You cannot grieve correctly until you know what is actually permanent and what is actually temporary.

Most of what we mourn is not what we think it is.

~ The Bhagavad Gita.

After almost 3 quarters of de-growth QSR industry started showing Earnings Growth.

- Post Result reading exercise starts.

Disc: Not a Buy/Sell Recommendations.

"i don't know what happened in hospital space this quarter" - no stress, we got you!

we read 17 listed hospital concalls (a few the prior quarter too) to know what's cooking on ground - at blindspot, we track this space closely.

what's inside?

- whose revenue grew the most and why, whose occupancy climbed, whose fell, and the real reason behind each with mgmt quotes.

- the trends we picked up - like every chain has a different read on mother & child (with genuine beef b/w apollo & rainbow) - one govt scheme that helped some hospitals and screwed others.

- the big one: are ARPOB, ALOS and occupancy even the right way to track a hospital anymore?

a lot more to unpack guys

link: https://t.co/W1B7KpfNZo

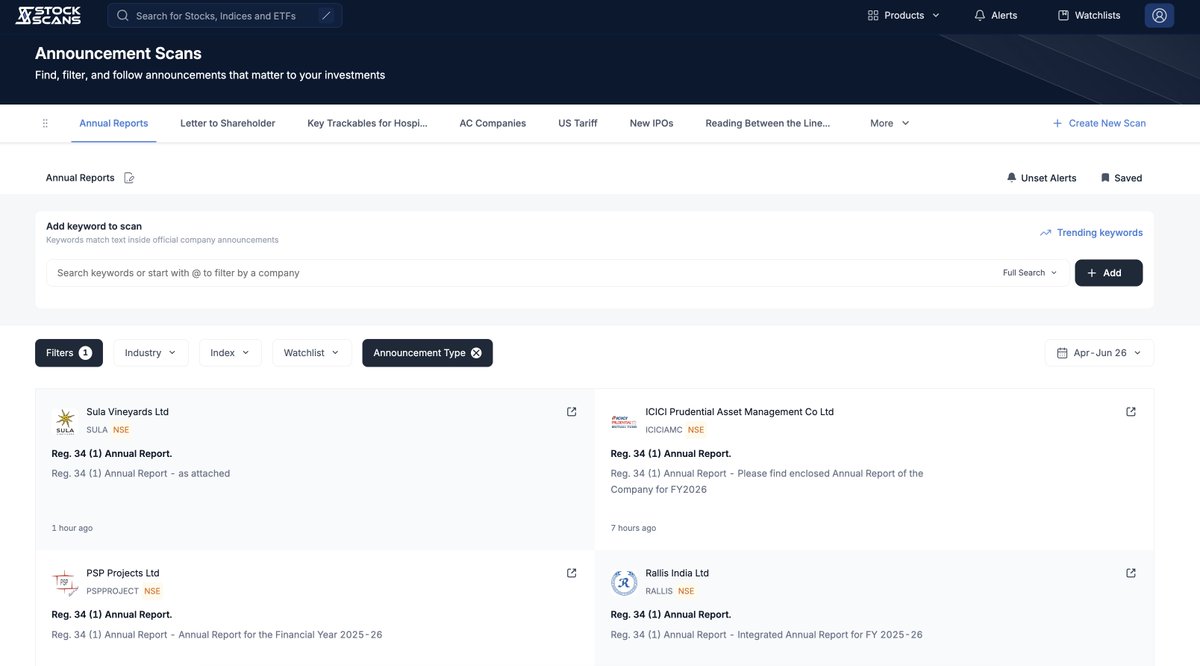

As FY26 results season comes to an end, keep a close watch on companies publishing their Annual Reports.

Annual Reports are one of the best sources to understand:

• Industry tailwinds and headwinds

• Management's long-term vision

• Capital allocation strategy

• Key risks and opportunities

• Competitive positioning

Make sure to run your Announcement Scans daily and set up alerts so that whenever a company releases its Annual Report, you receive an instant notification.

https://t.co/L3bK8C7CRS

Disc: Not a Buy/Sell Recommendation.

sattvānurūpā sarvasya śraddhā bhavati bhārata

śraddhā-mayo ’yaṁ puruṣo yo yac-chraddhaḥ sa eva saḥ ~B.G. 17.3

Faith shapes each being from within, according to the nature they’re in; A person is made of what they believe,

As one has faith, so one shall achieve.

- Today, approximately 89% of the company's code changes are contributed by Al agents.

- A new wave of entrepreneurs and businesses is being created, and we want to co-build the future of Agentic Commerce with them. Since AI mainstreamed two years ago the pace of change has radically accelerated, and we are building in a world of constant ambiguity.

There is no immediate endgame for how Fintech and Commerce will look post-AI, so we have chosen to experiment our way to the future of commerce, on the bedrock of AI.

~ Pine Labs PPT Q4FY26

Disc: Not a Buy/Sell Recommendations.

यततो ह्यपि कौन्तेय पुरुषस्य विपश्चितः ।

इन्द्रियाणि प्रमाथीनि हरन्ति प्रसभं मनः ॥

Turbulent by nature, the senses even of a wise man, who is practising self-control, forcibly carry away his mind, Arjuna.

B.G. 2.60

You know what?

Today, I will take you head on and not get intimidated by a 2 rs troll.

I have covered numerous sectors from Cdmo to aerospace to financials to shipbuilding and what not with an intention to share knowledge. Given your hate and stupidity you don’t even realise that I haven’t covered names like route etc that you have mentioned. I get it why you’re doing this- you want cheap attention & your twitter payout . Even businesses like alkyl at numerous places I have mentioned how margins are at an all time high and non replicable.

Many many businesses which have done well but given you just want to defame. I will mention this-

Those who know us and have followed hardwork of @soicfinance@ResearchSOIC - will know the value we have delivered.

