Kevin clearly has all his ducks in a row and reading from the same script now. See MBSMKT WEEKLY below. Imagine if CPI had printed hot on Tuesday though. Right before the pre-FOMC blackout period. 2s already reflect two hikes so bear steepener and 10s at 4.75? Mortgages dodged a bullet. Lots of room to widen both the basis and primary/secondary spreads in that scenario. Double whammy. Phew....all is well in the world again I guess—except in Iran where reviews are probably less than five stars.

Have a great weekend. Go France...

AQ

https://t.co/0DX1mFQZSj

-----

MBSMKT WEEKLY 7/17/2026

The U.S. military hit 140 Iranian targets last weekend and markets wasted no time making a mess on Monday morning. Rates pushed to their weekly highs early Tuesday before a better-than-expected CPI print gave bonds room to breathe, making a July rate hike look more like theater than feasible policy. Chair Warsh’s first semiannual grilling on the Hill came and went immediately afterward without fireworks...and all was well in the world again — except in Iran where reviews are probably less than five stars. Kevin stuck to the synchronized script in his testimony and offered no forward guidance. A month into his tenure, the rest of the committee seems to have gotten the memo. Every speaker circles the same three inflation drivers — Tariffs, Mideast energy risk, and AI-related demand — while insisting the labor market is stable and balanced. At this point, the Fed sounds less like a committee and more like a muted all hands call that ends with strict instructions from HR: "no freelancing, no flair"

By 3pm Friday, 2s were 13 bps below the weekly high at 4.171%. 5s exited at 4.271%, 12 bps off their peak. 10s went out at 4.542%, 9 bps better than Tuesday morning’s worst levels.

Mortgage rates climbed to three-month highs on Monday as dollar prices fell and basis spreads widened on extension risk. CPI helped turn the tone, with belly coupons leading the recovery. Current coupons dropped sharply before finishing the week near 5.54%. Specified pool payups unfortunately failed to join the late-week bounce, as investors got pickier while borrowing costs sat in moneyness purgatory. Conventional 30-year payups faded across most stories, with the giveback naturally scaling higher in fuller coupons and lower loan-balance buckets where call protection has the most room to lose value. With mortgage rates near recent highs and refi incentive thin, buyers are not exactly lining up to overpay for prepay protection that may not materialize through the box. Extension risk remains elevated. Even the most aggressive recapture servicers are running out of cold-call material.

Next week should be quieter outside Iran. The data calendar is light and Fed officials are sidelined by the pre-FOMC meeting comms blackout. Treasuries have room to keep recovering from oversold levels

AQ/AD

Back-to-back calls with pipeline hedgers is all we've accomplished this week. Time well spent but kept hearing the same horror story about wide bookie screen bid/ask spreads. Sloppy mortgage markets aren't uncommon when OTC RFQ protocols govern execution, especially in July and August, but 10 ticks wide in an anchor coupon? Not normal. This is where multiple views of a TBA mid can make a difference (dealer-to-customer, dealer-to-dealer, model). That's for marks. Traders gotta pick up the phone and battle for bps though. Put your coverage in comp and develop relationships. Don't just blindly accept pictured levels..

Don't be shy to request a demo. dataQollab MBSMKT CLOSE below

AQ

https://t.co/0DX1mFRxHR

----

MBSMKT CLOSE 7/15/2026

A contained rates response this morning to a less than inflammatory PPI report allowed MBS to once again take the lead. Yesterday's CPI miss was not a one-off after PPI unexpectedly declined -0.3% MoM versus flat consensus and +0.6% in May, the weakest print since April 2025. The YoY pace slowed, Core PPI lower than expected, with May revised sharply lower to +0.1% from +0.4% initially: a meaningful downward revision that makes yesterday's CPI miss look even more credible in retrospect.

Two consecutive inflation misses in back-to-back sessions is the kind of sequential confirmation the bond market needed to sustain the CPI-driven rally rather than fade it as a one-day event. The conclusion is that nothing in this release gives the Fed urgency to hike. The July pause narrative is now firmly entrenched, and the September meeting is incrementally less certain for a hike as well, though two more CPI/PPI updates in July and August keep it an open question. Empire Manufacturing joined the conga line with a 15.6 beatdown of the 9.2 expectation, a genuine upside surprise on activity.

