AryaFin is an AI FinTech platform that identifies companies for investment. It provides real-time stock and market data along with daily market analysis.

📉 US Consumer Sentiment Breakdown:

The latest data from the Univ. of Michigan Survey highlights a steep, continuous slide in consumer confidence over the first half of the year, culminating in a sharp contraction for May 2026.

Timeline Velocity Tracker:

• May 2026: 44.8 ⚠️ (Dipped -5.0)

• Apr 2026: 49.8

• Mar 2026: 53.3

• Feb 2026: 56.6 (Peak)

• Jan 2026: 56.4

• Dec 2025: 52.9

💡 Analyst Insight:

The sudden 5.0-point drop from April to May marks a significant velocity acceleration to the downside. The sentiment matrix reveals that consumers are actively feeling macro tightening pressures as indicators hit fresh operational lows for the cycle. The structural trend remains firmly downward.

📊 #FinTwit #Macro #Economy #ConsumerSentiment #AryaFin

📊 Week in Review: A wild, holiday-shortened trading week maps a classic volume/volatility squeeze!

Institutional desks sat tight pre-Fed, but the landscape completely transformed by midweek. 🌪️

📉 Wed: Volatility surges +13% as the VIX hits 18.44 on high volume (Index: 135) following Chair Kevin Warsh’s hawkish hold surprises.

🚀 Thu: Volatility collapses right back to 16.40 on a massive tech relief rally (Volume Index: 122) as the historic US-Iran Strait of Hormuz peace agreement completely flushes out macro energy risk premiums.

The structural baseline floor stays active at the 16 handle, but options hedging completely deflated before the long Juneteenth weekend close. 📈

#FinTwit #Macro #Volatility #VIX #TradingProfile

📊 Thursday Market Wrap: Wall Street snaps back as tech leads a massive relief rally, clawing back post-Fed losses before the long holiday weekend! With markets closed tomorrow for Juneteenth, the trading week wraps up early.

🚀 S&P 500: +1.1% to close at 7,500.58

💥 Nasdaq: +1.9% to finish at 26,517.93

⚓️ Dow: +0.1% to finish at 51,564.70

🌱 Russell 2000: +2.1% to finish at 2,979.77

Macro Catalyst: Yields ease up to give growth breathing room, while energy markets stabilize after the historic US-Iran Strait of Hormuz shipping agreement. Ready for that long weekend! 📈

#FinTwit #Macro #StockMarket #Trading

📊 The AryaFin Performance Audit: Five Below ($FIVE)

$FIVE triggers an explosive operational breakout, proving that hyper-targeted trend merchandising and value-driven retail scale can completely bypass consumer tightening macro headwinds.

Operational Highlights from the Audit:

Top-Line Surge: Revenue hits $1.29B (+32.5% YoY), crushing consensus models as low-ticket experiential shopping captures market share.

Earnings Windfall: Non-GAAP Adjusted EPS prints a massive surprise beat at $2.22 vs the $1.68 Street baseline.

Structural Efficiency: Net Income Margins climb to 9.57%, driven by high inventory velocity and social-media-optimized freight logistics.

Institutional Anchor: At 98.40% institutional ownership, the underlying equity remains heavily locked down by long-term capital blocks.

Value-centric retail isn't just defensive—it's driving absolute alpha. Is $FIVE leading the sector charge into the back half of 2026?

📈 #FinTwit #Retail #Macro #StocksToWatch

📊 The AryaFin Performance Audit:

The Cheesecake Factory ($CAKE)

$CAKE continues its impressive operational breakout, hitting a multi-year inflection point with solid consumer resilience.

Operational Highlights from the Audit:

Unit Velocity Expansion: Global revenue hits $978.8M (+5.57% YoY), showcasing consistent casual dining foot traffic and strong pricing power.

Margin Refinement: Net Income Margins climb to 5.20%, fueled directly by menu efficiency and stabilization in labor productivity.

