$ODD Lower bound revenue estimate if CAC problem is not solved (which is highly unlikely) for 3 brands together = 774,5 million usd for 2026. Only a minor decrease from 2025.

70% margins + P/S ratio of 0.92. A PE ratio of <7 and 250 mln in buybacks amounting to -30% of float!🤯

$EOSE ☕️

Reflecting on JPM + Uk CnF

Mfg repeatability trending our way, FPUSA shifting project timeline risk, & backlog melting higher even assuming massive haircuts…

Start with backlog. Entering the period: ~$640M

CnF: just awarded 250MWh minimum~$70M. 🔑

Busby & Ayr moving forward: ~1.5GWh / $375M gross. Haircut once = $187M

Haircut again to be ultra-conservative = ~$90M.

Bimergen-400MWh in ERCOT- the first PO under the 2 GWh FPUSA reservation. +$112M.

Net out ~$70M of revenue (backlog burns as you deliver): $640M + $70M + $112M − $70M ≈ $750M reported floor.

Add Ayr/Busby ~$840M. Double haircut figure…

The tell isn't the level.. it's the direction. Backlog grows ~$90M (+17%) even after recognizing $70M in revenue. Bookings are outrunning burn better than 2:1. This excludes Ayr/Busby..

And this floor counts zero from the rest of the board: Talen, MN8, Turbine X, Stella, NYSERDA, + Duke / Dominion / NextEra / DoD + Misc..

The market is still waiting on a marquee order -any one conversion will rerate.. don’t sleep on it forever

Here is the part of the eos story many miss… project execution & customer acceptance timing are THE margin variable right now. This is why joe hammered it at JPM.

Two companies can have the same $840M backlog & be very different stocks. One that converts it cleanly vs. one that recognizes slowly in fits…as sites & customers lag. The size of the backlog is directionally going higher.. but the speed backlog flows thru to revs is what drives margin. That part has been and still is unclear.

But here is why that risk has a shelf life. Joes focus on timelines is itself the tell… demand is still early enough that individual project schedules dictate the factory. That flips with scale, more orders, a single fungible SKU + FPUSAs capacity reservation.

This means that production decouples from any one project.. just build continuously and ship to whichever project is ready.

So.. as backlog builds organically.. Thornhill scales, L1 gets more efficient, FPUSA will be the multiplier.

The headline is financing but the second derivative is handling timeline/execution risk as Eos can build batteries against the reservation instead of a specific customer timeline/readiness..

Eos needs to control the controllables FPUSA absorbs the uncontrollable

The obvious pushback to “just scale”..can Eos actually add capacity fast and reliably enough for the “decoupling” via more capacity to be real..?

That is why the mfg proof points matter more than most think. L2 went live and hit on day 5 what L1 took 6 months to reach. Production is repeatable. And repeatability is the asset

Consensus calls TC a sunk cost pet project. Lazy.

“Not profitable yet” is about timing, not a ceiling- and Joe is still taking cost out of L1 while Thornhill ramps. You don’t optimize a line you have written off. My bet: TC is additive even if it never matches Thornhill bc it doesn’t need to be the best line- it has to be an accretive one. 🔑

Writing it off before margins play out isn’t a call; it’s a shoulder shrug…

L1 10 second cycle times. L2 9 seconds. At least we know new capacity isn’t static… (Cost out working…) L1 is still being optimized.

Finally…the RO overhang will clear this week and Eos will have a vehicle where they could finance projects up to $2B very soon… FPUSA engaging with KKR as a structuring agent for its debt program to design & syndicate the stack is a subtle tell..

Although the RO overhang has lasted longer than many of us would like.. we will be happy a yr from now eos was able to keep this financing value in house… + RO finalizing will shift focus back to execution.

Net/Net- backlog is outrunning burn, mfg repeatability is improving, FPUSA may be the bridge between demand and bankable project execution. The stock is still in grind mode but the setup will become less about can they get orders… & more about can they convert them cleanly.

That’s a better problem to have…

@x_times_1@kaliva09 Honest quest. Isn’t refraining from that expected outside of official earnings releases and calls after the Q4 mess and ongoing lawsuit because of that?

The official statement of exceeding production targets of L1 in less than half a year is a good indication they are on track

$EOSE

At an average sales price of 240$ per KWH > these combined orders of 2.8GWH + 520MWH = 3.320.000 mln KWH > would lead to a backlog increase of 767 million dollars. Surpassing the current total BL of 700 mln.

Is this napkin math right?

$EOSE

Frontier wins 520 MWh system in Wales under UK Cap and Floor scheme and will work with Ofgem during the consultation to flip others.

They also indicated they're nevertheless moving forward with the 2.8 GWh for Ayr and Busby in Scotland using Eos batts, as the projects are already advanced. Just a question of whether the payment scheme will ultimately fall under Cap and Floor or not. And I guess that's not really Eos' problem.

