Guys, this profile has gone dead for a while as I morph into a new role.

Will be back with hopefully lot more - just a bit different. More focused on energy transition opportunities globally, particularly in tech & autos

Thanks for your participation so far, I appreciate it🙏

@HDFCERGOGIC Everyone knows that Corporate greed runs rampant in this country. Can still deal with it on Dalal Street but when it turns against honest tax paying middle-class citizens on the main street, its worth at least reporting the same. @HDFCERGOGIC is just one example of the same

@HDFCERGOGIC If you are still able to prove them wrong, I won’t be surprised if @HDFCERGOGIC goes even further back and asks her to prove that she wasn’t born with cancer or heck! even born at all. This is an idiotic chase down a rabbit hole. Are there any avenues to address such grievances?

@sahneydeepak Mkt may do its jing-bang but fwiw results not bad at all imho (nor the valuations)+ FY25 guidance (reiterated today) looks quite achievable to anyone who knows the basic seasonality/one-offs in this biz .... so, most likely your call will work

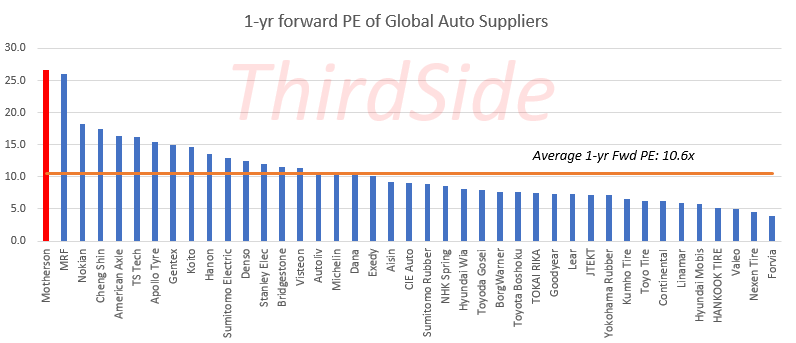

Last but not the least, the outlook appear particularly dreary for European auto suppliers like Motherson since West Europe is likely worst hit with OEM production estimated at -6%YoY by S&P Global (China & America see modest growth).

Motherson is a global auto supplier like the rest in this chart. You don't need rocket science to figure out the extent of overvaluation in India but let me give some colour anyways. (1)

Auto suppliers are driven primarily by Auto OEM volumes. S&P Global 2Q24 production estimates were downgraded last week from +2.6%YoY earlier to 0.5%. 2024 Light Vehicle production is now seen contracting 1.1% (2)

Globally, investors are nervous about auto suppliers due to likely OEM volume decline but recent comments from Stellantis on supplier cost savings are also creating margin worries i.e. margin squeeze by customers (3)