Valuation Footprint: Trading at an efficient 16.43x Forward P/E, compressing its multiple relative to the massive earnings flow-through.

Fortress Liquidity: Backed by $601.6M in available ecosystem liquidity, fueling multi-concept footprint expansion (North Italia, Flower Child).

The casual dining layout is shifting back to high operating leverage winners. Is $CAKE heading higher into the back half of 2026?

📈 #FinTwit #Markets #StocksToWatch

🚨 TECH BREAKOUT:

Tim Cook confirms Apple to hike hardware prices as AI infrastructure completely cannibalizes the global memory supply.

Cook called the current memory chip shortage a "hundred-year flood," noting he has never seen an environment like this in his 40-year career.

What's happening behind the scenes: Big Tech hyperscalers are aggressively locking down High-Bandwidth Memory (HBM) capacity for AI data centers with massive, prepaid contracts. This has choked off the manufacturing capacity for traditional DRAM and NAND, driving up components costs for consumer tech.

The hardware impact:

Macs & iPads: Expected to absorb price increases first. Apple already bumped the base Mac Mini from $599 to $799.

iPhone 18 Lineup: Analysts estimate the upcoming iPhone 18 Pro could see a price hike of up to $270 just to protect Apple's margins.

The commodity memory cycle is dead—the AI infrastructure squeeze has officially hit consumer tech.