This is happening with $EOSE over and over again. Some of the biggest bulls become the biggest critics only to turn bullish again when it serves their holdings.

Their are beacons of hope in the community though being realistic no matter the PA.

Snelste weg is verwerpen Box 3

Als we dit aanvaarden heeft Financiën geen enkele haast meer om snel te komen met vermogenswinstbelasting

De druk valt weg

Eenmaal aangenomen wordt deze slechte wet niet meer ingetrokken

@NOS@nu@ADnl@volkskrant@trouw@fd@nrc@BNR@RTLZ

@JanMe32@Jansen_MWH@TheoBuysStocks Dit artelijke denken helpt heel het land naar de klote. Niemand kan de markte door decennia heen altijd goed peilen. Zeker niet in deze tijd. Dan heb je nog de marktconjunctuur die door niemand met zekerheid te voorspellen is. Het is geen arbeid met een vaste uitbetaling.

$EOSE 🧵 Future valuation

Sitting in a coffee shop in the town I grew up in.. have a wedding in a few hours (tux all set)..

Zooted out of my mind on ☕️ … and this is what is going to be the picture 5 months from now.. and how the mkt will value Eos… 😁

The credibility shift is here. Revenue ramp this year: Q1 $57M Q2 $70M Q3 $75M (L1) + $17M (L2) Q4 $80M (L1) + $35M (L2)

~$332M from both lines = they hit guide.

That changes everything.

Why this matters: Joe & co missed revs last year, so the street slapped a credibility discount on the name. Hitting guide is the first domino. That discount starts closing the moment the picture gets clear

Now the backlog. Currently $645M

What converts over the next 2 quarters (assuming $250/kWh)

Bimergen: 450MWh -> +$112M

Germany: 750MWh -> $187M

NYSERDA by YE: 1GWh -> $250M (conservative)

Talen: 1GWh (at least) = $250M

Mn8: 500MWh = $125M

Turbine X: 700MWh = $175M

Misc microgrids + hotels: 300MWh = $75M

~$1.2B (new backlog) on top of the $645M

= ~$1.8B. Net of revs ($332M) the rest of the year (2026) = exit 2026 with ~$1.5B backlog.

Here's the key insight that lets us actually model EOS again:

$330M revs but ~$1.2B booked = a 3.6x book-to-bill.

Apply that multiple forward. 🔑

2027: if EOS does $650–700M and books ~3x revs, that's +$2B in new orders next year alone.

Nameplate: exit 2026 at 4GWh, likely add another 2–4GWh in 2027 -which keeps pushing terminal value higher.

Where we are today: ~20% credibility discount baked in. $7.50 × 1.2 = ~$9 fair value right now.

The flywheel from here: hit revs -> grow backlog at 3x ->close the credibility gap -> upgrade counterparty quality ->FPUSA cash flows get clearer (wildcard) -> margins flip back (late this yr / early next) -> market finally gives EOS credit for the quarters ahead. 🔑

$330M this year -> $680M next (2027)

Now model 2028: ~$1.2B revs, 8GWh nameplate, backlog north of $3.6B (that 3x book to bill), geographic + customer diversification, higher-quality counterparties, cleaner balance sheet, Thornhill full steam+ maybe a 2nd site (TX or UK/Germany).

2028 unit economics:

$250/kWh - $200 COGS + $45kwh credits -> ~38% GM

OpEx was $115M (2025) last yr, grows approx ~25%/yr -> $143M ('27) -> $179M ('28).

-> ~$280M EBITDA.

Subtract Opex by 38% Margins to top line (include credits)

= Massive inflection. 🔑

Now…30x EBITDA (low, imo, given the growth + magnitude of change) = ~$13 PT.. Very soon.

But… the street will be looking past that (‘28) - to 2029.

2029: ~$2B revs, backlog ~3x revs.

$800M GP − $223M OpEx = ~$600M EBITDA… give EBITDA a 30x

->EV ~$18B. ÷ 600M FD shares = ~$30….likely priced in by Q1/Q2 2027.

VERY binary. 🔑

The kicker:

The algos price the outstanding count, not FD.

Here is how the mkt “may” view

The float…

-> The mkt/buyside/sellside likely pricing ~450M shares (just using a weighted avg of FD and actual outstanding count bc the picture is always a bit gray when there is a higher delta between FD and outstanding.

(The algos do a lot of the work anchoring to current outstanding count… not the fundamental analyst fwiw)

Anyway.

$18B EV - ~$600M debt ÷ 450M shares = ~$40 PT and that can get priced as early as Q1/Q2 next year as the credibility gap closes imo

The change in fundamentals, credibility, and perception is why I am long in size.

It’s almost July 4th y’all.