This all was pleasing music to mortgage’s ears, with the belly and upper coupons again leading the way. Spreads have come in 5bps the past two sessions on technical adjustments alone as flows appear sporadic at times. Aside from the recent spike to trading surrounding last week’s Class A allocations, flows have been melting with the summer heat. Once we get by Class C tomorrow, the remainder of the month’s focus again comes into question.

• Benchmark rates net lower 5bps: 10yr 4.55%, 5yr 4.26%, 2yr 4.14%.

• MBS prices gained five to 10/32nds, middles stack leading the way, with spreads 2+ ticks firmer in the belly/currents as lower wings lagged two ticks.

• Current Coupon -6bps to 5.50%; +110/5&10yr tsy blend (2 tighter).

• MBS trading volume low today at $65B, dropping July daily avg. to $87B.

• Econ Monitor Thursday; Weekly Jobless Claims, Retail Sales, Philly Fed, Pending Home Sales, Biz Inv, and Class C 48hr day.

AD

Happy 'National Franks and Beans Day'. Mortgages celebrated by getting all their parts caught in a zipper. Not sure if rates were the franks and vol was the beans but the outcome was painful either way. TBAs lower and wider with little to no mortgage rate moneyness left on the table. Quick explainer. Benchmark rates rose → Borrowers less likely to refi because of it → Loans expected to stay outstanding longer → MBS durations extended → TBAs sold off more than Treasuries.

AQ

https://t.co/0DX1mFQZSj

ps..name the movie!

----------

MBSMKT CLOSE 7/13/2026

Treasuries sold off and the curve bear-flattened after another weekend flare-up in U.S.-Iran tensions kept energy-driven inflation angst in control ahead of Tuesday morning’s June CPI release. The 2-year cheapened 7.3 bps to 4.2280%, the 5-year backed up 7.1 bps to 4.377%, and the 10-year rose 6.3 bps to 4.623%. The 2-year note is now at its highest yield since February 2025. The flatter curve reflects growing conviction that the Fed could actually tighten as soon as July, with fed funds futures now assigning roughly 45% odds of a hike versus about 25% on Friday. Governor Waller reinforced that possibility when he warned in a speech today that “if we get another hot reading on core inflation this week, then the FOMC will need to consider tightening monetary policy in the near term.”

Mortgages had a rough day -- moving lower in price and wider on spread -- as rising benchmark yields further reduced borrower refinance incentive and effectively extended durations. FNCL’s current coupon rose 8.3 bps to 5.639%, gapping 1.5 bps vs 5s and underperforming 10s by 2.4 bps. Decompressing coupon swaps were directionally supportive for MSR marks, and primary/secondary spreads did tighten as a result, but not enough to spare lender rate sheets from broad-based reprices for the worse. dataQollab’s par 30-year fixed note rate finished 4.5 bps higher at 6.581%. TBA volume was approaching $70B heading into the 4:45 p.m. marks, but the composition changed as the afternoon selloff gathered momentum. Roll share faded as outright volatility became the main driver, convexity accounts shed duration, and lenders added hedge coverage into higher pull-through and panic locking. Liquidity was more useful in theory than in practice. This was less a clean basis story than a hedging problem, with rising rates and extension risk moving back to the center of the market.

June CPI leads the calendar tomorrow, with headline CPI expected at -0.1% month over month, which would be the first negative print since May 2020 if realized. That forecast depends heavily on last month’s energy decline, but confirmation that inflation is cooling from the May peak would still matter by reducing the perceived risk of pass-through from headline inflation into core. A hotter core print would keep July hike odds elevated and likely reinforce today’s front-end pressure.