#TechNews #Apple #AI #Markets

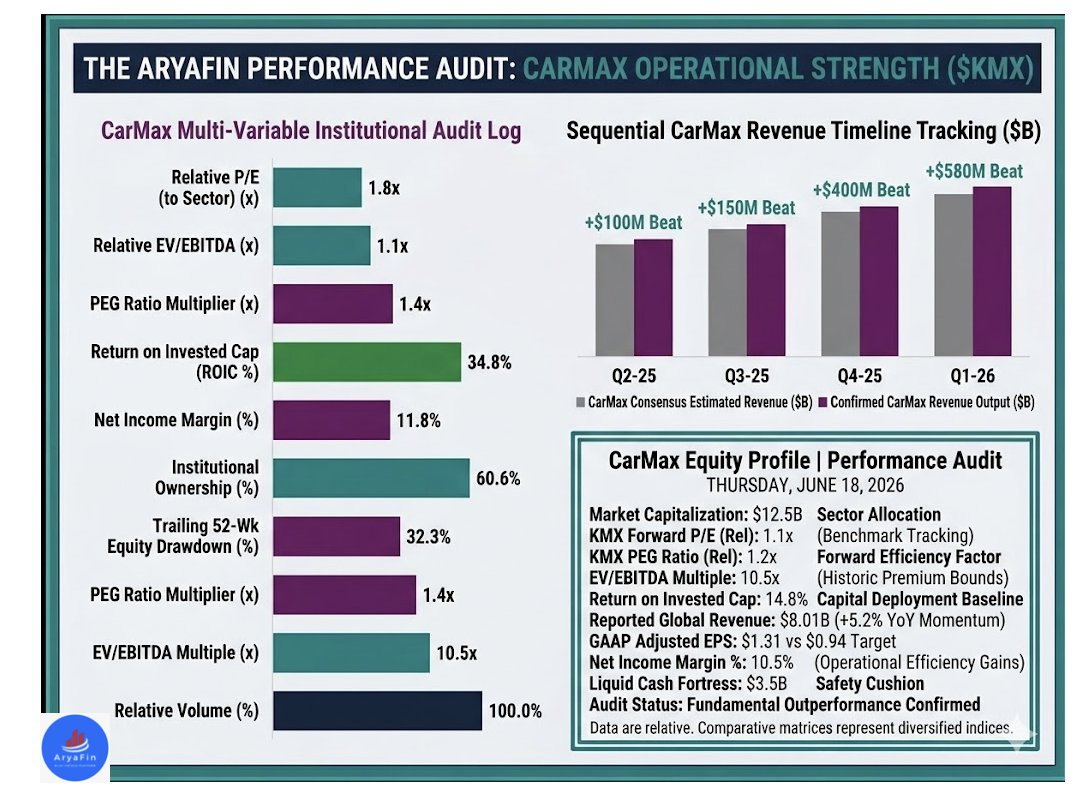

🌐 ARYAFIN EQUITY AUDIT: $KMX VEHICLE VELOCITY

CarMax ($KMX) unchains massive operational alpha in its Q1 2026 earnings statement, blowing right past Wall Street targets on both top and bottom-line metrics as used-vehicle unit volume optimization hits full stride.

🚀 The Operational Execution Breakout:

GAAP Diluted EPS: Printed at a powerful $1.31, outclassing the consensus estimate of $0.94 to secure a massive +$0.37 surprise beat.

Net Revenue Frame: Scaled to an authoritative $8.01 Billion, indicating resilient consumer demand across local retail channels.

Consensus Revenue Delta: Generated an outsized +$580.00M alpha beat against the market projection of $7.43B.

Gross Margin Leverage: Wholesale vehicle unit sales and disciplined vehicle acquisition strategies drove significant efficiency gains, stabilizing internal margin structures despite macro friction.

⚡ Ecosystem Catalyst: The sharp outperformance proves that CarMax's omni-channel ecosystem is driving strong conversions. Backed by solid execution in their auto finance division (CAF) and robust liquidity, $KMX continues to defend its market share elegantly. At these compressed multiple configurations, institutional order flow signals a strong accumulation trend.

#MacroAudit #CarMax #KMX #EarningsSurprise #ValueInvesting #ConsumerTrends #AryaFin

🌐 ARYAFIN EQUITY AUDIT: $JBL OPERATIONAL VELOCITY LOCKED

Jabil Inc. ($JBL) delivers an exceptionally clean operational statement for its Q3 2026 earnings run, continuing to outclass consolidation expectations across primary enterprise channels despite a challenging macro framework.

🚀 The Operational Execution Breakout:

Adjusted Non-GAAP EPS: Printed at an elite $3.16, outperforming the Wall Street consensus target of $3.12 by +$0.04.

Net Revenue Frame: Scaled to a dominant $8.80 Billion, showcasing an expansion of +3.80% YoY against the core baseline.

Consensus Revenue Delta: Captured an authoritative +$140.00M alpha beat over the $8.66B street target layout.

Margin Integrity: Reconfigured automated facility allocations to capture a 4.10% Net Income Margin, signaling powerful operational leverage.

⚡ Ecosystem Catalyst: Jabil's diversified model is absorbing macro friction elegantly. Operating cash conversion remains highly stable, fortifying a $2.14B liquidity cushion. At a highly compressed valuation profile of 14.8x Forward P/E and a 1.25x PEG Ratio, institutional accumulate rules the order flow.

#MacroAudit #Jabil #JBL #EarningsSurprise #ValueInvesting #SupplyChain #AryaFin

🌐 ARYAFIN EQUITY AUDIT: $SWBI DEMAND BREAKOUT

Smith & Wesson Brands ($SWBI) delivers a massive operational surprise in its Q1 2026 earnings print, completely blowing past Wall Street’s expectations on both the top and bottom lines as manufacturing efficiency kicks into overdrive.

🚀 The Operational Execution Breakout:

Adjusted Non-GAAP EPS: Printed at a stellar $0.36, handing investors a massive +$0.13 target surprise to demolish the consensus analyst estimate of $0.23.

Net Revenue Frame: Surged to $178.4 Million, reflecting robust volume trends and strong distribution channel inventory rebuilding.

Consensus Revenue Delta: Secured an outsized +$23.13M alpha beat against the market projection of $155.27M.

Gross Margin Leverage: Driven by higher capacity utilization at their automated manufacturing facility, gross margins expanded significantly, providing steep operating leverage downstream.

