I'm a CPA. Not an engineer. The best thing I did was ignore that label and just start building. Supabase + Vercel + Claude = more leverage than any certification I've earned.

what is agent looping

for the last two years we prompted agents one task at a time. that is starting to change

instead of asking an agent to build the landing page and then driving every step yourself, you set up a loop that handles discovery, planning, the work, checking, and iterating until the goal is met

looping is a setup you build. almost any agent harness can run it, it just depends on how you wire it up

at its simplest, looping is one agent working on itself:

> researches

> drafts

> checks the draft against a goal

> fixes what is weak

> runs that cycle again until the work clears the requirements

you are not prompting each step anymore. the agent repeats the cycle for you

the bigger version is a fleet looping. you give an orchestrator agent a goal, it breaks the goal into pieces, hands each piece to a specialist agent, and those specialists hand smaller jobs to their own subagents

the whole tree keeps looping through discovery, planning, execution, and verification until the goal is met

one agent looping is like a person redoing their own draft. a fleet looping is a whole team running a project end-to-end

you create a goal, and the system runs the loop until it finishes within the reqs you set

open and closed looping:

OPEN LOOPING is exploratory. it still has conditions and a goal, but you give the agent or the fleet a wide space to move in. it can try different paths, discover things, build something you did not fully spec out

this is the exciting end, it is what Peter and others are doing, and tbh it is where I want to spend more time

the catch is cost, an open loop with real room to explore burns an insane amount of tokens. for the 90 percent of people without an unlimited budget it is not runnable yet, and pointed at projects with a loose standard it turns into a slop machine

CLOSED LOOPING is bounded. a human designs the end-to-end path first:

> clear goal

> defined steps

> an eval at each step

> a point where it stops or hands back to you (and feeds back performance data)

the agents still loop, but inside framework you built. it gets better every run because each pass feeds the next, and it runs on a normal budget because the path is tight.

for most marketing work, closed is the one that pays off today.

> the orchestrator owns the goal

> the specialists own the steps

> the subagents do the narrow work

> an eval gate make sure its not slop

Andrej Karpathy spent 2h showing how he actually uses AI day to day

he's a co-founder of OpenAI and led AI at Tesla, so when he shows how he works, it’s worth watching

and the whole session is just him telling the machine what he wants in simple terms, like he's briefing a coworker

watch what's actually happening the entire time:

> he describes the task in normal words

> it goes off and does the work

> he glances at the result and nudges it with one more sentence

that's the whole skill, and you've had it since you learned to talk

the only gap between that and a worker that runs on its own is handing that sentence a schedule and the tools to act

check his work, then build the version that keeps working when you stop

The Iranian-backed Houthi terrorist group in Yemen confirms tonight’s missile attack against Israel, which they say was carried out jointly with Iran, while declaring a “complete and total ban on Israeli maritime navigation in the Red Sea.”

The most basic way AI could blow up imo. I'm not saying it does but this is the most obvious way I can see it happening

- Per seat subscriptions are massively subsidized. The flat fee was priced way below what heavy usage actually costs

- For real business use you have to move to the API anyway. Data protections, work integrations and compliance officer approval

- On the API you pay metered rates, and businesses are burning credits way faster than the per seat pricing ever led them to expect

- This is everywhere right now. Internally for us, Codex users, Uber torching its entire 2026 AI budget in 4 months, the Microsoft comments. Just go try an API

I shared more on this here: https://t.co/iZrqrCAIRW

- And I don't think most businesses have the money to keep paying increasing API rates without a real change to how they operate (caps needed)

- Because they have a cheap alternative. They can reach open source models through any aggregator (OpenRouter, Venice, Baseten, Together) and still get strong privacy. Venice private data centers, or E2EE/TEE serving GLM 5.1.

More on open source inference provider raises here: https://t.co/7kf56P44yQ

- And the discount is enormous. DeepSeek V4 codes within a hair of Opus on SWE bench at roughly 1/30th the price, and the cheapest open models run closer to 1/100th

- Chinese labs open source frontier grade models. The model is the single biggest cost an inference provider has, and they get it for free

- This idea dies if China goes closed source. That is actually bullish web2 AI labs, because if everyone is closed you pay up for the best intelligence. China goes closed source if they are tired of giving away an asset and they want the revenue and data flow to train new models

- Is this showing up in web2 AI lab revenue yet? No. Revenue is off the charts. Anthropic went from 9B to 47B run rate in five months

- So go forward, what happens?

