Notice all those "The State of [insert a tech vendor's thing]" studies going around? I wrote a CTO's guide to them and released a database of 250 studies on building a business with software, AI adoption, security, developers, and more. https://t.co/JqBABq5zh3

@eastdakota I understood folks wanting to get some more transparency and to get Vail to take some more responsibility for parking a few years ago, but doing it at the expense of the visitor experience turned crazy.

Spent the last few weeks pulling together our thoughts on the state of the software and ai market ahead of our annual meeting yesterday. Obviously a dynamic time with a lot going on so tried to unpack what is happening and our view on the different levels of risk and opportunities.

Thank you to my colleagues @AdilBhatia and @lydianday for the hard work on this with me.

Something I don't hear discussed enough - how Microsoft pointlessly screwed over OpenAI and handed the enterprise market to Anthropic.

Microsoft is a big investor in OpenAI and decided to make their models exclusive to Azure Cloud. This turned out perfectly for Anthropic, but not for OpenAI and maybe not for Microsoft either.

Back in c.2023/4, OpenAI was not only leading in consumer but the enterprise too - it was first to introduce things like JSON response format and Structured Outputs, Batch Mode and a bunch of other features - all ahead of Anthropic. And it wasn't clear that Anthropic's models were any better at that point.

So how did Anthropic gain share? Back then it wasn't Claude Code or Cursor, but it as the simple fact that if you are on AWS (c.35% of market), Claude models were by far the best models you could access. Remember, OpenAI wasn't allowed to be on AWS.

AWS customers could go to OpenAI directly and some did, but don't underestimate the amount of effort this takes for large companies. I was working in a large legacy business at the time and it took us c.4 months and about $500k to just get access to OpenAI at the time, being an AWS customer. And this was considered a highly successful project. Most will just not bother.

Perhaps back in 2023, exclusivity was useful - OpenAI was basically the only game in town and some could theoretically switch to Azure. But now, what's the theory for keeping OpenAI exclusive to Azure?

If you are an AWS or GCP customer (half the market), the easiest thing you can do is to just go use the API that is available in your cloud, which still cannot be OpenAI. I can't imagine a situation where a meaningful AWS customer would switch clouds to Azure to only use OpenAI models.

And what for? Ok, Azure gained a couple of points in market share, maybe some of it was because of OpenAI exclusivity back in the day. Now, OpenAI is frantically re-writing their relationship with Microsoft and it might leave Microsoft with no IP in the future.

Even mathematically, I would bet higher OpenAI growth would have generated more value for Microsoft through their ownership of OpenAI rather than getting Azure a little bit of an advantage 3 years ago.

I hope Dario will buy Satya a beer.

