On March 3, 2026, For the first time in its history, $BX - Blackstone Private Credit Fund, the flagship of the largest alternative asset manager on Earth, just lost more money to redemptions than it raised in new capital.

What happens when $1.7 trillion in opaque credit meets human psychology and a trapped Fed?

8 funds. 4 sponsors. 1 pattern. The other shoe is dropping - you might not hear it yet, but you will.

New Post: https://t.co/lWEjX3UE5E

Asset management was the sector of the month. 4 separate research teams independently targeted firms in the space, averaging -24.7%.

The thesis across all of them: capital is leaving, and these business models weren't built for that. @CitronResearch , @AbelianAnalysis , @NingiResearch , and @CulperResearch all had receipts.

New post: "Paper, Silicon, and Crude"

Four days ago we mapped the AI supply chain from Microsoft to TSMC. Today, two links in that chain are under pressure.

Hormuz is closed. Oil is spiking. If it lasts, the inflation transmission hits CoreWeave's interest coverage directly.

Full analysis: https://t.co/ImHMhQDvli

#Iran #OilPrices #CoreWeave

The PLA Daily — the official mouthpiece of the Chinese military — ran three things on the SAME front page, March 1:

"Ten pots, nine lids" (十口锅九个盖) cartoon commentary — explicitly arguing that the US cannot cover all its commitments simultaneously. This is a capacity-constraint argument with obvious Pacific implications.

PLA Southern Theater Command combat readiness patrols at Scarborough Shoal — announced on the same editorial cycle as the Iran coverage.

Counter to Philippines-led "joint patrols" with extra-regional countries in the South China Sea.

These three items appearing together is not an accident. Chinese state media is editorialized with extreme precision. The message structure is: America is overextended → we are patrolling our claims → external powers trying to meddle in our waters can be countered.

The AI buildout is the largest capex cycle in history, but the financial scaffolding is built on a "time arbitrage" that’s starting to slip. ⏳

$CRWV is running out of time. With a 182-day DSO and $2M/day in idle interest, the clock is ticking.

Full report 📉: https://t.co/LFTABSNmnn

#ShortSelling #AI #CoreWeave

$JOBY Earnings call - key takeaways:

1. Nonlinear completion is the core risk The easy 60% of certification within existing regs goes fast. The hard 40% outside existing regs is where programs stall and burn cash. Joby is entering the hard phase.

2. The regulator is behind the applicant. FAA at 73% vs Joby at 80% means the bottleneck is the FAA, not Joby. You can't certify faster than the regulator can review.

3. The framework is still being built. The FAA's own roadmap shows airworthiness convergence work running through January 2027. Joby is seeking certification under rules that are still being finalized.

4. International expansion is years away. Every international market Joby has announced requires bilateral agreements or separate validation processes that don't exist for eVTOL. The bilateral agreement timeline runs through at least mid-2027.

5. Cash burn clock. $2.6B in liquidity, zero revenue, 2 aircraft/month production rate. Every quarter of certification delay is cash burned with nothing to show for it.

6. Pre-revenue company priced on hope. The entire investment thesis depends on certification timing that the FAA's own documents suggest is more uncertain than Joby's shareholder letter implies.

Toyota has spent decades and billions on hydrogen fuel cell technology — the Mirai passenger car, the Kenworth semi-truck partnership, heavy investment in hydrogen production infrastructure. They genuinely believe hydrogen will be a major energy carrier in a decarbonized economy and they've been willing to look wrong about the timeline for a long time. Joby's fuel cell IP is legitimately interesting to a company with that strategic orientation. They may care more about the patents and the engineering talent than about whether air taxis ever become a consumer product.

$JOBY is attempting something that has never been done: build a commercially viable, hydrogen fuel cell-powered eVTOL aircraft, certify it under regulatory frameworks that do not yet exist, and bring it to market before the company’s cash runway expires. We are short JOBY.

- Read my full thesis here:

