THE WRONG TRADING MINDSET

I keep saying to my subs that trading is a game of probabilities not a game of predictions☝️

#market rarely can be predicted with significant probability in order to provide edge.

But the ads, the furus, trading services teach retails the wrong mindset of sweating to predict every next moves.

And this results in the common behavior that retails trying to hit the lottery ticket and following different furus, they keep oversizing their bets on the next #market move.

Meanwhile the furus are fighting with eachother over the best hit rate.

...this is all very very very wrong...

And the reason is the general undereducation of the people in mathematics...

As somebody who consistently built a significant wealth before turned 30, and worked for firms, I tell you the very simple basis, what I mean... Listen...☝️

Since Kolgomorov, we have a very nice definition of probability that says that the relative frequency of an event converges to its true probability value over infinite trials.

This means, that the probability value gives us a value that says how many times the event will happen over 100, 1000, 100,000 etc. trials.

An event with 70% probability happens 70 times over 100 trials, and 700 times over 1000 trials, and so on.

The meaning of this is that the true edge emerges over even larger number of trades.

From this point, you can know that hit rate doesn't really matter, but the true edge lies in position sizing and consistent and conscious risk management.

If I have a win rate of 75%, I consequently have a loss-rate of 25%

Let's say, I am a typical retail, who is impatiently starve to hit that one lottery ticket, and I win only $100, but loss $400

This means I win 75*$100 but lose 25*$400 over one hundred trades, so I will end up with an expected value of -25, meaning I'm expected to lose $25 in average on each trades over the long run.

Or lets say, I win $150 and lose only $200 (so only a 33% more $ loss than win).

So my expected value will be 0.75*150 - 0.25*200 = $62.5 win on each trade in average.

Not too profitable right? Despite the 75% win rate😉

The key is the wrong sizing.

Now flip the coin, and let's say I'm right 25% of times, and wrong 75% of times, but my sizing is logoptimalized, kelly-based, stop-losses and limit sell-orders are consistent, and my approach is very patient...

Let's say I win $200 25% of the times, and lose $50 dollar 75% of times.

0.25*200 - 0.75*50 = $12.5

So, as you can see with a relatively very bad hit rate, one can still win on the long-run if the sizing is consitent and conscious. The $12.5 is very small, but it can be increased when the trader sizes up on his wins through leverage etc. So the key is that you can get the same or even better EVs than in the previous example, with significantly worse hit rate☝️

This is the reason btw, why options selling strategy works better on the long run, than constantly being long #volatility.

The reason is that time is going forwards (long theta) and that #volatility is mean reverting (short vega).

Let's say you see a 25-delta option. This means, that approximately you have like 25% chance to win on this contract.

Let's say the premium it asks is $150

Now, you have a probability of 75% to win $150 and a probability of 25% to lose some portion if you short this contract.

(In theory, the max loss on a short option position is infinite, but this happens only to very dumb people, who forget to use stop-loss, and forget to read the chart of the underlying. So in reality you will lose less than $150)

But here is the thing...

I risk roughly $150 when taking that 25% risk. (I say "roughly" bcs you won't lose all the $150 due to stop-losses)

In probability theory this means, that over 100 trades I collect 75*150 = $11,250 and lose only 25 times $150 or less. While the option buyer, who risks $150 to win only 25% of times, are like a bad gambler in the eyes of the Wall Street and market makers, bcs time and #volatility works against the option buyer (if not the spot itself).

☝️🙂The key point that instead of thinking of #market and #trading like dependent events (which is not), keeping in mind Kolgomorov's definition-based probability theory when building strategies, will result in converging towards the expected win rate value over time.

The former results in an emotion-driven, conceptionless, erratic trading behavior with no longer-term edge, while the latter demands patience and self-control, but results in a consistent and less-volatile growth over the long-run.

This is how a succesfull trader thinks.

❗️There is no Holy Grail, Secret Sauce, or any secret Equation of Success formula/techinque to grow (contrary to what many furus promise for you out-there), but consistent and patient and conscious mindset and planning😉

(Not to mention, that to backtest an allegedly 70% hit rate, you need like 320 consistent sample at best, to differ variance from disprove of the strat... so be cautious of these self-claims. The key word here is "consistent", bcs #market can change requiring different strats)

☝️❗️Also keep in mind that bcs #market is not a deterministic system but a multidimensional stochastic system with billions of variables (each of them a also multidimensionals), every trading strategy performance necessarily fluctuates. Every one of them!

And not just that the standard deviation changed, but the skewness as well, depending on #market environments, so to forecast the negative variances of a strategy is very tough thing, and we only have rough approximations to do so.

And as the fluctuation also follows a random process, you can have the 40 losing trade at once in case of a 60% hit rate, meaning, you have a very high chance that you will blow your entire account.

This means, that there is a non-zero % chance that the losses eat up your whole account before your winning period kicks in.

This chance can be significantly reduced by taking smaller position sizes.

This is why, I keep recommending to use paper trading account first. I did the same, meanwhile I'm a mathematician, focused on gambling theory and stochastic systems during my years of study, and I was able to mathematically plan my trading consciously...

