This is bigger than a $60B headline. If SpaceX moves forward with Cursor, it signals a deeper shift toward owning the full Al-driven development stack.

SpaceX said it has an agreement giving it the right to acquire artificial intelligence startup Cursor for $60 billion later this year or to pay $10 billion for the companies’ work together, part of the Elon Musk-run firm’s efforts to catch up with rivals in AI coding tools.

Bloomberg’s Natasha Mascarenhas has more https://t.co/xOcgVku6RE

Warren Buffett: "I sold [Apple] too soon. But I bought it even sooner, so it worked out. I think we've made over $100 billion in that pre-tax."

"I don't have any ability to predict what stocks will do next week or next month."

"Apple is still our largest single investment."

Warren Buffett spent three years quietly selling everything while the rest of Wall Street was throwing a party.

Between 2022 and 2024, Berkshire Hathaway sold a net $172 billion in stocks while buying almost nothing in return.

In 2024 alone, he offloaded $134 billion in equities, a pace of selling so fast that most investors did not even notice it was happening.

He sat through a bull market, watched stocks climb to the moon, and kept stacking cash anyway.

The result is $373.3 billion sitting in Treasury bills right now, the largest corporate cash hoard in the history of American business.

That number is not a mistake or fear, it is a loaded weapon waiting for the right moment to fire.

His own market valuation signal, the Buffett Indicator, is now sitting at 220 percent, a level that has only been higher during the dot-com bubble of 1999.

The Shiller CAPE ratio, another valuation measure, recently hit 39.42, which is the second-highest reading ever recorded outside of that same dot-com era.

Buffett has previously said that when the indicator crosses 200 percent, it is like playing with fire.

Now he has confirmed it publicly in an interview, when a big market decline comes, Berkshire will deploy, and they will deploy because businesses become attractive, not because someone told him the bottom is in.

He is not guessing at timing, he is simply waiting until the math works in his favor again.

When Berkshire had just $31 billion in cash going into 2008, Buffett turned that crisis into over $16 billion in pure profit through deals with Goldman Sachs, Bank of America, and General Electric.

Today he has $373 billion, twelve times that firepower sitting ready while recession warnings are louder than they have been in years.

Goldman Sachs and Capital Economics have both warned that the S&P 500 could face a double-digit decline if earnings disappoint or economic conditions weaken further.

Berkshire has already outperformed the market by 23 percentage points in 2026 alone, simply by doing nothing while everyone else lost money.

Meanwhile, that $373 billion in Treasury bills is generating roughly $13 billion in risk-free interest every single year while Buffett waits.

He is being paid billions to be patient, and the patience itself is the strategy.

Apple is still his largest single equity holding roughly 19 percent of the entire portfolio and he called it publicly better than any business Berkshire owns outright.

He admitted he sold Apple too soon but made over $100 billion pre-tax on the trade anyway, which is the kind of mistake most people spend a lifetime dreaming about.

The new CEO Greg Abel has described the cash pile as a "strategic asset" that allows Berkshire to act decisively when others are fearful which is the clearest signal yet that a major move is coming.

When Berkshire finally pulls the trigger, it will not be a cautious nibble, it will be one of the largest single capital deployments in the history of financial markets.

The only thing left to figure out is what price breaks him off the sideline.

Based on every signal he has sent over the last three years, that price is getting closer.

As a shariah compliant investor myself, one of my main concerns has been calculating the Zakat and Dividend Purification amount every year in accordance with my shariah obligations.

I couldn't find something that worked for me, so I decided to create it myself at SmartPSX 😄

Ken Hersh built a $20B PE firm with this rule:

would I trust this person with my kids?

if yes: write the check and make them invest their own money

$37M into Energy Transfer became $1.3B

one of the best PE books I've read

SpaceX just acquired xAI in a deal valuing the combined entity at $1.25 trillion.

Elon says it's about building "data centers in space."

But let me translate what's really happening here...

xAI is burning through $1 billion per month.