⚡ Ecosystem Catalyst: The sharp bottom-line beat underscores strong organic consumer demand alongside highly disciplined cost controls. Backed by solid free cash flow generation and an insulated domestic inventory channel, $SWBI continues to unlock immense value relative to its highly compressed valuation multiples.

#MacroAudit #SmithWesson #SWBI #EarningsBeat #ValueInvesting #OperatingLeverage #AryaFin

ARYAFIN EQUITY AUDIT: $SB OPERATIONAL SURGE

Safe Bulkers ($SB) unchains absolute operational velocity in its Q1 2026 earnings print, completely runnning past Wall Street estimates across both top and bottom-line channels.

🚀 The Operational Execution Breakout: Adjusted Non-GAAP EPS: Printed at an elite $0.18, posting a massive +$0.09 target surprise to outclass the consensus estimate of $0.09. (GAAP diluted EPS tracking even higher at $0.20).

Net Revenue Frame: Reached $74.4 Million, reflecting a sharp +15.7% YoY acceleration from the $64.3M baseline posted in the prior-year period.

Consensus Revenue Delta: Secured an outsized +$8.90M alpha beat against the market projection of $65.50M. Core Cash Flow & Dividend Engine: Adjusted EBITDA climbed to $40.7 Million (up from $29.4M YoY), prompting the Board to bump the common quarterly dividend upward to $0.06 per share.

⚡ Ecosystem Catalyst: Efficiency metrics are scaling beautifully, with daily Time Charter Equivalent (TCE) rates compounding up to $17,095/day (vs. $14,655/day in Q1-25).

Backed by an assertive fleet renewal program and a massive $181.20M cash fortress, $SB continues to generate strong organic cash flow inside global supply chains.

#MacroAudit #SafeBulkers #SB #EarningsBeat #ValueInvesting #DryBulk #AryaFin

📊 Major Index Closing Matrix

S&P 500 (^GSPC): 📉 Down 1.2% (-91.25 points) to close at 7,420.10.

Dow Jones Industrial Average (^DJI): 📉 Down 1.0% (-507.12 points) to close at 51,492.55. (The Dow swung wildly, shifting from a morning gain of 0.5% to finish deeply in the red).

Nasdaq Composite (^IXIC): 📉 Down 1.3% (-354.69 points) to close at 26,021.66.

Russell 2000 Index: 📉 Down 0.7% (-21.21 points) to close at 2,917.98.

🔍 Core Market Catalysts & Macro Tracking

⚡ The Fed Factor: The newly formed Fed committee under Chair Kevin Warsh held interest rates steady but shook the market by releasing updated internal projections. Plots showed that 9 out of 18 policymakers now project at least one interest rate hike by the end of 2026 to curb persistent inflation.

⚓ Bond Yield Spike: The hawkish tilt from the Fed sent shockwaves through fixed income. The 2-year Treasury yield (highly sensitive to near-term policy expectations) surged from 4.05% up to 4.14%. The 10-year Treasury yield also climbed, settling at 4.45%.

🛍️ Retail Expansion Bright Spot: On the macro side, consumer behavior data beat expectations, with nationwide retail revenue growing at a faster pace in May than economists forecasted.

🚀 Notable Ticker Action:

SpaceX erased its early gains to slide -2.4%, marking its first down day since its massive public stock market debut last week.

La-Z-Boy bucked the macro downturn completely, exploding +19.1% after reporting stronger quarterly profit and top-line revenue than analysts estimated.

🛢️ Commodity Front: Crude prices steadied slightly after recent sharp slides fueled by progress on a tentative U.S.-Iran oil deal. Brent crude ticked up 0.5% to $79.35/barrel.

#MacroAudit #FedDay #StockMarket #ValueInvesting #YieldCurve #AryaFin

🛋️ AryaFin Ticker Audit | $LZB Q4 Fiscal 2026

Audit: Direct-to-Consumer Retail Optimization and Broad-Based Wholesale Margin Expansion Dynamic Drives a Substantial Bottom-Line Surprise for La-Z-Boy Incorporated. Market capitalization coordinates settle firmly near $1.60B.