For 2rs troll like you - this is the last bit of attention that you deserve especially when you can’t even write your real name.

Our work will go on and get better from here :)

The bee and the python are two excellent spiritual masters who give us exemplary instructions regarding how to be satisfied by collecting only a little and how to stay in one place and not move.

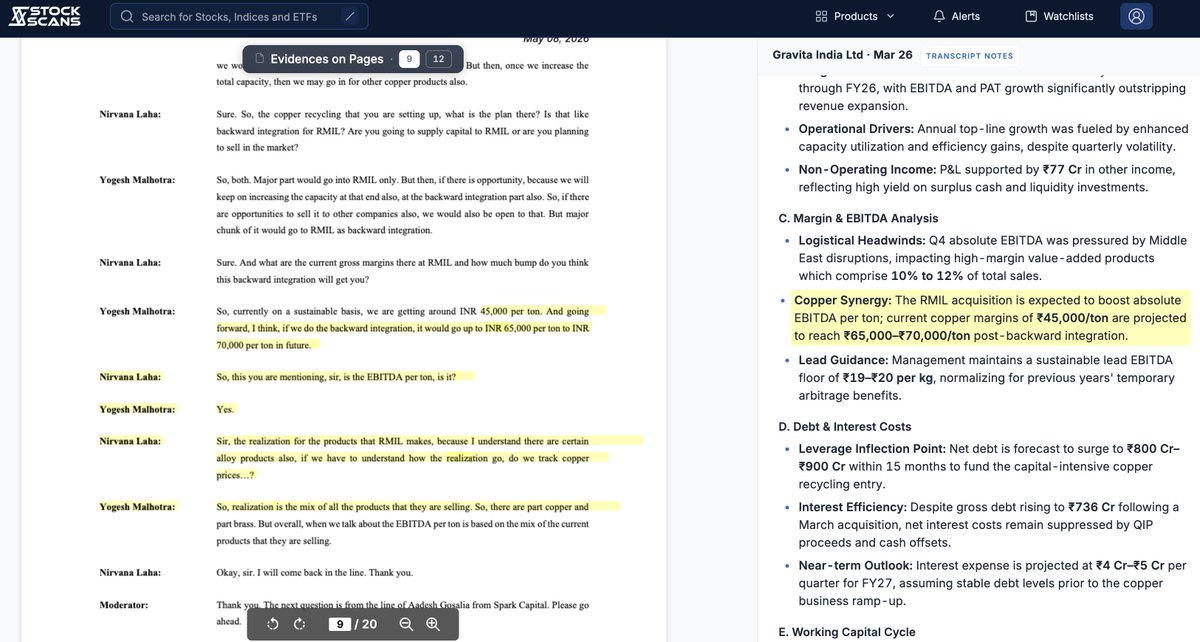

Concall Highlights - Gravita India Ltd.

1. FY26 Adj. EBITDA margin came in at 10.6% with PAT margin at 8.88%. Per-ton economics: Lead ���23,043, Plastic ₹16,043, Aluminum ₹12,328. Q4 EBITDA was pressured by Middle East logistics disruptions which hit value-added products (10–12% of sales) and Q1 FY27 EBITDA/ton is expected at the lower end of guidance until those normalize.

2. Total 4-year CAPEX has been revised upward from ₹1,200 Cr → ₹1,700 Cr, with copper alone consuming ₹700 Cr in CAPEX + ₹1,200 Cr in working capital. The ₹560 Cr RMIL acquisition (99.44% stake, 31,200 MTPA Gujarat facility) is the anchor; copper margins are projected to expand from ₹45,000/ton today → ₹65,000–70,000/ton post backward integration, targeting 20%+ ROCE for the segment. Net debt is forecast to spike from ~₹100 Cr today to ₹800–900 Cr within 15 months to fund this but the multi-year program is otherwise self-funded via internal accruals.

3. Capacity is set to nearly double 4.57 Lakh MTPA today → 8+ Lakh MTPA by FY29. Lead target was raised to 800,000 tons; the 45,000-ton Phagi (Jaipur) plant is physically complete and awaiting government approval for Q1 FY27 commissioning. Copper Phase 1 (29,400 MTPA Mandvi, ₹160 Cr) and Mundra rubber expansion both go live in H1 FY27, with copper scaling to 60,000 tons in 2–3 years and 100,000 tons by FY29.

4. Vision 2029: 20–25% volume CAGR, 50% revenue from value-added products (vs. 42% in FY26), and a 70+ country footprint. Segment EBITDA guidance: Lead ₹19–20/kg, Copper ₹45/kg (rising to ~₹60/kg at full integration), Plastic ₹10–12/kg, Rubber ₹7–8/kg.

Interesting Management Quotes-

"Net debt will surge to ₹800–900 Cr within 15 months to fund the copper build-out. After that, the multi-year program is self-funded external borrowing is reserved strictly for working capital, not asset creation."

"Sustainable lead EBITDA floor is ₹19–20/kg. Recent years had temporary arbitrage benefits we're normalizing out but the unorganized sector arbitrage shrinks as RCM and TDS on scrap come in."

"Lithium-ion volumes are not in our FY29 guidance that's pure additional upside. Steel recycling has been deferred 2–3 years so we don't lose execution focus."

"Q1 EBITDA/ton will likely sit at the lower end of guidance Middle East logistics disruptions are hitting the value-added mix, which is where our highest margins are."

"Full utilization of the 30,000-ton copper capacity needs roughly ₹1,000 Cr of dedicated working capital that's the 90-day cycle of imported copper scrap."

Read full Concall & Notes here: https://t.co/q0Cnfco5P3

Disc: Not a Buy/Sell Recommendation.