Zepto filed an updated prospectus for its IPO on Monday night, June 8, seeking to raise Rs 8,010 crore in fresh capital.

The company has gained share, but at a cost.

BoFa's theoretical NOV calculation puts

Blinkit at 52% market share, Zepto at 27%, and Instamart at 21%

🚨🚨Zepto has three quarters of cash left ahead of IPO

These figures help explain why the quick commerce player is pushing ahead with an IPO even as the listing environment has turned uneven.

Zepto: $311 mn

Swiggy: $1.32 bn

Eternal: $1.4 bn

Details: https://t.co/CkMDub8n3J

🚨Did SEBI just approve FDI in online retail?

First time seeing this structure out in the open… #Zepto

Even Blinkit waited for IOCC approval before recognizing NOV as revenue..

Maybe kosher from a legal standpoint, but definitely not in spirit

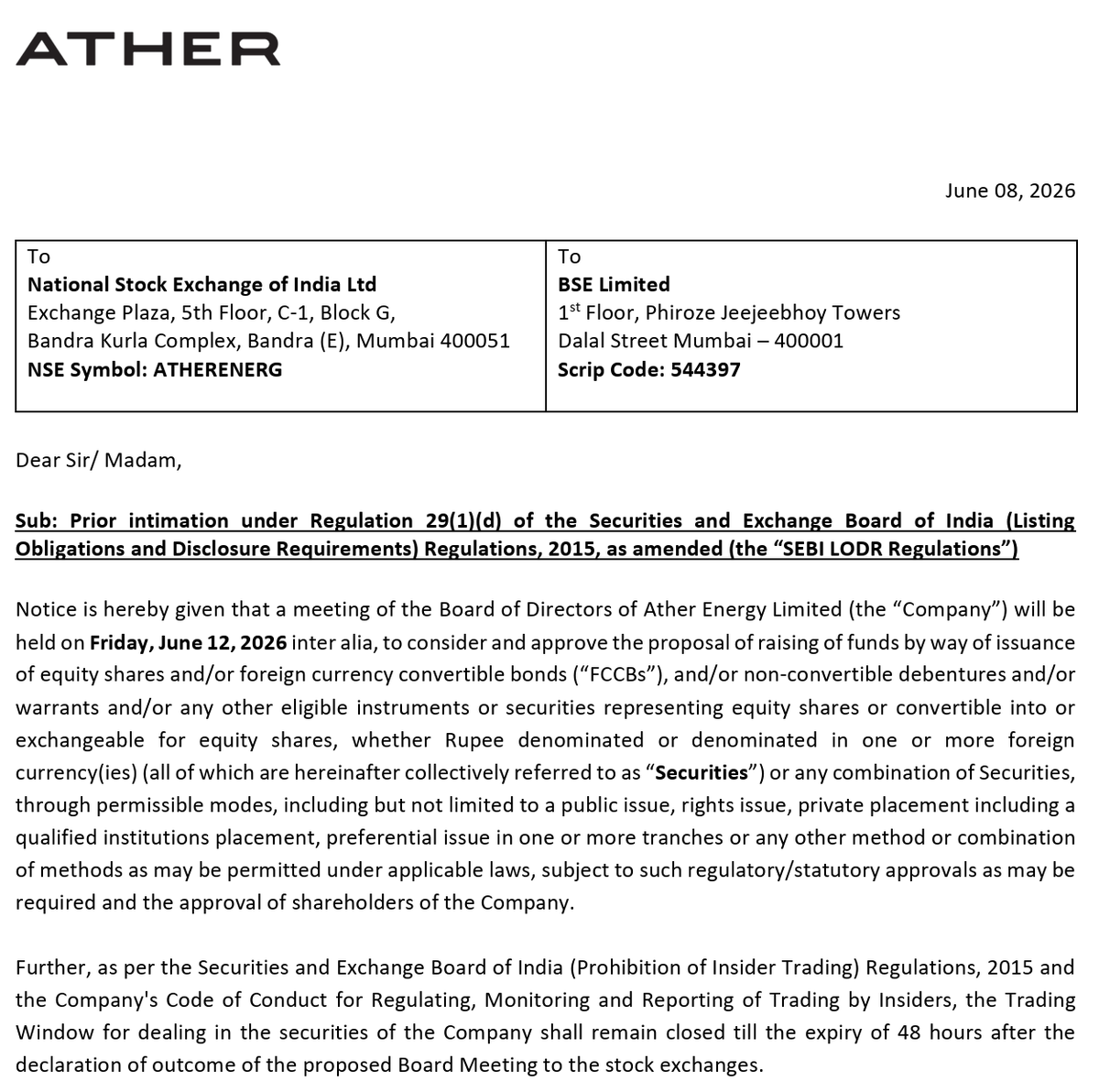

🚨 Ather Energy's board will meet on Friday to discuss a fresh capital raise.

This comes over a year after the IPO in which Ather raised Rs 2,626 crore in primary capital.

Since the IPO, Ather's share price has tripled, giving it a market cap of Rs 39,000 cr ($4.1 bn).

Zepto's implied valuation has fallen from about $7 billion to closer to $4 billion in grey-market discussions ahead of the IPO.