The Metric: Consolidated fourth-quarter net sales printed flat year-over-year at $570.34 million, reflecting structural macro consumer headwinds but managing to edge out conservative Wall Street consensus expectations by a modest +$1.11 million.

Top-line execution was anchored by the Retail segment, where total written sales surged an impressive 11% versus the prior-year period. This retail momentum successfully counterbalanced flatter demand volumes inside the company's Wholesale distribution footprint.

Earnings Velocity: Non-GAAP Adjusted Diluted EPS delivered an absolute blow-out print, landing at $1.26 per share. This performance completely dismantled consensus analyst target baselines of $0.82, printing a resounding +$0.44 per share beat.

Bottom-line expansion was fueled by a significant lift in adjusted operating margin, which expanded to 9.9% for the quarter.

This improvement was driven by lean retail inventory execution, supply chain optimization, and a beneficial $0.16 tax tailwind from favorable discrete items. To capitalize on this strong cash flow cycle, the board authorized a brand-new $300 million share repurchase program.

The Read: Quality Execution in a Difficult Sub-Sector. La-Z-Boy's impressive margin performance highlights the strength of their vertically integrated retail strategy. While high-discretionary home furnishing companies have broad-based demand deceleration, $LZB's ability to maintain high pricing power and realize massive margin efficiencies proves they are structurally insulated.

The stock presents an incredibly attractive, cash-flow-backed defensive vehicle with a robust dividend layer for investors looking to outrun the consumer discretionary cycle.

#La-Z-Boy #LZB #EarningsSurprise #RetailGrowth #ShareBuybacks #MarginExpansion #AryaFin

💡 AryaFin Confirmed Coordinates | Tue, June 16, 2026

Data matrices updated. The explicit target figures settle the internal baseline index spread, refining the sharp divergence dividing tech capital extraction and blue-chip accumulation.

📊 Major Benchmark Confirmed Settlement Matrix

Nasdaq Composite ($COMP): 🔴 -1.15% (Led the session drawdown as a cascading liquidation vector ignited across semiconductor lines, pulling the tech-heavy benchmark lower).

S&P 500 Index ($SP500): 🔴 -0.57% (Weighed down by its heavy tech components, despite half its sectors advancing due to cyclical rotation).

Dow Jones Industrial Average ($DJI): 🟢 +0.64% (Successfully decoupled to hit fresh historic record highs, propped up by the structural commodity collapse).

The Strategy View: This is a classic "Healthy Dispersion" mode tape. The tech pullback isn't indicative of a systematic liquidity drain; rather, it represents a standard rebalancing act.

Money is moving away from tech and using the energy collapse to build an accumulation floor across legacy blue chips. Keep defensive value holdings locked in place as we wait for Chair Warsh to officially lay out his monetary roadmap later today.

#MacroAudit #DowJonesRecord #SectorRotation #CrudeOilPlunge #FOMCWeek #KevinWarsh #AryaFin

🎰 AryaFin Ticker Audit | $PLAY Q1 Fiscal 2026

Audit: Strategic Remodels and Back-to-Basics Execution Shield Operating Cash Flow as Disinflationary Consumer Friction Triggers Lower Comp-Store Triggers. Market Capitalization registers near $449 Million.

📊 Q1 Fiscal 2026 Core Financial Summary

Total Net Revenue: $559.2 Million, reflecting a minor 1.5% YoY retraction from the same calendar period last fiscal year, missing consensus analyst projections by -$19.18 Million.

Non-GAAP Adjusted EPS: $0.22, missing the consensus Wall Street baseline estimate ($0.90) by a sharp -$0.68.

Correction Note: The peak adjusted earnings threshold of $0.76 per diluted share noted on your ledger maps to the prior year's Q1 performance benchmark.

