanks to VIN data.

@piloly@garyblack00 This is going to be interesting because I've published Q2 delivery estimates for the past seven years, and all seven were lower than the actual number. If my estimate ends up being too high, it will be my first time overestimating Q2 deliveries.

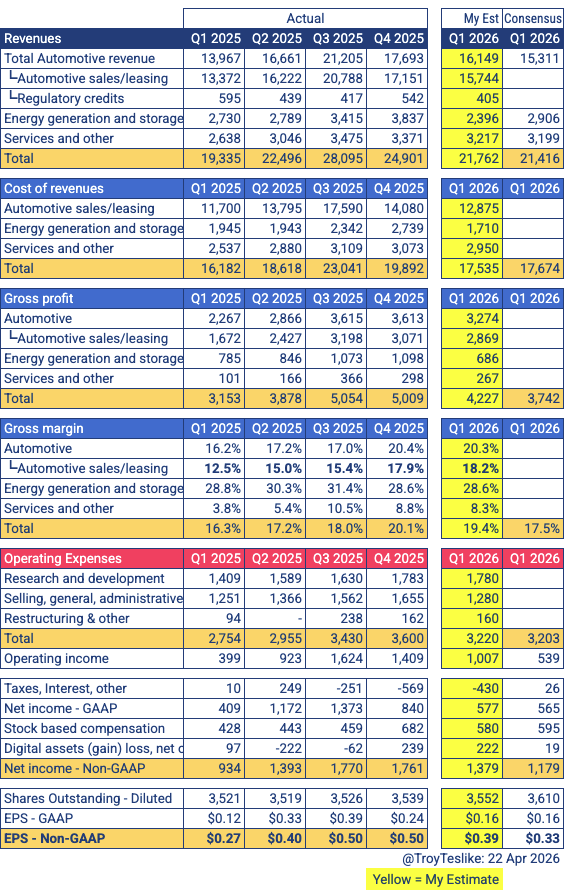

@funwithnumberz I expected automotive gross margin to improve, because the average sale price data for the US showed higher prices for both the Model 3 and Model Y in Q1 2026 compared to Q4 2025.

Here are my estimates for Tesla’s Q1 2026 earnings:

Non-GAAP EPS:

• My Estimate: $0.39

• Analyst Consensus: $0.33

The last two columns show my estimate and the analyst consensus. Tesla will report the actual numbers in a few hours.

The $0.33 analyst consensus is based on Tesla’s survey of 20 analysts, also known as the Company-Compiled Consensus, released on Tesla’s website on April 17: https://t.co/9xSyXOnUbK

@MorganHammar There are different surveys for the analyst consensus. The main ones are Tesla’s own survey (also known as the Company-Compiled Consensus), Bloomberg’s survey, and FactSet’s survey.

Tesla’s survey was published here. It shows the $0.33 consensus: https://t.co/KjhxrOScwU

Interestingly, the line “Digital assets (gain) loss, net of tax” does not reflect the Bitcoin impact. Instead, the impact is recorded under “Other (expense) income, net” and is included in GAAP net income.

However, non-GAAP net income excludes the Bitcoin impact, so it needs to be removed. That’s what the “Digital assets (gain) loss, net of tax” line does. It removes the Bitcoin impact, so it’s equal to it but in the opposite direction.

@lin627661 I was estimating automotive gross margin to improve because the average sale price data for the US shows higher prices for both the Model 3 and Model Y in Q1 2026 compared to Q4 2025.

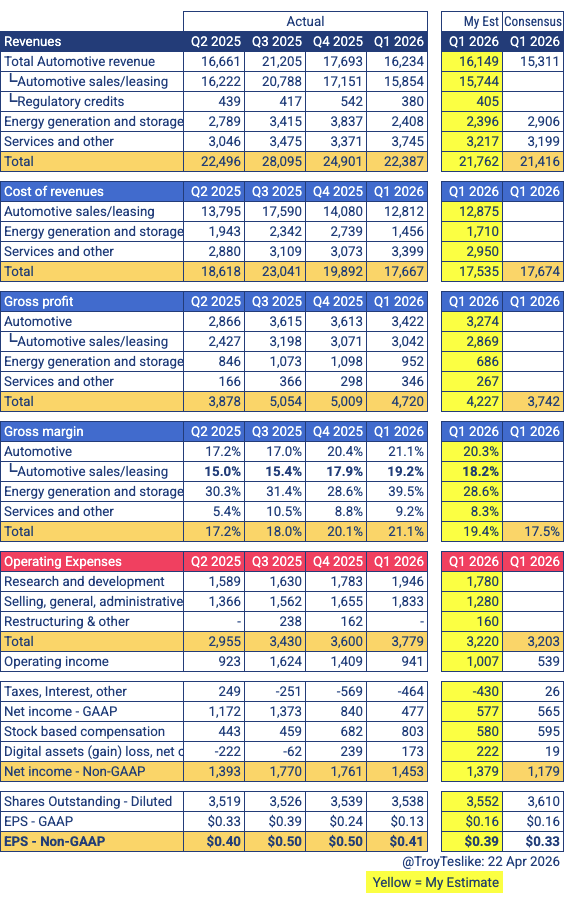

The actual numbers are in. Tesla beat the estimates.

Non-GAAP EPS:

• Actual: $0.41

• My Estimate: $0.39

• Analyst Consensus: $0.33

The last three columns show the actual results, my estimates, and the analyst consensus.

No, I didn’t change anything. We stopped getting weekly China car insurance numbers in mid-October 2025, which made estimating China more difficult. US estimates were already difficult due to limited data.

I expected Tesla to make reasonable adjustments to production, such as reducing output when demand is weak, but that didn’t happen this time. As a result, I overestimated despite being cautious.

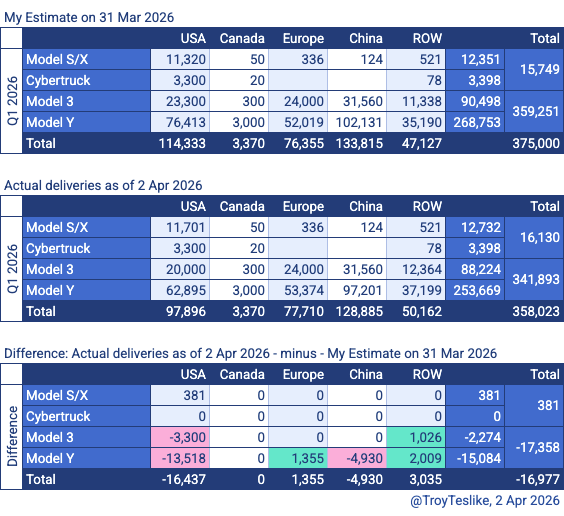

The tables show my estimates, actual deliveries based on the data available so far (China numbers are still missing), and the difference between the two.

Hi everyone. Here are the final Tesla delivery estimates for Q1 2026:

• My estimate: 375,000

• Analyst consensus: 365,645 (based on Tesla’s survey of 23 analysts, known as the Company-Compiled Consensus, published on Mar 26)

Last year, Q1 deliveries were 336,681 units, unusually low because of the Model Y Juniper transition. It’s a low bar to clear, though it’s still unclear whether full-year deliveries will exceed 2025.

Tesla’s Europe sales are trending stronger than usual. Q1 2026 deliveries in Europe (not global deliveries) are expected to surpass any quarter in 2025. The increase in demand may be linked to the ongoing oil crisis. For more details, subscribers can view the draft here: https://t.co/FyFHBwCFZo