✨ By the Grace of God… Happy to Share release of Fifteenth Edition of GST Made Easy and Eighth Edition of GST Law and Practice (including Pocket Edition)✨

🌟 When something goes beyond numbers, it becomes a journey of faith, perseverance, and support. These milestones are not mine alone — they are built on the blessings of God, the encouragement of mentors, and the unwavering love of my parents and family and the unwavering support of @taxmannindia.

🙏 Thank you to my parents and family for being the pillars behind every edition, every page, and every word.

📘 Fifteenth Edition Released-GST Made Easy- From foundational concepts to nuanced issues, this book offers practical insights for day‑to‑day challenges under the GST regime.

📙 Eighth Edition Released-GST Law and Practice — A comprehensive compendium of CGST & IGST Acts, enriched with Rules, Notifications, Forms, Circulars, Clarifications, and Case Laws.

👉 This time, also available in a Pocket Edition for easy reference on the go.

Dear @TRAI,

Imagine your recharge plan is going to expire in 2 days.

Imagine someone is following your sister late at night, and she is trying to call you for help.

Imagine you are injured on the road and desperately trying to call a family member.

But before the call even connects, telecom companies play long warnings like “your plan is expiring soon, please recharge” in two languages. During this warning, the actual call does not connect, and valuable time gets wasted.

In emergency situations, even a few seconds matter. These repeated recharge reminders are extremely frustrating.

We already know when to recharge. Customers should not be forced to listen to long, nonsensical warnings.

Please order all telecom companies to immediately stop these nonsense warnings before calls, or allow the call to connect while the warning plays in the background.

Be serious.

When I raise issues on X about day-to-day problems of our Portals and CA practice in general, many accounts straightaway start replying Carbon credits, Forensic Audit, IP, Foreign Accounting etc. etc.

If you reply again, then they start talking about some new Certificate Courses!!

Do these people know that CAs exist in Tier 2 & Tier 3 cities too!?

Need genuine replies and opinions 🙏🏻

Enough is enough.

A humble but very firm request to all elected leaders of our profession - please speak up now. We need your voice, now more than ever! 🙏🏻

Every day, professionals are battling broken, unstable and poorly thought-out portals across all departments. Work that should take minutes is stretching into days, sometimes weeks and months. So many professionals are literally spending day and night firefighting and raising voice for technical glitches and believe me, this is seriously draining us mentally, professionally and personally.

Now to address the elephant in the room, we often get told “Why are you speaking? Let businesses speak, it is their issue.” But how can we remain silent when this is our day-to-day professional life? When compliance failures caused by system issues fall on our heads? When our credibility and reputation as CAs suffers because systems don’t work?

Repeated tagging, representations and feedback seem to vanish into silence. New statements are issued, new portals are rolled out, but stakeholder consultation is missing. The same issues and new ones keep appearing, with no accountability and even less resolution and full-on shamelessness of @IncomeTaxIndia@Infosys_GSTN@HelpdeskMCA21V3.

Leadership of the profession must toe the party line when needed and must also stand firmly with professionals when the ground reality becomes unbearable. We don’t need photo-ops. We need representation. We need strong voices raising real issues at the right forums. 🙏🏻

Enough is enough. Please speak for us. Please stand for the professionals you represent.

Rebate under Sec 87A cannot be denied just because income includes STCG (Sec 111A), if total income is below Rs. 7 lakh: ITAT

🚫 CPC’s system-based disallowance ≠ law.

✔ Appeal allowed, tax demand deleted.

❤️Like 🔁 Repost, 📝Comment “CITATION” to know citation

Industry chambers @FollowCII, @ASSOCHAM4India, @ficci_india, @phdchamber and @ICC_Chamber, you have a responsibility beyond conferences and policy papers.

When due process is bypassed and investor confidence is threatened, as in the case of the baseless FIR filed against Shri Anil Agarwal Ji, your silence is not neutrality. It is a failure of your core mandate.

Speak up for justice and what is right. That is what you exist for.

If a factory accident = FIR on the promoter, then..

Train accident → FIR on the Railway Minister?

Air crash → FIR on aviation authorities?