Warsh follows CPI with his first semiannual monetary policy testimony before the House Financial Services Committee at 10 a.m., with Barr, Goolsbee, Cook, and Bowman speaking later in the day. Warsh is likely to update the inflation assessment without offering the explicit guidance markets still want. Even if CPI softens, he will probably keep the inflation-first message intact and point to the Fed’s new task-force process as part of the broader policy review. CPI gets the first swing tomorrow, but Warsh gets the last word on how much comfort the market is allowed to take from it.

AQ/AD

.@dataQollab MBSMKT Weekly 7/10/2026

Rates moved higher this week as investors absorbed another round of geopolitical stress and the inflation imperative that comes with it. Another breakdown in the U.S.-Iran ceasefire, along with renewed hostilities around the Strait of Hormuz, pushed crude materially upward and kept the Treasury complex on the defensive. Oil finished the week nearly 7% more expensive, helping lift the 10-year Treasury yield by 7 basis points and leaving the 2s/10s curve slightly steeper. This was not the kind of geopolitical tapebomb event where Treasuries caught a safe-haven bid. Energy prices were the bigger story, and investors treated higher oil as a tax on duration rather than a reason to hide in it.

The June FOMC minutes kept the same pressure point in focus: inflation remains the center of gravity for Warsh’s Fed. Officials are clearly open to hikes if price pressures remain stubborn, and the committee continues to look more comfortable operating without a clear forward-guidance crutch. That matters for rates because it gives each data release more room to affect rate pricing. Warsh’s newly announced external task forces also confirmed the idea that the Fed is reviewing its framework more broadly. The balance sheet group naturally drew attention from the mortgage crowd, but for now there is no obvious indication that agency MBS runoff is the main target.

Mortgage spreads were steadier than the Treasury backup might have suggested, though dollar prices still felt the pressure. Current-production 5s and 5.5s were down 1/2 to 5/8 of a point on the week, while the 30-year current coupon rose ~7bps. Current coupon spreads widened 2bps to +112 over the 5/10-year Treasury blend but all the underperformance played out post-48hr day. That is not a full-blown basis problem, but it does show where the street’s comfort zone sits right now: shorter duration, cleaner profiles, and up-in-coupon exposure. When oil is driving the rates screen, nobody is eager to own the part of the stack that turns into a long weekend houseguest (lower coupons).

The most notable mortgage-market development was activity, not direction. TBA trading volume averaged nearly $100 billion per day, 20% above the recent pace, as geopolitical headlines collided with Class A settlement flows and active duration gap management. Rolls and allocations accounted for a meaningful share of the total, but the headline-driven pickup was not just noise. Lenders and servicers were forced adjust coverage as rates shifted quickly, especially when late-day war headlines hit. That made daily attribution less clean, but the practical takeaway was clear: summer liquidity may look calm until the screen suddenly asks everyone to run a fire drill.

Specified pools remained uneven. Investors continued to lean toward premium coupons and shorter-duration exposure, while lower coupons and parts of the belly lagged as extension exposure was repriced. Spec pools are also dealing with flatter S-curves, inconsistent special-roll support in premium coupons, and weaker GSE purchase demand. Those issues could ease if rates rally and volatility cools, but the current setup keeps rewarding structures that avoid getting dragged too far out the curve. Valuations may be more attractive in spots, but the entry point depends heavily on whether rates can stabilize and oil stops acting like it has a microphone.

June prepayments were mostly benign, with premium coupons generally coming in slower than model expectations. The exception was 6-8 WALA 6.5 major pools, where speeds picked up notably, led by rate-term refinance activity across several large servicers. In a borrower base where most homeowners lack a meaningful incentive, servicer behavior continues to explain a large share of prepayment variation. Pool selection remains less about the generic rate backdrop and more about who owns the borrower relationship.

Housing and origination data continued to point to a market that is open for business but operating with one foot on the brake. Mortgage applications softened around the holiday week, with MBA purchase activity down 2.2% week over week while refis rose 2.3%. Freddie’s 30-year mortgage rate increased 2 basis points to 6.49%, keeping affordability tight and refinance math limited. Existing home sales weakened, inventory improved only gradually, and buyers remained sensitive to every rate change. Wage growth is starting to compare more favorably against home-price appreciation, but not enough to change the broader affordability story yet.

