❗️Let's Talk About Something Serious

"What concerns me most is that many of the datasets now being used to call a bottom are largely the same datasets that were previously used to predict last year's market top."

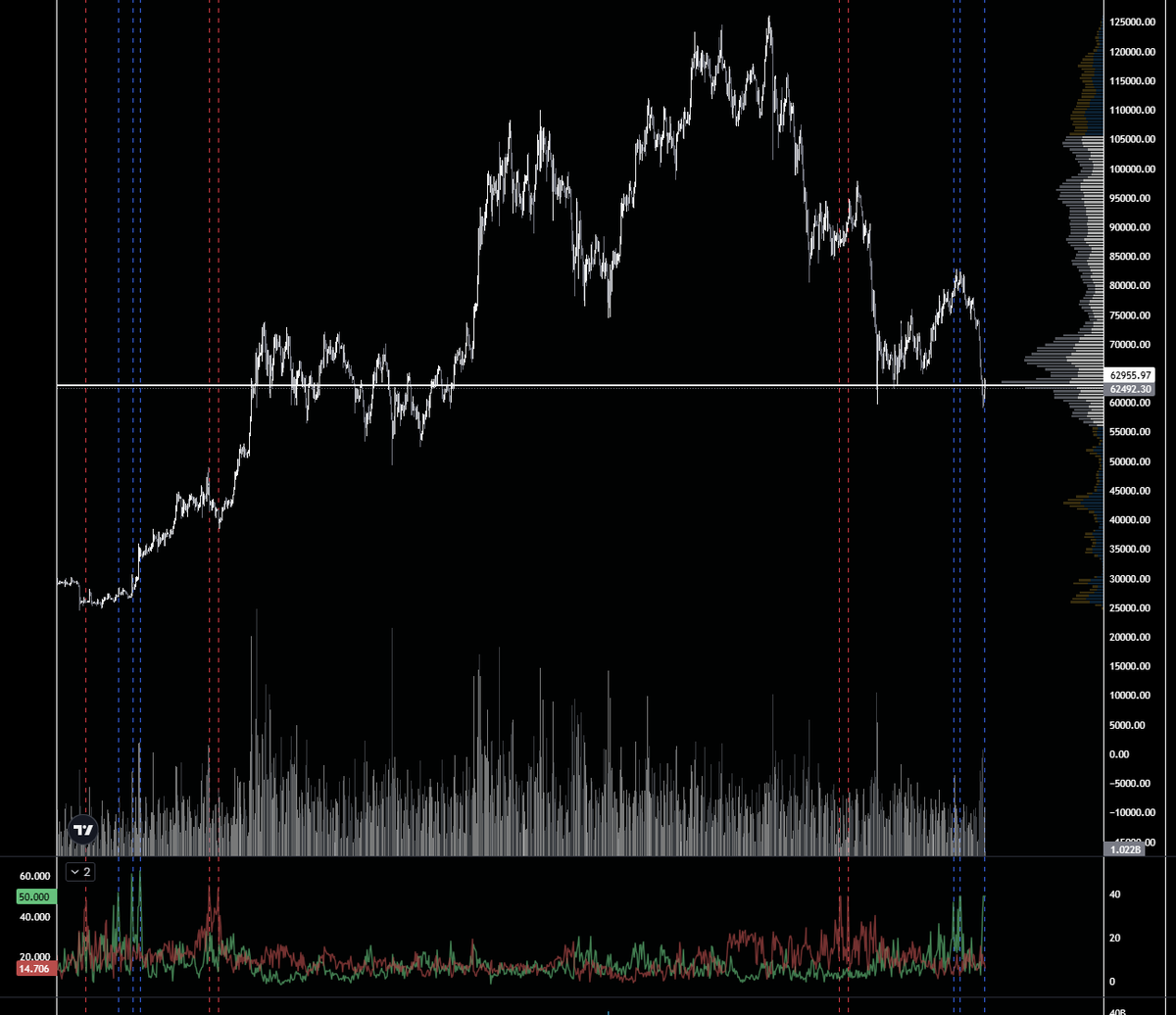

The market continues to move in the direction I have been concerned about.

Bitcoin is barely holding the $60,000 level, but personally, I do not believe this area will hold for very long.

Since last week, I have repeatedly stated that conditions are becoming increasingly serious, and my view has not changed.

Today, I want to discuss two major concerns I have about the current market, as well as some thoughts on how market data should be interpreted in the post-ETF era.