https://t.co/bYOeE3AAVT

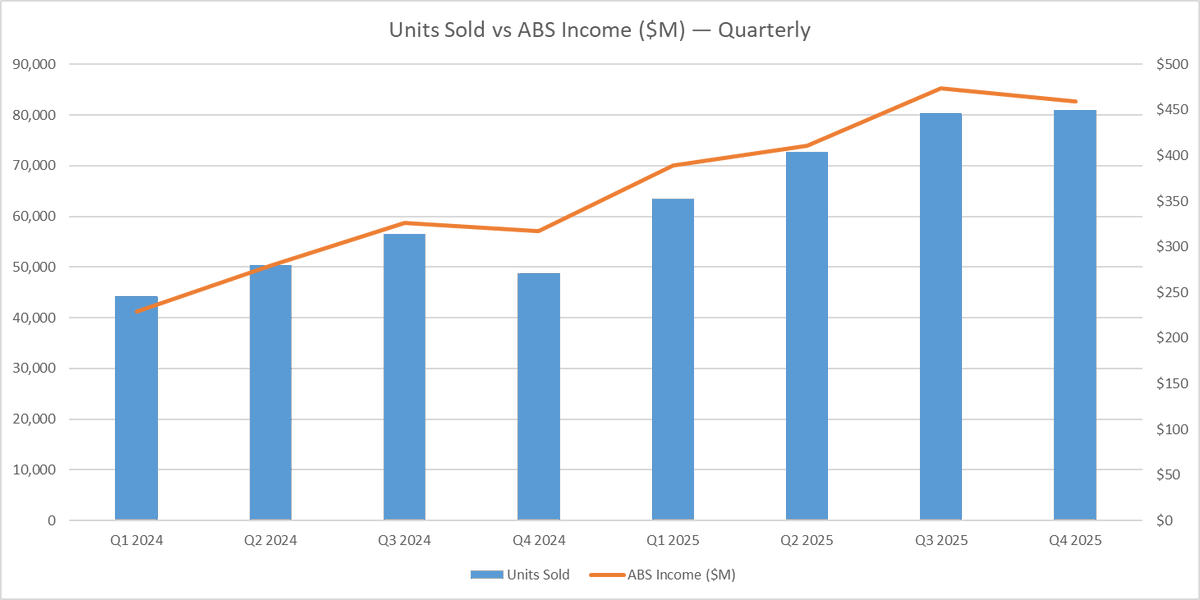

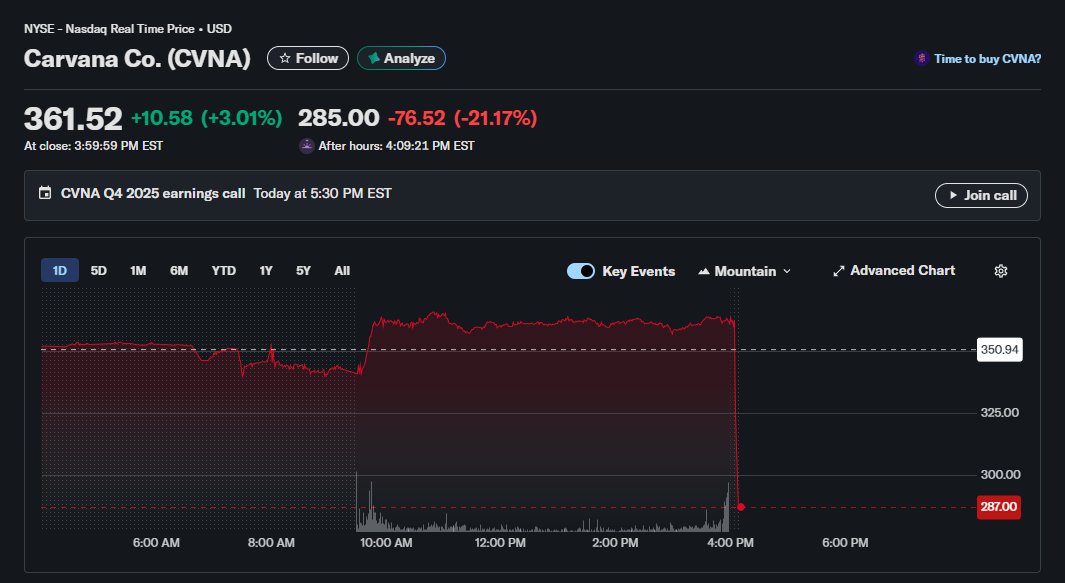

$CVNA's Flywheel is beginning to seize. Even with increased unit sales profits on ABS securities are down. This is a clear break in what has been an otherwise tight correlation for the last 2 years.

"Stage 4: Flywheel seizure. If Carvana cannot securitize, it cannot originate. If it cannot originate, it cannot sell cars on credit. If it cannot sell cars on credit, revenue collapses. The 10,000% rally unwinds.

This isn’t a hypothetical sequence. It’s the exact chain of events that has played out in every securitization-dependent lender that experienced a credit deterioration cycle. The only question is timing." - https://t.co/oXgCP973wS

I think this is the real number to pay attention to.

The bull case for Carvana has always been that they're not just a used car dealer — they're a finance company that makes money on the spread from originating loans, selling GAP/VSC products, and securitizing the paper through ABS. That ancillary revenue is supposed to scale with units.

But this ratio is saying the opposite: as Carvana pushes harder on volume (units up 46% YoY), the finance engine isn't keeping pace. They're either:

Originating lower-quality/lower-margin loans to hit volume targets

Getting tighter ABS spreads in the securitization market

Attaching fewer finance products per car as they move into price-sensitive segments

Correction on Carvana analysis: LTV charts in original report showed "loanValueAtReportingDate" (amortized balance) not "originalLoanValue." Re-ran analysis with correct field.

Finding: ~30% of loans were underwater at origination across ALL vintages, not just recent ones. There is a noticeable drop in 2022, but we think this is most likely attributed to a boom in used car prices, not more conservative underwriting habits.

This doesn't change core thesis (stated income, FICO engineering, trigger management all stand), but the "deterioration narrative" on LTV was wrong.

Updated charts + full methodology correction posted here https://t.co/Ruxb3eDawR