Next week’s CPI report and an abundance of Fed Speak are the main events. The Fed minutes made clear that policy is now highly sensitive to whether inflation keeps proving sticky, especially with energy, tariffs, and AI-related demand sitting in the pressure bucket. A softer CPI print would give the front end room to shed some hike premium. A firmer print would keep a July hike in play and validate the concern that Warsh’s Fed is willing to surprise traders rather than pre-negotiate every decision. With crude elevated, MBS duration exposure more pronounced, and summer liquidity already thin, the market does not need much of a shove.

AQ/AD

Heavy volume in TBAs today. Class A allocations added to the total but the post-3pm pickup implies lenders were chasing coverage ratios after war headlines hit and LOs started panic locking. Attribution will be annoying in the AM as a result. Assigning the ask to loans and bid to hedges helps but few have that level of automation so expect a knee jerk in the morning when risk reports print.

AQ

https://t.co/0DX1mFQZSj

40°C Hinges. Boring Week Ruined...

Slow news week. “Extreme Heat Panel Cancelled Due to Extreme Heat” was the most shared story on Reuters. Funny that event cancellation happened in London during London Climate Action Week, right? In fairness, parts of Europe topped 40°C on Wednesday, which translates here in America to “hotter than the hinges on the gates to hell” Fahrenheit. Like I said... slow news week. Rates moved almost exclusively sideways sans a short window early Wednesday when 10s inexplicably dipped 10bps. Not going to overanalyze it at quarter-end but will say it probably didn't help lender P&L's. See more below. Boring week ruined...

AQ

https://t.co/0DX1mFQZSj

------

MBSMKT WEEKLY — 6/26/2026

Benchmark rates finished the week sharply lower with the 10-year shedding roughly 13 basis points from Monday's intraday high of 4.51% and the 2-year dropping ~15 basis points from its Monday peak of 4.23%. Oil's continued retreat toward pre-war February levels near $69/bbl, renewed confidence in the Fed's inflation-fighting credibility under Warsh, and quarter-end position-squaring all contributed to the cause with thin trading conditions acting as a directional amplifier.

Economic data releases this week confirmed macro stability without increasing urgency to hike rates. Supercore PCE was the most troubling print at +0.5% MoM with the YoY pace at 3.9%, highest since March 2024, and remains the central constraint on the front-end rally. Such hot Supercore numbers limit how far 2s can run even as oil-driven inflation risks recede (hence the June flattener) but the bar for outright rates hikes remains higher than the futures market implies given the fast money follow-on influence after Kevin Warsh’s hawkish first FOMC press conference.

MBS spreads held surprisingly firm given falling rates and a significantly flatter curve backdrop — a constructive outcome that was aided by subdued implied volatility views,...since lower rates, a flatter curve, and elevated implied vol in combination would have raised MBS option cost and increased modeled prepay probabilities. The FNCL current coupon closed Friday at 5.35%, tightening from +110 to +108 over the 5/10-year blend. The lower stack demonstrated notable resilience, though negative convexity profiles meant prices lagged the Treasury rally on spread — a predictable outcome as the curve gyrated from flatter to steeper mid-week and extension risk repriced. Sadly for lenders, secondary marketing desks likely absorbed hedge P&L damage into month-end as the primary/secondary spread widened approximately 7 basis points week-over-week into lower benchmark rates without a corresponding surge in new lock volumes.

The tradable window is compressed next week with SIFMA calling an early close July 2nd and full close July 3rd, shifting Non-Farm Payrolls to Thursday instead of the normal first-Friday print. The marquee event is Warsh at the ECB's Sintra symposium Wednesday — his first major policy communication since the June FOMC. A dovish surprise re-steepens the curve quickly, though the unknown pass-through of higher oil prices into core and the still-live geopolitical risk premium make that an unlikely outcome. The IRGC's attack on a Singapore-flagged vessel Thursday and Friday's tanker warnings in the Strait of Hormuz served as reminders that the ceasefire remains fragile. Next round of U.S.-Iran talks confirmed for June 28-29...