U.S. on @ 3 today 🇺🇸 🔋

The first Eos Cube built entirely with batteries from Battery Line 2 has shipped.

The batteries were produced at our Thorn Hill manufacturing facility, where we moved from Site Acceptance Testing into commercial production in four days. The Cube was assembled at our Turtle Creek facility.

Two battery lines are now running. Line 1 surpassed its full-year 2025 output in 164 days. Line 2 is launched and delivering.

This is scale meeting execution on the path to 4 GWh of American-made annual capacity.

$EOSE Today's Redbird announcement gives three important signals.

Most immediately, the 400 MWh order is being applied against FPUSA's 2 GWh capacity reservation agreement. That confirms the reservation agreement is now being utilized by an actual project rather than simply sitting as reserved manufacturing capacity.

The announcement also notes that this order brings fulfillment of the 1 GWh Bridgelink MSA to nearly 50%. That suggests the Bridgelink relationship is progressing from framework agreement to meaningful volume.

And then there is the reference to an additional 12 GWh development pipeline spanning ERCOT, PJM, CAISO and MISO. That number caught my attention.

One question I would love management to clarify: What exactly does the 12 GWh represent?

Is this a Bridgelink-controlled development pipeline? A broader FPUSA opportunity set? Or simply projects under evaluation where Eos technology may ultimately compete?

To me, that may be the most important takeaway from today's announcement. It suggests Redbird may be the first project emerging from a potentially much larger opportunity set.

https://t.co/oiAhnUkOhi

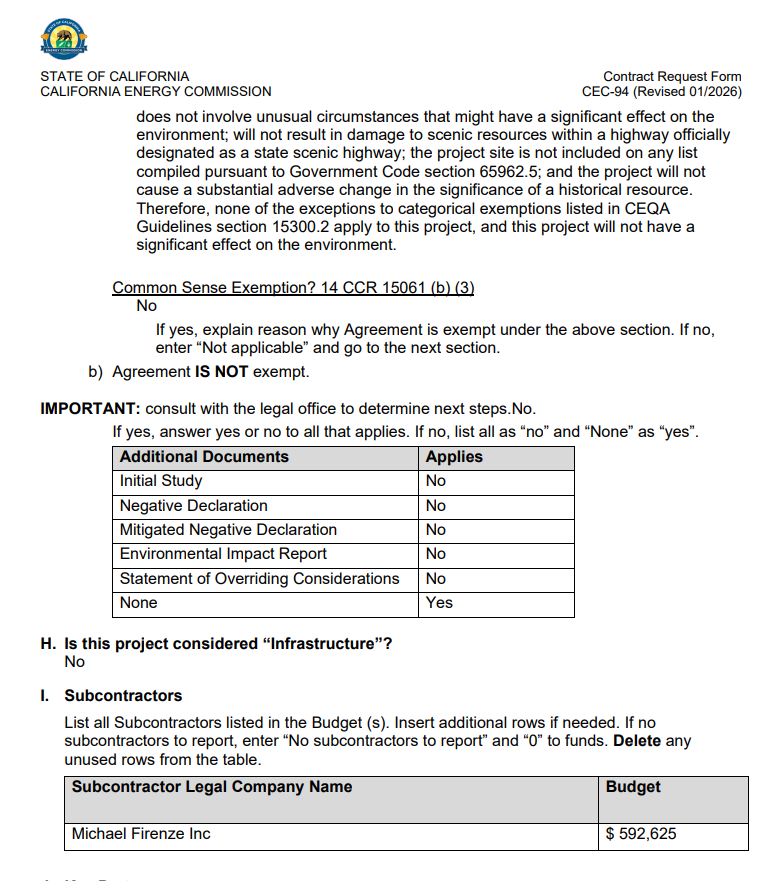

$EOSE

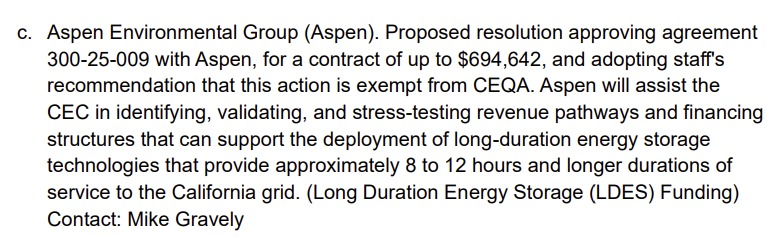

On the CEC agenda for upcoming Business Meeting: contract for $694k to Aspen for "identifying, validating, and stress-testing revenue pathways and financing structures that can support the deployment of long-duration energy storage technologies that provide approximately 8 to 12 hours and longer durations of service to the California grid. (Contact: Mike Gravely)

Main subcontractor: Michael Firenze Inc

Also Michael Firenze: Executive VP, Engineering and Construction of IEP

IEP has a 14 GWh pipeline in California.