- I think revenue slowly starts leaking to the open source inference providers (see Venice usage, OpenRouter's $113M raise, Baseten is raising at $11B or triple its valuation in three months, on revenue that went from $200M to $600M annualized in a single quarter)

- It doesnt move overnight, but it caps the labs ability to raise prices, and margins are already deeply negative. OpenAI is reportedly running near negative 122%

- With margins that bad there is no cash flow, so the labs are fully dependent on outside capital to buy GPUs, train models, and keep subsidizing usage (I.e. see Google tapping $80b equity sale, granted 30b for employee RSU taxes. Clearly they think Equity is overvalued or you wouldn't sell it)

- The break comes when that capital stops. Pricing is capped so margins cant improve, and the moment investors lose conviction on payback, the whole flow reverses

- Why would they lose conviction on payback? Back to the start - the inability to improve margins or get businesses to pay more

- This is also limiting, if we start making new drugs with AI or create entirely new businesses, you better believe people will pay up to the max for AI usage

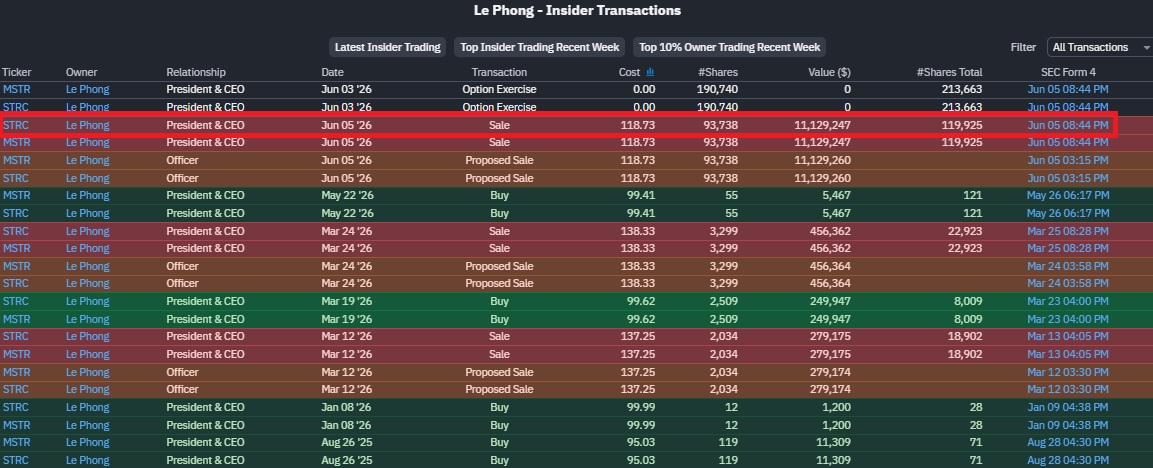

STRC is at $95.20 right now. That matters, and here’s why.

This is the security Saylor sells as stable, trades near $100. But it doesn’t sit near $100 by magic. $95.20 is right down in the zone where, by their own framework, management says they’d recommend cranking the dividend back up to drag the price toward par again.

So let’s talk about that mechanism, because anyone holding this stuff really needs to understand it. It’s called “the ratchet.”

When STRC slips below par, the only real lever they’ve got is the dividend. Fatten the yield, pull buyers back in, nudge the price back toward $100. Sounds clever. Here’s the problem. Every crank is basically permanent. You can’t quietly un-raise a dividend, because the price will drop, and you’re back at square one. So the annual cash bill just keeps climbing. And it’s already been hiked seven times since launch. 9% all the way to 11.5%.

Now ask where the cash for that growing bill comes from. They don’t make money from operations. So it comes from one of two places: issuing more stock, or selling Bitcoin.

See the trap? Price falls, they hike the dividend to defend par, the bill grows, bigger bill means more pressure to issue or sell. In a real downturn that’s not a flywheel. It’s a whirlpool.

And now watch the words, because this is where it gets Orwellian. Saylor used to say “I’ll never sell Bitcoin.” Full stop. Now it’s “I’ll never be a net seller.” Spot the move?