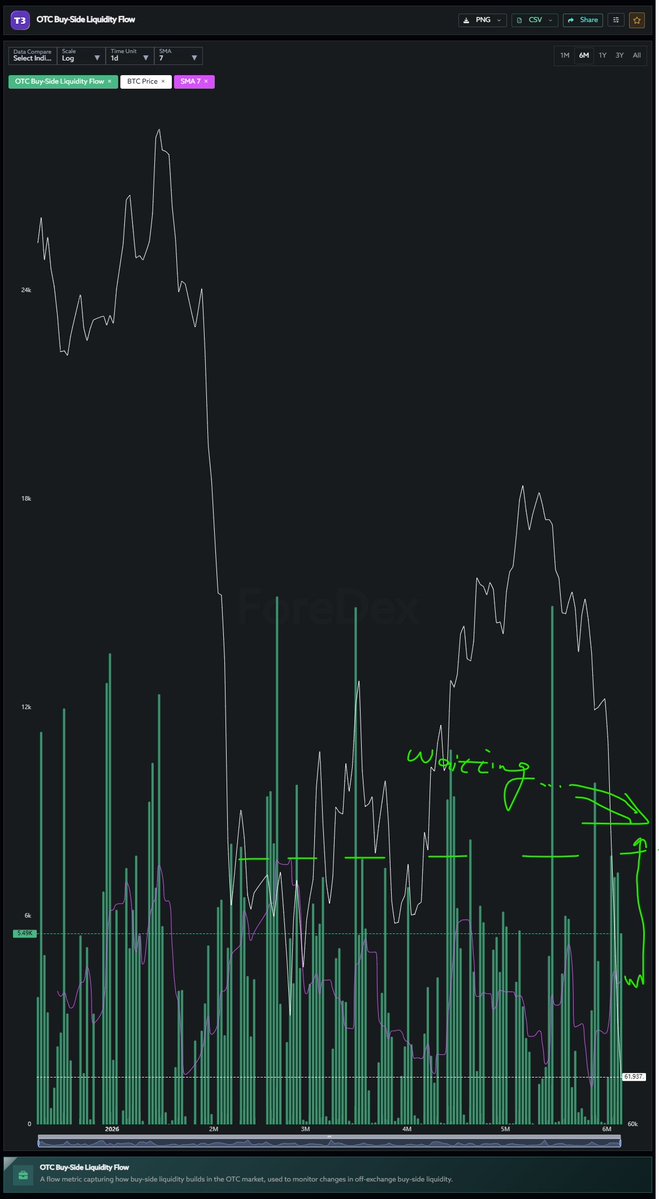

✅Concern #1: Liquidity Conditions Are Extremely Weak

liquidity flows that became especially important after the approval of the Bitcoin ETF continue to deteriorate and are now at some of their weakest levels.

So what about the liquidity indicators that were important before ETF?

Unfortunately, they are not telling a different story.

If market conditions were deteriorating while major players were quietly accumulating positions in the background, the situation would be different.

In that case, one could argue that the classic idea of "buying when others are fearful" was actually being put into practice.

That would be a constructive signal.

However, the data is not showing that behavior.

Objectively speaking, conditions continue to worsen.

✅Concern #2: Investor Psychology Remains Surprisingly Optimistic

The bigger issue is that many retail investors do not seem to view the situation this way.

While liquidity conditions and market data continue to deteriorate, the narrative being repeated across the market remains:

"Bitcoin has already fallen enough."

"Everyone is panicking, so this must be the bottom."

"Every crisis eventually becomes an opportunity."

"This is a buying zone."

I believe this is extremely important.

There is a significant disconnect between actual buying liquidity and what investors expect to happen.

In my experience, during periods of genuine fear, people do not openly talk about buying opportunities.

Instead, confidence disappears.

People become afraid even to discuss the possibility of a bottom.

Yet today, many participants continue to interpret the market through the lens of past experiences.

In other words, many still believe that the market remains within a predictable framework based on previous cycles.

To me, that is precisely what makes the situation more dangerous.

❗️Rethinking Data Interpretation After ETF Approval

✅1. Market Structure Has Changed Since ETF Approval

approval of Bitcoin ETF fundamentally changed trading behavior and market structure.

Those changes have also had a meaningful impact on on-chain data.

I recognized this shift last year and have been developing new datasets and analytical frameworks based on this new environment.

For more details, I recommend reading the ForeDex "Insight Report" referenced above.

