For all who are complaining about the @SpaceX valuation for its IPO, it’s a free market. Don’t buy it.

For those who believe in future and @elonmusk , it’s a free market, buy it.

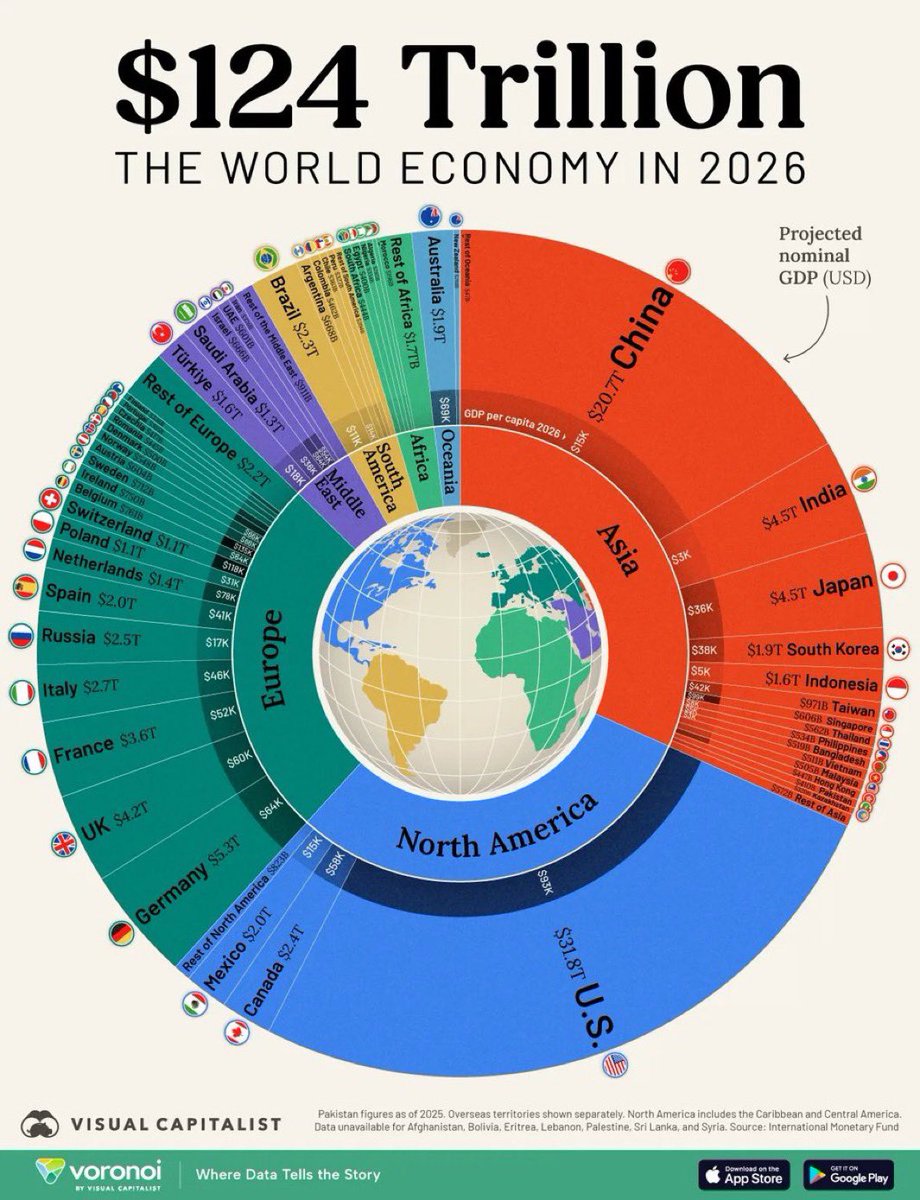

RT If you are going to invest

What you should be doing with your money at any age:

Birth - investing

10s - investing

20s - investing

30s - investing

40s - investing

50s - investing

60s - investing

70s - investing

80s - investing

90s - investing

Dead - investing

Exercising incentive stock options can trigger the Alternative Minimum Tax, often catching high earners off guard.

Here's how it works:

You might see a paper gain when exercising ISOs, but if you hold the shares, that gain is treated as income for AMT purposes. The regular tax system doesn't recognize this "income," but AMT does, and the liabilities can be significant, sometimes six figures.

To avoid a surprise bill:

- Plan to exercise ISOs over multiple years to spread out potential AMT exposure.

- Run detailed tax projections with your advisor before making any moves.

- Understand the timing rules: Disqualifying dispositions can change your tax treatment completely.

A proactive approach is the difference between strategic wealth building and an expensive oversight.

Bitcoin might be more popular if it was:

- Controlled by a small number of people.

- The most popular money for criminals.

- Printed at a rate of 7% per year.

- Easy to reverse transactions.

- Limited by banking hours.

But the dollar has a strong monopoly there.

@HermesLux@isabellasg3 Completely agree!! Got my bachelors and masters and health insurance taken care of. Learned skills and work ethic along the way as well.

The real edge?

Layer, stack, and time these accounts for max tax efficiency.

Don't let the IRS win by default.

Playing the account game well = bigger net worth, more options, less stress.

Many blow thousands in taxes, just because they don't know their account options.

Here's your 2026 playbook for every major retirement account (plus a few most never use):

Taxable Brokerage 💸

- No contribution limits, no RMDs

- Gains taxed at favorable rates

- Access funds anytime

- Example: For goals before 59½ or when you want pure flexibility.