At 1x NOV run rate multiple, implied valuation is ~ $3.3 bn

🚨🚨 Zepto is asking investors to rethink how they evaluate quick commerce.

For years, the conversation around Blinkit and Swiggy Instamart has centred on:

• Basket sizes

• Margin progression

• Expansion

https://t.co/AlN4LpEmOM

Zepto is making a different argument.

Its prospectus says profitability comes from density, not bigger baskets or more cities. That's the heart of the IPO thesis.

The key question: Will density-driven efficiency win, or will higher basket sizes prove structurally superior?

The market will decide.

🚨🚨Amazon is aiming for the top spot in India’s quick-commerce market

Country manager Samir Kumar says he is “in this to win it”.

Despite arriving late, Amazon believes the market is still early enough for leadership positions to change.

So what does Amazon’s playbook actually look like on the ground?

📦 Prime customers

📊 Years of shopping data

🏭 Deep relationships with brands

🚚 A supply chain built over two decades

💰 The willingness to invest through losses

🚨 Amazon pioneered e-commerce globally, but local startups like Flipkart were often ahead when it came to building an India-specific playbook.

This included innovations such as cash on delivery (CoD), in-house logistics networks, and financing options like no-cost EMIs and debit card EMIs, many of which were popularised by Flipkart.

Amazon, however, has consistently proven to be a fast follower - quickly adapting successful ideas and scaling them aggressively.

A similar dynamic is now playing out in quick commerce, although it is still early days as Amazon gears up to challenge market leader Blinkit.

Amazon has reportedly committed more than $300 million to the business and has already opened 400–500 dark stores in key metros.

So why is quick commerce strategically important for Amazon? And what advantages, if any, does it have over Blinkit?

@AditiS90 has a detailed article

https://t.co/j9LFaruRtK

🚨 FirstClub, a quick commerce app focused on premium products, has raised $55 mn in funding from Peak XV and Sofina.

New round doubles the two-year-old startups' valuation to $255 mn, taking its total funding to $86 mn.

The startup has been founded by Flipkart veteran Ayyappan R.

🚨 Together Fund's Manav Garg is leaving his role at the venture firm to join vibe coding app Emergent Labs as its executive chairman.

Together led Emergent's seed funding round in September 2024. And now Emergent is in talks to close a round at Unicorn valuation.

Ola Electric has set a floor price of Rs 37.74 per share for its QIP.

That's 50% below the IPO price of Rs 76, less than two years ago.

Repaying debt - which stands at close to Rs 2,500 cr for Ola Electric - is the key priority.

Most of the debt is at over 11% interest pa 👇

We backed Navo because we believed the B2B fashion supply chain needed a digital-first reset. The execution has been phenomenal: 20x growth in just 10 months with ZERO feet-on-the-street, ZERO credit. 🚀

Navo is making trendy fashion trends accessible without lag to Bharat customers.

Proud to partner with @SuparnGoel anshul and the team. Great piece by The Arc covering this shift: @madhavchanchani@AditiS90

60-minute factory-to-retailer supply chains and video-powered dark stores.

That’s how a new crop of startups - Navo, Bijnis, and Zoop - are looking to bridge the supply chain gap for small fashion retailers in tier-2 and tier-3 towns.

Investors such as Peak XV and India Quotient have already placed early bets on this market.

Swiggy is in damage-control mode after shareholders rejected its proposal to give more board seats to the founders and management team last week.

The company said in an exchange filing last night that the proposed changes were not about “concentration of power”, but part of an effort to make Swiggy an Indian-owned and controlled entity (IOCC).

Swiggy added that board rights are not in perpetuity and were approved by its independent directors.

Co-founder and Group CEO Sriharsha Majety admitted in an interview with The Economic Times that the company could have “handled this better through engagement” and “communicated more effectively”.

Majety has also said he wants to put the proposal to a vote again and believes it will eventually pass.

Let’s understand Swiggy’s board structure right now.

- Sriharsha Majety is currently the only management representative on the board after co-founder Nandan Reddy stepped down earlier this year.

- Amsterdam-listed Prosus, which owns over 21% in Swiggy, now has two representatives on the board - India head Ashutosh Sharma and Renan Pinto (who joined last week).

- The board also has four independent directors, including chairman Anand Kripalu.

However, independent directors, even if they are Indian residents, are not counted toward Indian control norms.

This meant Swiggy needed at least three management representatives on the board to outweigh the two directors representing foreign investor Prosus.

Proxy advisory firms argued that board representation should be linked to shareholding. Majety and co-founder Phani Kishan Addepalli together own less than 5% of Swiggy.

Failure to become an Indian-controlled entity could delay Swiggy Instamart’s shift from a marketplace structure to an owned-inventory model similar to Blinkit.

The owned-inventory model has given market leader Blinkit several advantages.

By owning inventory directly, Blinkit captures the full retail spread, improving gross margins already by 3% and is expected to improve net margin by 1%.

Owning the goods also allows Blinkit to book the full value of sold items as revenue instead of earning only a marketplace commission.

It will be interesting to see how this impacts Swiggy’s profitability and break-even ambitions from now on.