AQ/AD

MBSMKT: FED CHAIR WARSH (VOTER): MOST DATA CONSUMED BY THE FED RELIES ON OLD-FASHIONED SURVEY METHODS — CITES AS AREA FOR REVIEW UNDER DATA SOURCES TASK FORCE

Maybe we should more frequently interrogate data collection methodologies? 2% of what? The “what” is evolving faster than ever. Gig economies + new transaction technologies = fuzzy model inputs. #asterisk

Jay Now Silent Bob...

FOMC mañana plus an updated dot plot presser from our new Fed Chair. Kevin Warsh takes the podium for the first time at 2:30pm tomorrow. Not expecting much in the way of word count considering his anti-transparency approach -- so only one task remains ahead of the big event... deciding on Kev's new nickname. Haven't landed on the right call sign just yet. Need some help. Options include:

1. 'Spacey': We all know why that Kevin went silent so prob not a good pick, right?

2. 'Warsh and Peace': Inflation irony is off the charts here

3. 'Silent Bob': To honor Kevin Smith from 'Jay and Silent Bob'

4. 'KEVIN!': Home Alone for the win ...but always yelling, no exceptions

5. 'Mariner': Kevin Costner's character in 'Waterworld bc cold water is all Donald will be getting

6. 'Kev': Easiest name to yell if your D partner is getting forechecked by an absolute menace of a meathead

Vote on your fav or write in a better idea.

AQ

https://t.co/0DX1mFRxHR

This is def happening tonight:

“Good evening. I'm Tom Tucker and this is your Quahog Nightly News. Our lead story tonight? First, AI came for our passwords. Then it ruined social media. And now, according to new layoff data, job hungry robots are rising...up org charts. Tricia Takanawa with more."