Net seller means he can absolutely sell. He just has to buy more than he sells, BUT AND HERE IS THE IMPORTANT BIT, Oney whatever period he decides to measure, which could be over the last 5 years, or the next twenty.

So the promise already got quietly reworded once to fit what they’re actually doing. The question is simple: does he hold even this watered-down version? Or do we get the next rewrite, where “net seller” becomes some fresh phrase that conveniently fits whatever the structure forces on them that month? We’ve seen this film before. The words keep changing to match the situation.

And here’s the kicker. Even the dividend hike isn’t a promise. It’s a “framework” where management says they’ll recommend a raise, subject to the board, and they can suspend or change it whenever they want. Saylor said it himself about the $100 peg: no legal obligation under the security, it’s just the company’s “number one business objective.” An objective. Not a guarantee.

Look, if you’re going to put money you worked hard for into these perpetual preferreds, at least understand what you’re actually holding. I wrote a full 78-page report breaking down the real risks of these things in proper detail. It’s linked in the first comment below. Read it before you buy, not after. Read the full length report. These are your savings, money you worked hard for.

Sam Altman, Dario Amodei, Demis Hassabis and many others have signed a letter urging Congress to increase security on orders of synthetic nucleic acids - and the equipment needed to make them - as models continue to become increasingly bio-capable.

BREAKING: The US technology sector has rallied +42% over the last 2 months, the largest 2-month gain in 24 years.

This also marks the 2nd-strongest rally this century, surpassing even the +40% gain seen during the 2000 Dot-Com Bubble.

The surge has been largely fueled by chip stocks, with the Semiconductor Index, $SOX, rising +66% over the same period.

By comparison, the S&P 500 is up +16% while the Dow is up +10% over the same time period.

Meanwhile, the S&P 500 is up +20% since the March 30th low, with the top 10 stocks contributing ~65% of the index's gains.

Half of the top 10 contributors were semiconductor stocks.

The AI trade is hotter than ever.

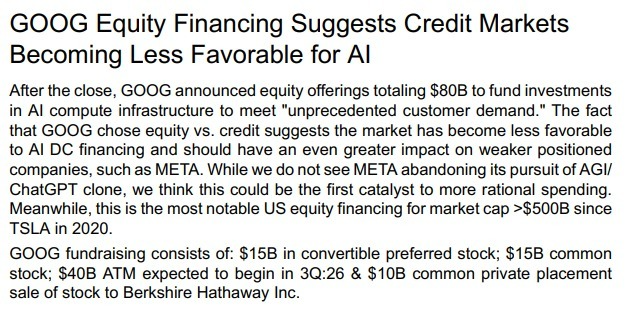

Oppenheimer brings out an interesting point here. If $GOOGL that prints massive FCF is tapping equity markets for $80B it's because credit is drying up. The private credit canary in the coal mine just died. The fact that their raise includes a massive $40B ATM and a $10B private placement to Berkshire Hathaway shows exactly how desperate the hunt for liquidity is becoming.

So who else is very exposed to the credit markets? $ORCL would be the first to come in mind, right? Name has rallied a ton here and suddenly looks like all the financing issues they have are forgotten. Their debt to equity is still over 5x.

$META is relentless in irrational spending. This might force Zucc to reevaluate his options here? Upgraded by Arete today btw.

Who needs to borrow a ton to keep the lights on? $EQIX and $DLR come to mind, 200MW datacenter costs 8 billion, certainly a hefty amount. But the biggest one of them all is none other than $CRWV, that rallied on $DELL yesterday, yet carries $21B of debt, including $8.5B delayed-draw term loan backed by GPUs.

Our understanding of $NAT deepens our understanding of Bitcoin - and vice versa.

$NAT is the only token in crypto that contributes not just monetary value to Bitcoin, but emotional value too.

Nothing like this has ever existed before.

I just joined the Kalshi Perpetuals waitlist. Perpetuals are finally coming to the USA. Sign up for Kalshi with my referral link for $25 to trade on Predictions https://t.co/uufdCOyzfS

BREAKING: The proposed US-Iran peace deal includes a $300 billion reconstruction fund for Iran, per NYT.

The program is being called an international "investment fund," which the US would facilitate in the final deal.

This comes as Iran demands "reparations" to end the war.