The company generated $107 million in revenue last quarter while hemorrhaging $1.46 billion in losses. It burned nearly $8 billion in cash through the first nine months of 2025.

That's not a business.

SpaceX meanwhile generated $8 billion in profit on $15-16 billion of revenue last year. It's the ONLY Musk company that actually prints money.

So what do you do when your AI startup is drowning in red ink ahead of your mega-IPO?

You fold the cash-burner into the entity that can still raise absurd amounts of capital.

And we've literally seen this exact thing before:

In 2016, Tesla acquired SolarCity for $2.6 billion.

SolarCity was bleeding cash, drowning in debt, and trading near all-time lows.

Tesla - the only Musk company at the time that could access the capital markets - absorbed it.

Wall Street analysts called it a "bailout dressed as synergy." Tesla's stock dropped 10% on the announcement.

The SpaceX/xAI deal is the same playbook.

Musk's stated rationale - that AI compute will be cheaper in space within 2-3 years - is the kind of thing that sounds visionary until you think about it for 5 seconds...

SpaceX builds rockets. xAI trains large language models.

These are wildly different businesses with zero operational overlap.

Imagine Microsoft acquiring a cement and steel conglomerate and claiming "tilt-up concrete slabs are essential for data centers."

That's the level of logic we're working with here.

The real play is simple: prop up xAI's insane burn rate with SpaceX's funding access ahead of what could be the largest IPO in history.

And xAI isn't alone in this capital-devouring spiral.

The entire AI sector has become a web of companies cross-subsidizing each other's losses.

OpenAI squeezes billions from Microsoft. Nvidia invests billions in xAI while selling them chips.

Everyone's propping everyone else up.

The investment thesis across the industry has devolved into:

"Please keep the Ponzi spinning long enough for someone else to be left holding the bag."

Meanwhile, the end product - AI - delivers marginal productivity gains for trillions in capex, soaring power costs, and balance sheet carnage.

If these services were priced to reflect their true economic cost, most users would find negative value.

But investors stopped reading balance sheets and cash flows long ago.

The AI models probably can't read them either.

What a time to be invested.

So what's the play?

AVOID the AI infrastructure complex.

When everyone's propping everyone else up, you don't want to be holding the bag when the music stops.

Look instead at sectors that have suffered from years of underinvestment: energy and commodities.

While trillions have been funneled into AI infrastructure, capital spending in oil, gas, and metals has been starved.

That's how cycles work - underinvestment leads to supply constraints, which leads to rising returns on capital.

Tech has the opposite problem. Overinvestment is destroying returns.

When you're burning $1 billion a month to generate $107 million in revenue, that's not a business model - it's a wealth transfer from investors to chip manufacturers.

Emerging markets are also attractive here.

They've been ignored while capital chased the Mag 7, and valuations reflect that neglect.

The Mag 7 now represent roughly a third of the S&P 500.

When this unravels - and it will - capital will rotate into the parts of the market where returns on capital are rising, not collapsing.

Energy. Commodities. Emerging markets.

POSITION ACCORDINGLY

@StockCompounder I certainly believe FFC should be valued on basis of consolidated account basis not on unconsolidated basis. On consolidated basis company result are weaker than comparative year

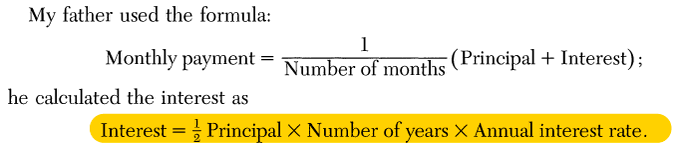

Years ago when my wife and I we were planning to buy a home, my dad stunned me with a quick mental calculation of loan payments.

I asked him how -he said he'd learned the strange formula for compound interest from his father, who was a merchant born in 19th century Iran

1/4

5 minutes of Charlie Munger’s wisdom on investing & life, in his trademark colorful style:

“What I needed to get ahead was to compete against idiots. Luckily, there’s a large supply.”