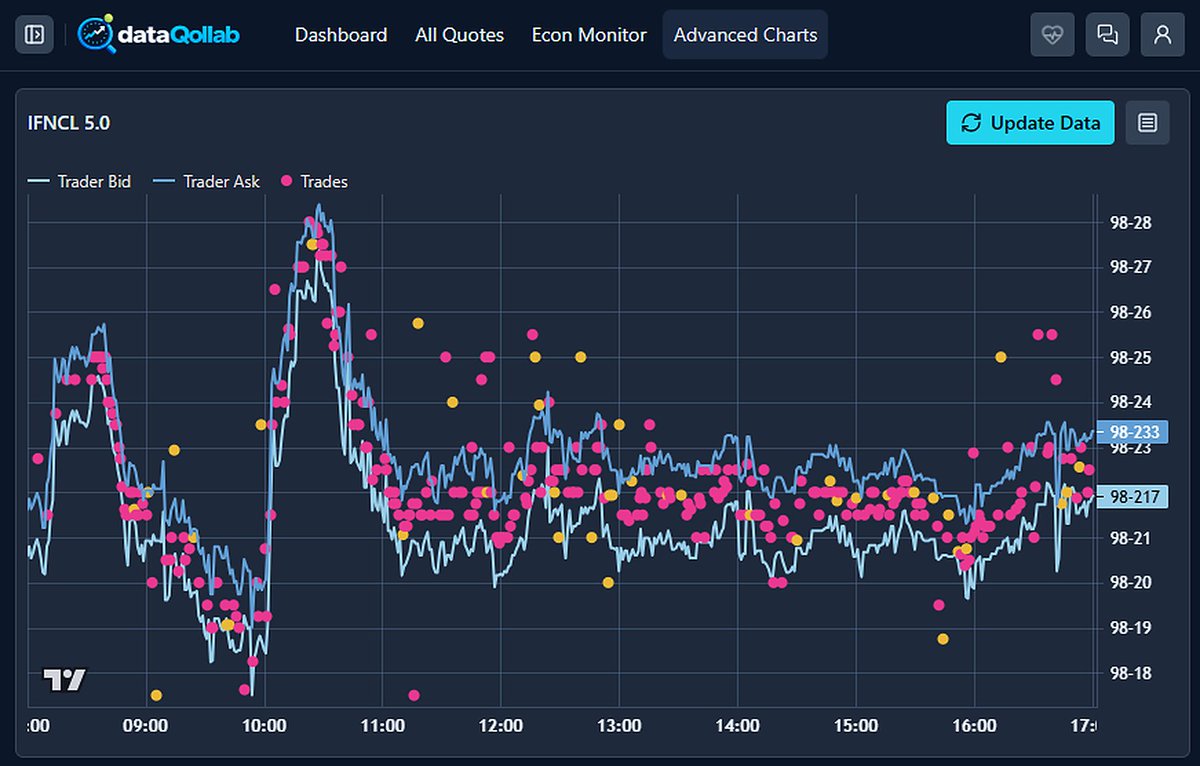

updating our TTB assumptions was fun this week. mortgage trading is once again an art after 15 years of artificial vol stomping. convexity matters again and it shows on the screen. check out our model driven FNCL 5.5 bid/ask vs actual trades yesterday and today. scatter plot highlights dealers chasing hedge ratios/repricing new convexity profile.

Best Advice for Handling Hedge Volatility...

Ignore all advice and say this prayer....

Frank, grant me the serenity to accept the deltas I cannot hedge,

the courage to manage risks I cannot model,

and wisdom to know the difference between real news and fake news.

All glory and honor are yours, Fabozzi forever and ever, Amen

Cool chart attached. dataQollab MBSMKT CLOSE below...

AQ

MBSMKT CLOSE 5/21/2026

The day pivoted on a single headline — reports of a U.S.-Iran ceasefire draft mediated by Pakistan turned a hawkish, energy-driven session on its head. Yields opened higher after the overnight uranium dust-up, only to 180 once (YET TO BE CONFIRMED) ceasefire news crossed the social wire early this afternoon. Crude collapsed nearly $6 from the morning highs, equities tacked on a full point off the open, and Treasuries ground their way back to lower yields with the long end leading. MBS, which had been on the back foot for much of the morning behind wider spreads and softer technicals, flipped to a positive day with hedge ratios chasing the rally which allowed lenders to recall and reprice rate sheets for the better. Inflation internals continue to catch the attention of vigilant eyes after hot pricing internals were obvious in both the Philly Fed and S&P PMI, plus two Fed speakers (Barkin, Goolsbee) flagging persistent inflation concerns — but the ceasefire narrative carried the tape. As Friday's early close approaches with Memorial Day weekend just beyond, desks are unlikely to carry meaningful risk with peace-or-escalation event risk hanging over the holiday.

• Benchmark rates close mixed but well off intraday highs; 10yr 4.566% (-1.9bp), 5yr 4.238% (-0.7bp), 2yr 4.075% (+1.6bp); flattener, 2s/10s 49bp (-3.6bp).

• MBS prices reverse morning weakness, finish modestly higher on the day; FNCL 5.5 99-235/26, FNCL 6.0 101-183/195, G2SF 5.5 100-01/035; spreads two to three ticks tighter into the close, convexity below par outperformed.

• Current Coupon sheds 2.7bps to 5.568% (~8bps off midday high): FNCL +132.5/5s (2.8bps tighter), +100.0/10s (1.2bps tighter)

• TBA trading volume $77B; modest pickup post-ceasefire draft headlines but slow after; Rolls 15% of volume; FNCL 4.0 drop a plus higher

• Econ Monitor tomorrow: 4am Fed's Waller speech; 10am UMich Consumer Sentiment (prev 48.2) / Expectations (prev 48.5) / 1yr Inflation Expectations (prev 4.5%) / 5yr Inflation Expectations (prev 3.4%); 1pm Fed Chair Warsh swearing-in ceremony

• Early close ahead of Memorial Day weekend

https://t.co/0DX1mFQZSj

inflation.