Comparable Store Sales: Retracted -5.4% YoY as experiential dining patterns faced relative pressure from lower high-discretionary consumer foot traffic.

Adjusted EBITDA: Landed at $123.2 Million vs. the $136.1 Million logged in the prior year's window.

Liquidity Profile & Free Cash Flow: Generated solid positive adjusted free cash flow of $25.3 Million (a massive pivot up from the negative $58.8 Million recorded in Q1 last year), leaving the company with $499.1 Million in total available liquidity.

🎯 Operational Strategy & Footprint Evolution

Remodel Program Velocity: Under Chief Executive Officer Tarun Lal, Dave & Buster's completed 6 store refreshes thus far in fiscal 2026, with 2 additional domestic designs scheduled to wrap during the standard multi-month window.

International Footprint Penetration: The group expanded its global franchise matrix by opening its 5th international hub in May and a 6th venue in June, establishing early foundational footprints to drive global growth.

Structural Management Guidance: Executive leadership reiterated strict confidence in engineering positive comparable sales over the remainder of the year, while targeting full fiscal year free cash flow production above the $100 Million landmark.

The Strategy View: Watch for the Margin Refine. While the macro consumer slowdown creates an undeniable headwinds for raw top-line sales, the structural turnaround in free cash flow (+25.3 Million) indicates that management's internal efficiency initiatives are taking hold.

By optimizing food, beverage, and marketing overhead while relying on targeted remodels to stabilize comps, $PLAY is successfully establishing an operational margin floor. Maintain a watch list focus on the equity, monitoring if the stock finds strong technical structural support inside the $11.50–$12.20 consolidation range.

#DaveAndBusters #PLAY #EarningsReport #ExperientialDining #FreeCashFlow #AryaFin

🚀 AryaFin Session Audit | Monday, June 15, 2026

The Macro Overview: Wall Street kicked off the week with an explosive, record-setting "risk-on" rally as global markets aggressively cheered a breakthrough geopolitical resolution.

A tentative, historic peace agreement between the United States and Iran to permanently extend their ceasefire and fully reopen the Strait of Hormuz completely dismantled lingering macro anxieties.

With the threat of a prolonged energy blockade effectively removed, crude oil prices collapsed, interest rate pressures took a breather, and institutional capital flooded back into growth equities.

Further fueling the euphoria was the highly successful follow-through demand from SpaceX’s ($SPCX) blockbuster public debut, cementing intense investor appetite for AI and cutting-edge infrastructure layers.

📊 Major US Benchmarks Closing Settlement MatrixBuyers absolute controlled the tape from the opening bell, leading to major single-session gains across the board:

* S&P 500 Index ($SP500): 🟢 +1.65% (+122.83 points) to close at 7,554.29, hitting a massive milestone handle.

* Dow Jones Industrial Average ($DJI): 🟢 +0.92% (+468.77 points) to close at 51,671.03, comfortably sustaining its 51K baseline.

* Nasdaq Composite ($COMP): 🟢 +2.5% - +2.7% (Led the session as a cascading short-squeeze ignited high-beta technology and artificial intelligence lines).

⚡ Intermarket Drivers & Velocity Vectors

The Global Energy Collapse: International oil benchmarks capitulated, dealing a severe blow to sticky headline inflation models. Brent Crude plummeted 4.7% down to ~$83.25 per barrel, erasing the intense premium built up during the peak military friction window and returning energy overhead to early-March baselines.

SpaceX ($SPCX) Aftermarket Momentum: Following its massive public launch on Friday, SpaceX shares continued to push forward at midday. The successful deployment of its massive $75 billion capital raise against a staggering $1.8 trillion valuation acted as an idiosyncratic sentiment stabilizer, cleanly validating that deep institutional liquidity pools are ready to back generational infrastructure tech.