Pothole death → FIR on the Municipal Commissioner?

Accountability must be consistent , not selective.

🚀 Just launched something BIG for every CA & Tax Professional!

CA Prompt Library — 500+ AI Prompts, built specifically for taxation work.

No more staring at a blank screen wondering how to prompt AI. Just search, copy & go. 🎯

✅ 500+ ready-to-use prompts

✅ 27 categories (ITR, GST, TDS, Audit & more)

✅ Search any prompt instantly

✅ Edit prompts to fit your exact need

✅ One-click Copy

✅ Share via WhatsApp / Twitter / LinkedIn / Email ✅ Export to Excel / Word / JSON / Plain Text

✅ Bookmark your favorites

This is the toolkit I wish I had when I started using AI in my practice. 💼

👉 Try it free: https://t.co/6g9CV6U2Um

Built with ❤️ using @claudeai

Drop a 🔖 if you're bookmarking this.

Tag a CA friend who needs this RIGHT NOW. 👇

#TaxationUpdates #CharteredAccountant #AIforCA #TaxAI #PromptEngineering #GST #IncomeTax #AITools

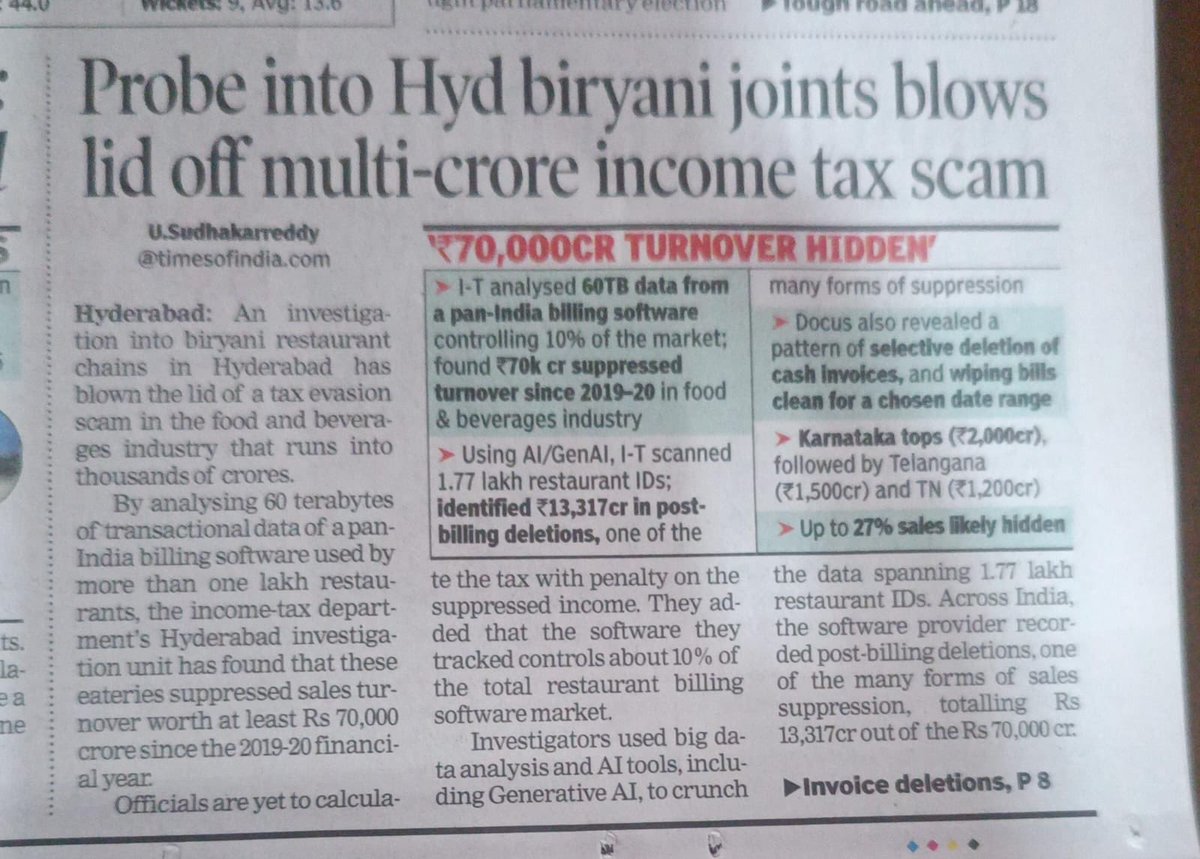

India Tax Probe Uncovers ₹70,000 Crore Hidden Restaurant Sales

India's Income Tax department analyzed data from a major billing software used by over 100,000 restaurants, uncovering at least ₹70,000 crore in suppressed sales through tactics like deleting cash invoices and under-reporting. The probe, using AI and big data on six years of records showing ₹2.43 lakh crore in total billing, flagged patterns across states with Karnataka, Telangana, and Tamil Nadu leading deletions. Officials call it just the beginning, praising the tech-driven approach while skeptics question AI reliability and note common industry practices—no penalties issued yet as liabilities are calculated.

This software is used by 10% restaurants, around 27% of sales were potentially the extent of under-reporting.

Extrapolating the number, this could be a Rs 700,000 crore under-reporting.

This is a much needed move.

The 2 crore odd of us who pay income taxes are bearing an inordinately high burden.

Widen the tax next and increase compliance, rather than taxing the salaried and compliant on all fronts.

There should be deterrent punishment for such tax evaders .

@PMOIndia@nsitharaman@narendramodi

@NalinisKitchen Income Tax Act clearly says that 50% of Gross Receipts or actually earned profit, whichever is more is considered as Taxable Income in case of specified professional under Section 58 (Erstwhile 44ADA)

By showing exactly 50% as profit with no actual expenses leads to tax evasion.

@PratibhaGoyal In the New Income Tax Act, Section 58(Erstwhile 44AD) is mandatory, means showing profit less than the specified % will attract tax audit in Section 63.

Can Section 73 be invoked for the purpose of recovery of Late Fees for delayed filing of Annual Return or GSTR-1