MBSMKT: S&P GLOBAL FLASH PMI (MAY): SUPPLIER DELIVERY TIMES LENGTHEN MOST SINCE AUG 2022 ON WAR-RELATED DISRUPTIONS, TARIFF CONSTRAINTS

MBSMKT: S&P GLOBAL FLASH PMI (MAY): INPUT BUYING RISES STEEPEST SINCE APR 2022; INPUT INVENTORIES BUILD

MBSMKT: S&P GLOBAL FLASH PMI (MAY): SERVICES INPUT COSTS POST STEEPEST RISE IN ONE YEAR

MBSMKT: S&P GLOBAL FLASH PMI (MAY): OUTPUT PRICES RISE FASTEST SINCE AUG 2022; GOODS PRICES HIGHEST SINCE SEP 2022

MBSMKT: S&P GLOBAL FLASH PMI (MAY): SERVICES SELLING PRICE INFLATION HITS 10-MONTH HIGH, AMONG SHARPEST IN 4 YEARS

Bonds are back on the inflation narrative which is now more sticky than the aftermath of Donald's tummy time with President Xi today. STIRS started baking-in Kev's first hike months ago but 2s officially pressing through 4.00% implies a whole new level of 'WTF ARE WE DOING' front-end frustration. Unfortunately for mortgages, duration don't sleep on vol and market profile in futures ain't exactly our friend. That smile isn't making any hedger grin. This is when rate shocks start to look silly. Enough said for embedded optionality. Extend screen weights and transact when yields are getting grabbed. Pain for payups in the process because no one needs protection...

Realized cost of being short gamma becomes P&L convexity risk in these environments.

AQ

https://t.co/0DX1mFQZSj

TBAs traded heavy to ratios into falling prices today. Inflation is a problem. Easy to see mortgage basis underperformance on https://t.co/BEaAmxTYo2 charts. The @dataQollab model price is duration driven without any other influence while our trader price pushes model levels around like a wholesale screen maker would based on liquidity. Lower and wider all day. Pink and yellow dots are actual trades.

Degenerate trading algos sent stocks to new record highs this week after Tinder and Zoom announced 'proof of humanity' eye-scan technology that helps humans identify other humans on the internet. How long before bots start shorting actual people on actual prediction markets? Being the adult in the room isn't getting any easier for bonds. Not when robots are running the Ricky Bobby "if you ain't first, you're last" system prompt. Everything feels algorithmic at the moment. Headlines hit. Sentiment is scored. Algos react. Last trade moves the whole pile. Delta hedgers chase tolerance. Repeat the following morning after attribution analysis reveals an unexpected shock and executives blame you for the edge case. Rates won't tolerate this for long. Vector heads are actively accumulating evidence to validate any scenario that restores bonds as the "adult in the room" i.e. stop being full blown price takers to oil. Next up is NFP. Until then, tapebombs are always a problem and the GSEs will put out cash window BWICs. Those covers will reset payups for the entire month of May.

How much day 1 payup margin you got baked into late stage uncommitted loans???

AQ/AD

@dataQollab https://t.co/qx3JTUwkcb CLOSE 5/1/2026

• Programmatic hand moving still rates in lockstep with oil futures; Strategic bias is a guessing game

• Lots of huffing and puffing, no house blown down; 10yr exits UNCH at 4.371%, 5yr +0.9bps at 4.014%, 2yr +0.9bps at 3.878%

• Oil algos loved peace talk on the tape this AM but bots quickly covered shorts before weekend

• S&P 500 and NASDAQ post sixth consecutive weekly advance, longest run of weekly gains since October 2024

• MBS barely earned a participation trophy this week; Be careful with payup durations and rate sheet margins

• NFP next week. Bonds getting closer to confirming stagflation story

AQ/AD

Boring start to the day but (unconfirmed) headline angst eventually got the best of bonds. Benchmark rates spiked higher around 1pm and no one cared to catch the falling TBA knife. So lower and wider we went. The mortgage basis traded heavy to ratios as levels fell. Lenders repriced for the worse shortly thereafter . Not much movement in rolls but front-month FNCL 4.5s and 5s looked like Jean Claude Van Hamme and Chunk Norris by 4pm...

Minimal day-over-day change in mortgage rates though. Just gyrations within the range. @dataQollab

AQ

https://t.co/0DX1mFRxHR