Still people keep refusing training on a paper trading account first, bcs they are greed, impatient and willing to win the lottery ticket now and here.

The thing is however, if you cannot succed with a paper account, you won't succeed with real money either, especially bcs on paper trading there is less emotion involved and it is easier to hold the consistency.

Paper trading gives 1) chance to educate your mind, prepare your psyche to trade in live account; 2) it gives you a chance to backtest, finetune your strategies bcs you have no additional stress.

And I didn't talked about the real annual returns, adjusting to #inflation... thats the hard thing to do...

and thats the very first thing every trader should learn: how to save your present money from inflation generating 0% real annual return. If you can do that with confidence, you can make the next step: generating 5%; 10%; 15% real annual portfolio return...

The conclusion is this:

No wealth was ever created through intraday trading☝️

Wealth can only be built on the long-run, and must be saved from inflationary pressures first☝️

In every field, only the patient and consistent win on the long-run. In the world of smartphones and screwed soc-media, it's etting more and more rare among people, but lets be smarter than the majority and play the long-term game.

Remember Cliff Young?😉

If you made it to this line here, thank you for listening. Now lets re-read the post, and take responsible actions. Make it alive in your life😘

#riskmanagement #tradingstrategy #optionstrading #stockmarket

Predictive Anylytic Models (PAM)

Robert P. Balan

Jun 5, 2025 5:42 PM CEST -- 2 hrs after NY open

Bullish, with early consolidation risks. June 5 0DTE likely to see SPX consolidate between 5950–6000, with a 40% chance of holding (MM support, call volume), a 25% chance of testing 5975–5950 (profit-taking, put volume), and a 35% chance of reaching 6025–6050 (bullish momentum). The bullish trend persists, but intraday dynamics and macro risks may introduce early consolidation risks

(Source: @ConvexValue App)

Stabilizing, Positive Forces

5950 Gamma Fortress - 40.79 GEX provides major downside support

Current Position Safety - 5976 positioned above key support clusters

Pin Risk Dynamics - 5975 maximum gamma (49.96 GEX) creating gravitational pull

Support Architecture - Multiple defensive levels below current price

(Python Matlibpro; Data Source: @ConvexValue App)

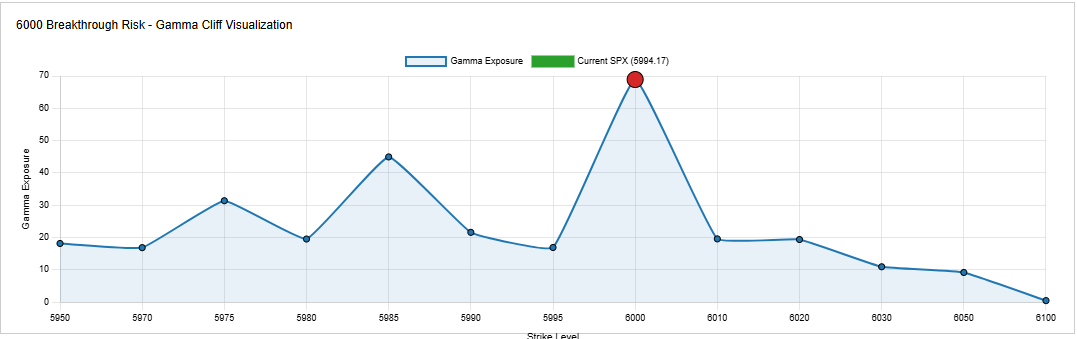

6000 Level Breach Impact -- Breakthrough Dynamics

MMs with massive short call exposure must hedge aggressively at breach of 6000. Every point above 6000 increases delta hedging requirements exponentially.

At breach of 6000, Market Makers will be AGGRESSIVELY BUYING futures to hedge their massive short call exposure.

Short Call Position: MMs sold 48,535 calls at 6000 strike

ITM Exposure: With SPX above 6000, these calls have positive delta

Delta Neutral Requirement: MMs must buy ES futures to offset short call delta

Exponential Effect: Each point higher increases delta (gamma effect)

(Python Matlibpro; Data Source: @ConvexValue App)

Market Maker Hedging Imperatives

Critical Exposures:

5980 Strike: Heavy call delta requiring aggressive selling if breached

6000 Level: Massive short call exposure demanding fortress defense

5975 Zone: Maximum gamma creating pin risk and hedging complexity

5950 Support: Put protection requiring buying pressure if threatened

(Python Matlibpro; Data Source: @ConvexValue App)

MM Hedging Action Map (visual above)

Stacked bars showing required MM actions:

Green bars: Buying pressure required (ITM calls + put support)

Purple bars: Pin risk complexity

Blue bars: Neutral monitoring zones; momentum acceleration zones

MM Delta Hedging Requirements by Strike

(6000): Massive +1,256 delta requiring aggressive buying

(5975): +1,022 delta pin risk zone

(5980): +393 delta from breached resistance

(5950): -271 delta support requiring buying if threatened

Tactical Stance:

Position for possible breach of 6000 in late, EOD, or overnight Asian/Europe trade