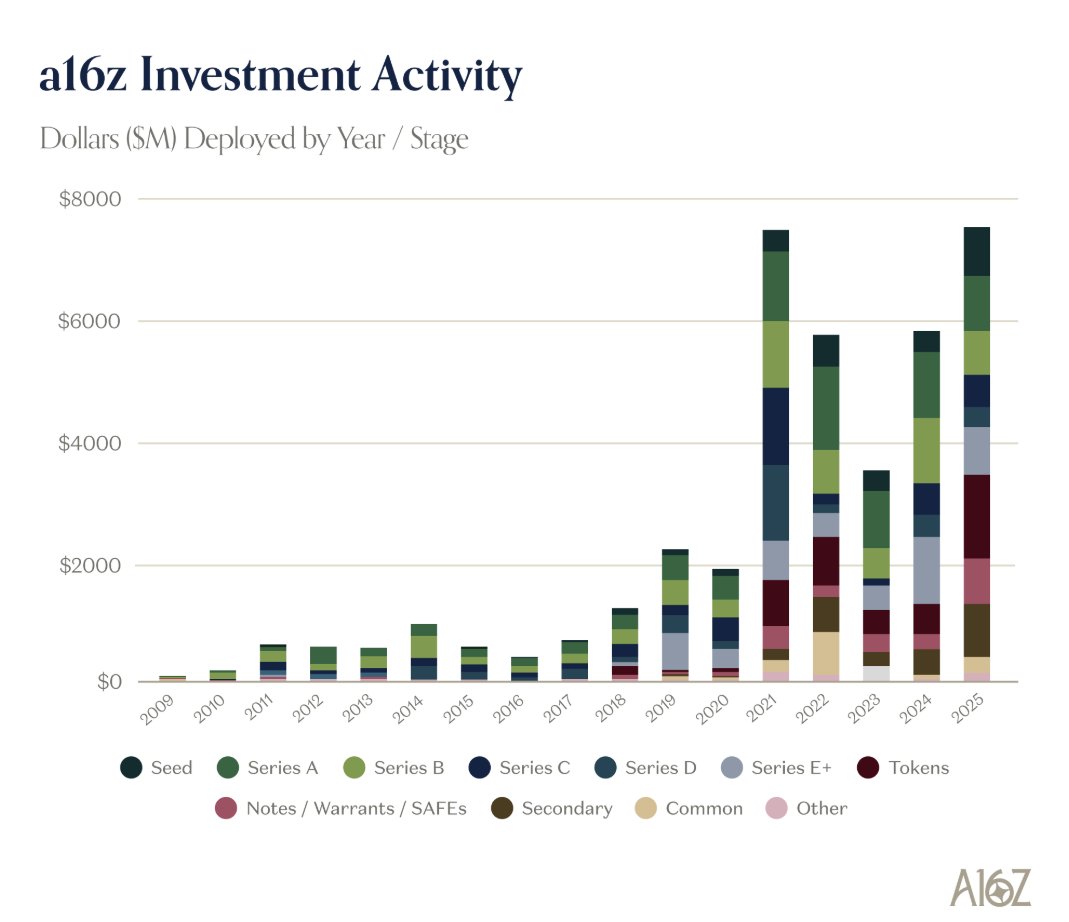

Really interesting chart from a16z's latest State of Markets report:

- a16z deployed $1.5B into crypto tokens in 2025. This looks to be majority of their increase in capital deployed between 2024 and 2025.

- Also looks like a big jump in SAFE's. If we assume its all pre-Series A rounds, looks like a 5-6x increase in capital deployed into Seed.

- Basically every category except Tokens, Seed, and Secondaries is flat or down between 2024 and 2025.

- a16z bought ~$750M in Secondaries in 2022, $1B in Secondaries in 2025.

- I would assume 2022's ~$750M in Common is Secondaries too, but they specifically call these two out. Wonder what exactly this is, maybe partly the $350M Flow round? Maybe some weird structured rounds?

- a16z practically exited the Series C/D market in 2022 and 2023. Looks like dollars deployed down 95%+, from ~$3B in 2021 to maybe ~$100M in 2023. They also pulled back slightly in 2025 after a bigger 2024 (was about 66% as large as 2021).

- There's an unlabeled gray bar of ~$200m in 2023. Might just be uncolored Common/Other? Pls fix.

Founders say “we’ve got PMF.”

But do you have:

• Offer-audience fit?

• Channel-message fit?

• Delivery-expectation fit?

If any one’s off, scale breaks.

@EvanKirstel Kinda, after you increase the existing scare supply of a material by 1000x+ it's no longer worth a trillion. See Debeers and synthetic diamonds for more details.

Goldman: "We don’t think the AI investment boom is too big. At just under 1% of GDP, the level of spending remains well below the 2-5% peaks of past general purpose technology buildouts so far."

Oracle announced a third network architecture today. At first glance, it's a modern Juniper QFabric developed with Arista. Kinda neat to see that architecture come back. $ORCL $ANET

https://t.co/xLw4hWyKiw

"Quantum systems cannot be networked...The reality is Quantum computing is narrow, domain-specific breakthroughs with [an] extremely limited TAM." From @DeepSailCapital.

https://t.co/5s94bb25tJ

Personal Takeaways from Yotta and the AI Infrastructure Summit:

-The Infrastructure Arms Race & Time-to-Power Premium: Every fundraising and revenue dollar is flowing directly to compute infrastructure, creating a GPU/HPC arms race. Time-to-power now dominates all site selection criteria with significant pricing power as demand appears insatiable for the next 1-2 years, though more uncertain beyond that. Revenue lost waiting for grid connections exceeds premiums for faster alternatives, but this depends on AI clouds/labs eventually generating sustainable profits.

-Neoclouds vs. Traditional Players - Speed as Competitive Advantage: Neoclouds and crypto-to-HPC players' main edge is faster deployment, standing up sites in months vs. years for traditional players through existing interconnect and strong field ops. This isn't just premium hardware rental on fast-depreciating assets. Traditional hyperscale clouds are seeing 75-90%+ margins on GPU compute (historically unprecedented) due to chip/power scarcity so they are excited about faster deployment timelines. Behind-the-meter power is a huge focus with 6-72 month generator acceptance as primary power while grid connections complete.

-Rapid Tech Evolution & Infrastructure Flexibility: Rack density evolved from ~10kW years ago to ~130kW now, accelerating toward 1MW racks. Everyone is designing for uncertain future requirements given fast-moving electrical/cooling equipment development. IT refresh cycles shortened to 5-7 years with multi-vendor strategies to reduce supply chain risk. Interesting split on workload flexibility. I heard "up to 70% of workloads can be interruptible" and some newer thinking that training/inference can co-locate and some workloads may focus on both simultaneously (vs. an either or thinking that has been prevalent in the market). That also introduces some optimism on the ability to repurpose infra should training/inference needs change in the future.

-Capital & Labor Constraints: Given the scale (~20% of hyperscaler revenue, ~60% of operating cash flow on aggregate), seeing: JVs bridging financing gaps, PE flooding every ecosystem touchpoint, and capital recycling from existing infrastructure becoming standard. Labor is constrained across the entire value chain: electrical technicians, HVAC/mechanical specialists, construction craft labor, and data center operations staff for complex AI workloads.