The key point is simple:

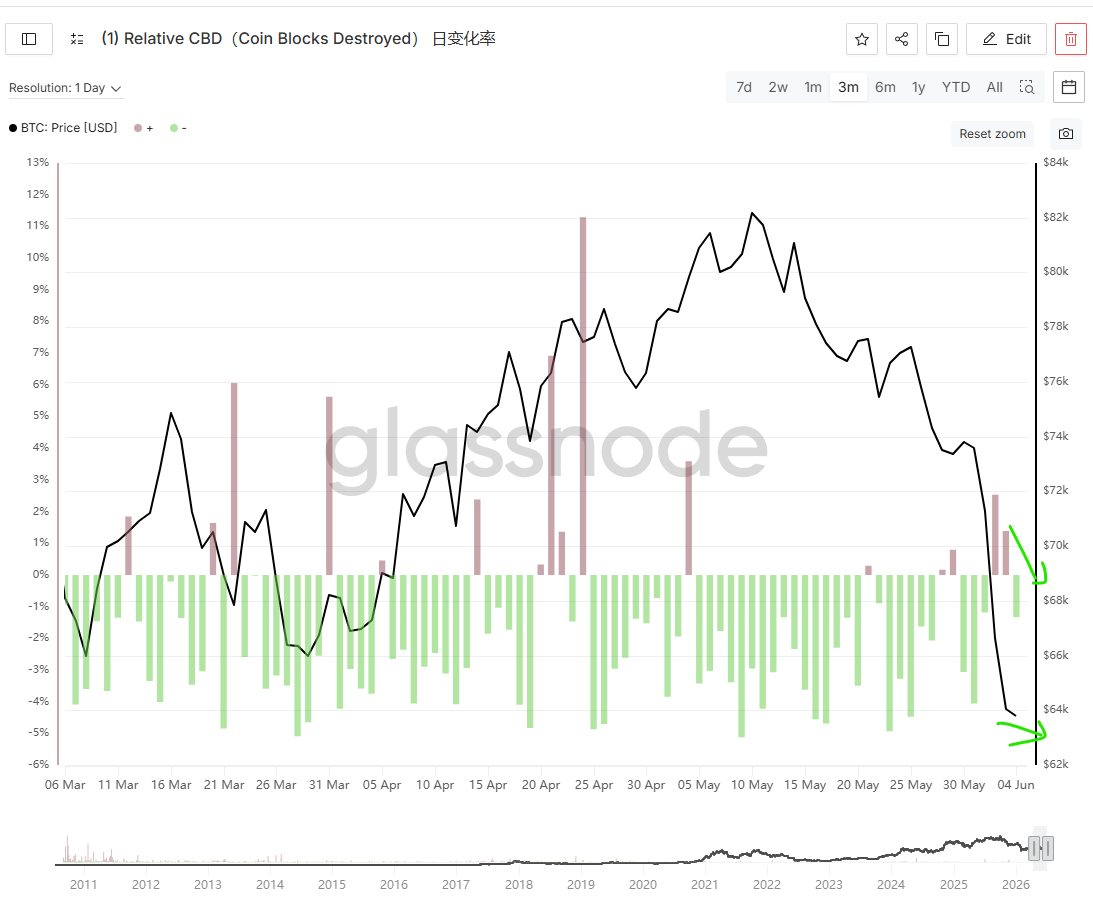

Many datasets that historically carried a high level of reliability no longer behave the way they did in previous cycles.

Technical cycle indicators, on-chain cycle indicators, and market cycle indicators all produced results that differed significantly from historical expectations.