It’s very common these days wherein notices are normally being issued for recovery of Late Fees under Section 73 for Annual Return or GSTR-1. The question is can action under Section 73 be taken for recovery of Late Fees.

Section 73 provides for recovery of tax, interest and penalty thereon and there is no mention of Late Fees. Thus, Section 73 which provides for determination and recovery of tax, interest and penalty does not include within its ambit late fees and had the intent of the legislature been to do so, they could have very well provided the same in the legislature.

Not only that, additionally, if we go through circular No. 238/32/2024-GST Dated 15th October 2024 solely to understand the perspective of the government and why they did not allow late fees to be covered under amnesty scheme (without going into legality of the circular for the purpose of Section 128A) and refer to Question No. 12 at Point 4 which provides as under

Question-Whether Section 128A will cover waiver of penalties under other provisions, late fee, redemption fine etc?

Answer-It is clarified that any penalty, including penalties under section 73, section 122, section 125 etc, demanded under the demand notice/ statement/ order issued under section 73, is covered under the waiver provided under Section 128A. However, late fee, redemption fine etc are not covered under the waiver provided under Section 128A. Reading between the lines, in my opinion, answer to the question raised by this article is also covered under the given question.

If we give a thought that why as per the circular, late fee was not covered under Amnesty Scheme. It appears that the circular is based upon the understanding that similar to redemption fine which is not recoverable under Section 73, late fees also cannot be recovered under Section 73 as it is covered by Section 47. Therefore, provisions of Section 128A are not applicable for waiver of late fees since it was only for orders passed under Section 73 and late fees cannot be recovered under Section 73. Thus, this is a sort of admission only that provisions of Section 73 cannot be used for recovery of late fees.

Thus concluding, Section 73 and using the background of the clarification issued for making argument, it can be very well argued that no recovery of late fees can be made under Section 73 as it only provides for recovery of tax, interest and penalty.

PM Sir, we only demand a fair extension of Tax Audit due date — not for our comfort, but for MSMEs, for clients, and for the economy.

A proper audit in proper time ensures proper compliance. Please intervene. #Extend_DueDatesImmediately@nsitharaman@FinMinIndia@PMOIndia