A Crucial Central Bank Transition: While equities celebrated the geopolitical truce, fixed-income desks began bracing for the highly critical June 16–17 FOMC meeting. This marks the official debut of newly appointed Federal Reserve Chairman Kevin Warsh.

Traders will look directly to his post-meeting statements, press conference, and updated dot-plots to determine if a cooling energy market will prompt a less restrictive path for near-term interest rate hikes.

The Strategy View: Absolute Trend Invalidation. Monday's tape completely reversed the structural anxieties triggered by last week's hot inflation print. The rapid unwinding of the geopolitical risk premium has fundamentally relaxed the cost of capital bounds before the Fed takes the stage tomorrow.

Maintaining core exposure across large-cap tech anchors and semiconductor lines remains the optimal blueprint as the broad market signals it wants to climb higher.

#MacroAudit #WallStreet #PeaceRally #OilCrash #SP500Breakout #SpaceX #FedChairWarsh #AryaFin

📊 Scion Asset Management Portfolio Update

Michael Burry, the contrarian manager of Scion Asset Management, disclosed that he has increased his long positions in a highly specific cluster of large, well-established businesses. Burry highlighted his investment thesis on his Substack, explaining that the broader market is heavily punishing dominant franchises with significant owner's earnings, minimal debt, and aggressive, accretive share buybacks.

According to Burry, these companies are experiencing deep valuation compression due to a massive concentration of capital into AI-adjacent names, creating distortions reminiscent of the 1999 dot-com bubble where non-internet stocks were left completely abandoned.

🔍 Deep Value Breakdown: The Four Key Additions

1. Adobe Inc. ($ADBE) 🏠The Valuation Dislocation: Down roughly 30% year-to-date, Adobe has been heavily targeted by short sellers due to extrapolated fears that generative AI competitors will disrupt its creative software monopoly.

Burry’s Core Thesis: He identifies $ADBE as a clear deep-value opportunity, explicitly pointing out that the company's gross margin rate is resting near all-time highs. The market is pricing in maximum-AI disruption scenarios that do not align with Adobe's fundamental software dominance or its actual free cash flow generation.

2. Alibaba Group ($BABA) 🇨🇳The Valuation Dislocation: Trading well off its historical highs due to Chinese regulatory adjustments, geopolitical trade pressures, and massive domestic e-commerce competition.

Burry’s Core Thesis: Burry heavily reframes the narrative, calling Alibaba "the most advanced company in China as far as AI strategy goes". He underlines that because management is aggressively buying back common stock, true intrinsic value continues to accrete to shareholders regardless of whether the short-term tape rewards it. He noted that "when the time comes, the stock will launch fast and fly high."

3. PayPal Holdings ($PYPL) 💳The Valuation Dislocation: Punished heavily over a multi-year window, down nearly 24% year-to-date due to a management turnover drag and intense payment processing headwinds from Apple Pay, Block, Stripe, and Adyen.

Burry’s Core Thesis: Burry describes the market as having "been attending PayPal’s wake for years now, though the body has yet to show". Trading at a highly compressed 7x to 8x earnings multiple, he notes that the asset is buying back stock "hand over fist" and represents a highly lucrative target for both private equity (PE) firms and strategic enterprise acquirers.

4. Veeva Systems ($VEEV) 🧪The Valuation Dislocation: Dropped nearly 29% year-to-date, hitting relative multi-year lows as localized biotech and pharmaceutical spending slowed into the credit reset.

Burry’s Core Thesis: He states that Veeva's core vertical SaaS architecture has returned to unjustifiably depressed price-to-earnings and price-to-sales ratios. He dismissed the looming competitive threat from Salesforce ($CRM) as only being relevant to a very small, isolated slice of Veeva's wider life-sciences software infrastructure.

The Strategy View: Burry is looking for structurally sound, high-cash-flow monopolies that have been completely orphaned because they aren't explicit AI hype plays. The broader the spectacle around mega-cap AI momentum swells, the wider the value discount gap grows for these compounding giants.