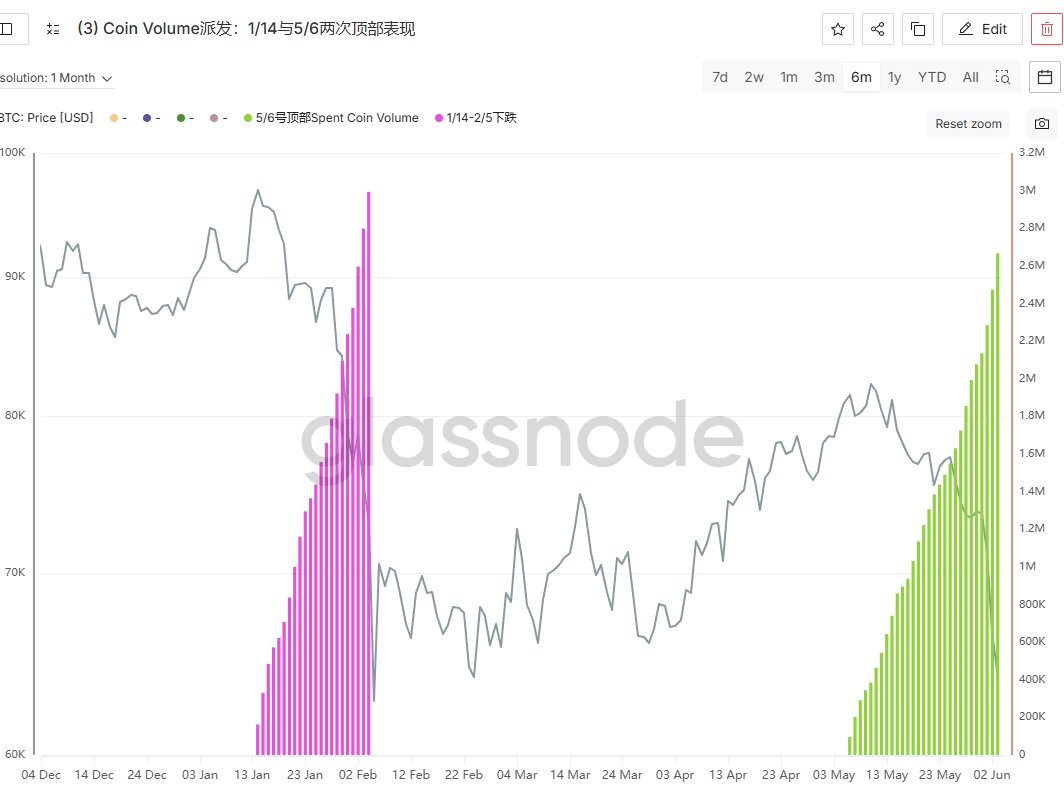

We saw this very clearly around last year's market top.

✅2. Think Back to Last Year's Market Top

At the time, the market was filled with discussions about the "Banana Zone."

Many investors built detailed plans around various cycle indicators:

"I'll sell when price reaches this level."

"Then I'll rotate into altcoins."

"Then I'll rebalance my portfolio."

These were not vague ideas.

People had specific roadmaps.

But did the market actually follow those expectations?

Not at all.

When I raised concerns about this at the time, the response was mostly criticism and dismissal.

Yet in the end, the market did not behave the way most participants expected.

✅3. If the Framework for Identifying Tops Has Changed

If ETF approval changed the way market tops should be identified, then our approach to interpreting data must also change.

If existing frameworks no longer work, new frameworks are needed.

If existing datasets no longer provide reliable answers, new datasets must be developed.

This is where the real problem begins.

✅4. We Are No Longer Looking for the Top — We Are Looking for the Bottom

Today, market participants are no longer trying to identify a top.

They are trying to identify a bottom.

And numerous arguments are now being presented to support bottom-calling narratives.

But here is the contradiction.

Many of the datasets currently being used to argue that a bottom is forming are largely the same datasets that were previously used to predict last year's market top.

This is what concerns me most.

If those datasets failed when identifying the top, then we must at least consider the possibility that they could also fail when identifying the bottom.

Yet the market largely ignores this possibility.

The assumption seems to be:

"They failed at the top, but they'll work at the bottom."

I believe that assumption is dangerous.

✅Conclusion

Taken together, market conditions continue to deteriorate.

Yet many investors continue building plans around datasets and frameworks that previously provided clear signals but ultimately failed when it mattered most.

That concerns me deeply.

Markets do not move according to our plans.

The same frameworks that failed to identify the top are now being reused to identify the bottom.

As retail investors become smarter, the dominant market participants become even more sophisticated, more strategic, and more capable of exploiting expectations.

The implication is straightforward.

Even if a major price shock occurs, the market is unlikely to unfold the way most participants currently expect.

In fact, when everyone is using similar frameworks and reaching similar conclusions, the probability of a larger shock may actually increase.

And even if the market eventually moves in the expected direction, there will likely be extreme volatility designed to shake investors out of their positions and cloud their judgment along the way.

We do not need to look very far back for evidence.

Even during the April–May period, the market repeatedly created one deception on top of another, constantly manipulating investor psychology.

And it worked.

If investors can be misled so effectively within a structure lasting only a few months, can we really be confident that a multi-year cycle will unfold exactly as the majority expects?

I am not convinced that it will.