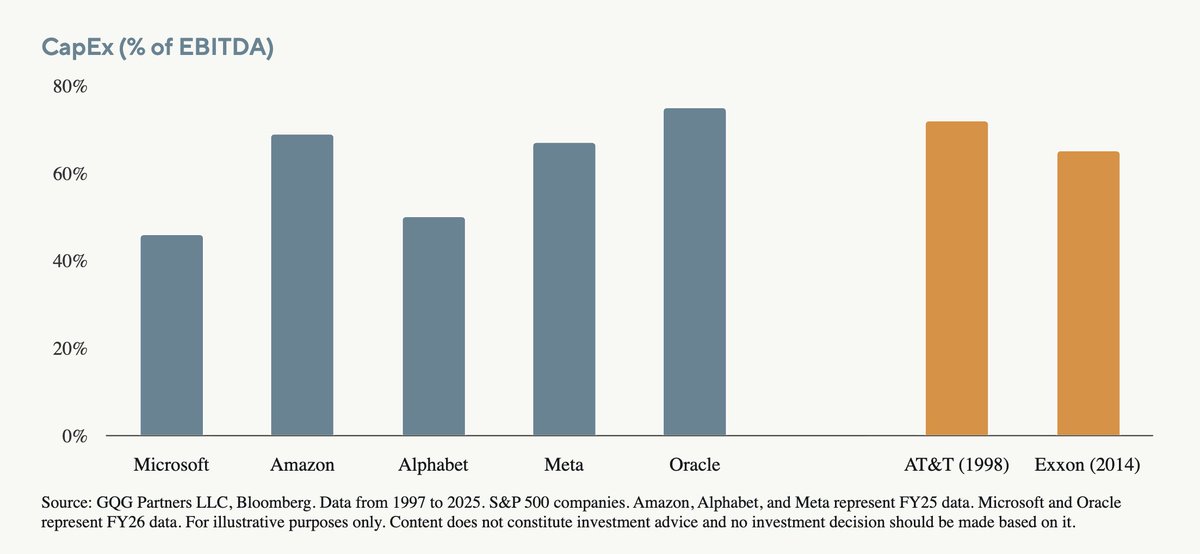

"Big tech CapEx as percentage of EBITDA is now running at 50%-70%, which is similar to AT&T’s 72% at the peak of the 2000 telecom bubble and Exxon’s 65% at the peak of the 2014 energy bubble.

Historically, companies experiencing higher capital intensity tend to be structurally poor investments.

In other words, AI CapEx has already caught up to prior bubble levels, even after adjusting for big tech’s initial high margins."

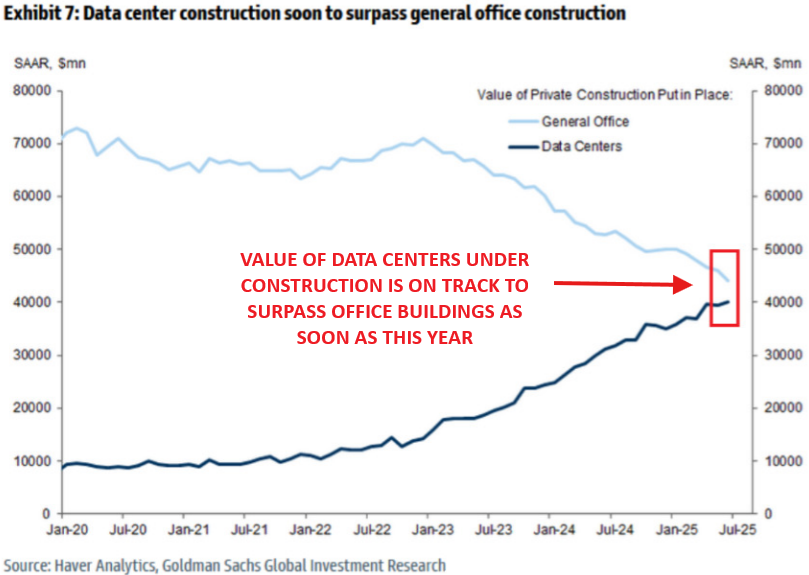

This is absolutely insane:

There are now $40 BILLION worth of US data centers under construction, up +400% since 2022.

For the first time in history, the value of US data centers under construction will soon EXCEED office buildings.

This is a historic shift.

(a thread)

![EricJhonsa's tweet photo. "Quantum systems cannot be networked...The reality is Quantum computing is narrow, domain-specific breakthroughs with [an] extremely limited TAM." From @DeepSailCapital.

https://t.co/5s94bb25tJ https://t.co/VNqWzfGK4a](https://pbs.twimg.com/media/G2NMrXtbwAA9nzm.jpg)