It’s Kevin Warsh Day. And first impressions matter.

We know that there will be a HOLD today, but three things we’re looking out for today:

--> The Statement & Dot Plot - Will the statement remove the easing bias? Probably so. The dot plot is more of a given; we’re likely to see more hawkishness. Then come the inflation, labor, and growth forecasts. I think inflation will change, labor steady, and growth steady - just my 2 cents. Watch the USD - higher for hawkish, weaker for dovish.

--> Fed Independence - We’ve had concerns about how independent Warsh will be from the White House, and whether he will buckle under pressure and lean dovish. I also wouldn’t want him to comment too much on the peace deal or the war, given that’s a more political standpoint.

--> Which Way Warsh Leans - Warsh has been known to be an inflation hawk, meaning he prioritized keeping inflation low, over labor market concerns. Over the last few months though he’s been talking about AI productivity gains allowing the economy to expand without overheating - so a more dovish view. Regardless, I don’t expect him to signal forthcoming hikes.

U.S. crude oil inventories fell by 8.3 million barrels as refinery utilization climbed to 96.7%. Petroleum demand remains solid, with total products supplied up 3.3% from a year ago, though gasoline demand continues to lag slightly behind last year's levels.

It’s Kevin Warsh Day. And first impressions matter.

We know that there will be a HOLD today, but three things we’re looking out for today:

--> The Statement & Dot Plot - Will the statement remove the easing bias? Probably so. The dot plot is more of a given; we’re likely to see more hawkishness. Then come the inflation, labor, and growth forecasts. I think inflation will change, labor steady, and growth steady - just my 2 cents. Watch the USD - higher for hawkish, weaker for dovish.

--> Fed Independence - We’ve had concerns about how independent Warsh will be from the White House, and whether he will buckle under pressure and lean dovish. I also wouldn’t want him to comment too much on the peace deal or the war, given that’s a more political standpoint.

--> Which Way Warsh Leans - Warsh has been known to be an inflation hawk, meaning he prioritized keeping inflation low, over labor market concerns. Over the last few months though he’s been talking about AI productivity gains allowing the economy to expand without overheating - so a more dovish view. Regardless, I don’t expect him to signal forthcoming hikes.

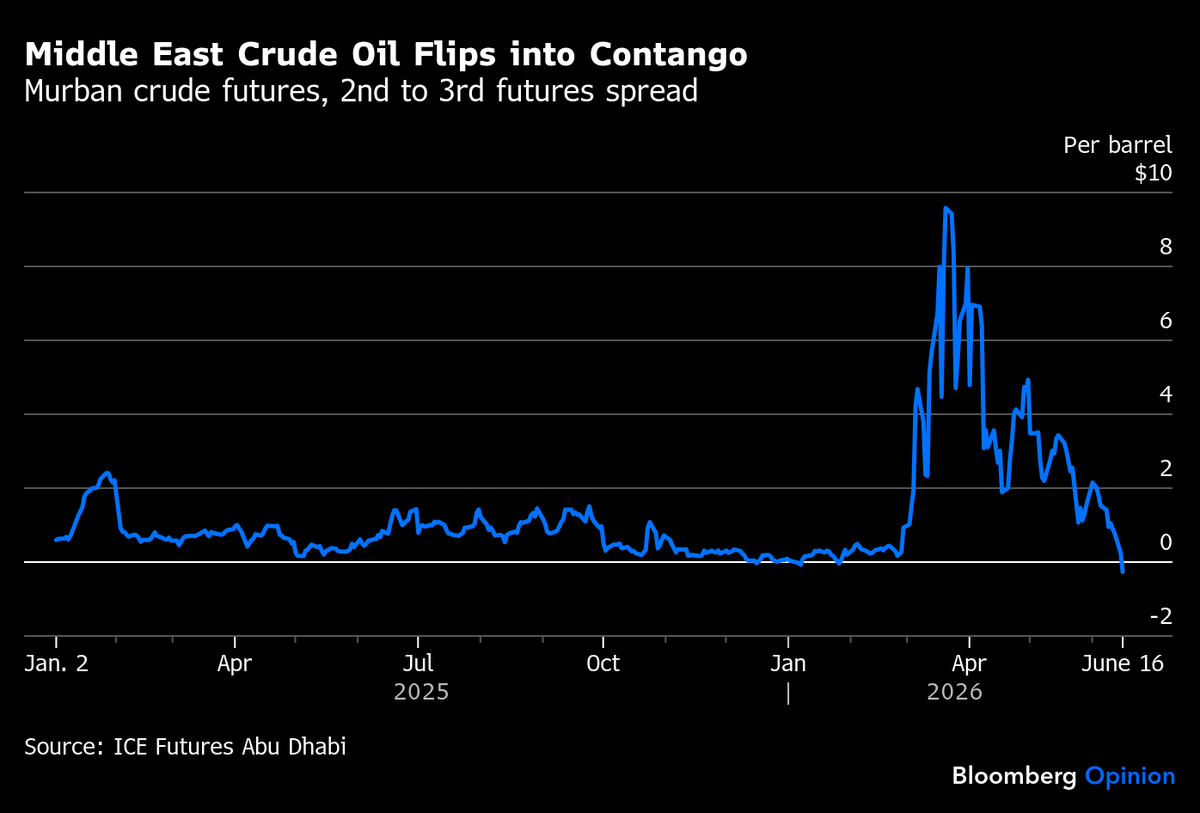

CHART OF THE DAY: What goes into backwardation, can go into contango.

The time spreads of some key Middle Eastern crude grades have collapsed. Murban from UAE is now in contago, even before Hormuz formally re-opens with the signing of the deal, scheduled for Friday.

We've now started talking about token economics

GS predicts that token consumption could increase 24x today's estimated global capacity

As the use of agents become more widespread, the demand will be driver by enterprise and consumer agents, compared to non-agent workloads

The BOJ delivered the widely expected 25 basis point hike to 1%, the highest policy rate Japan has seen since 1995.

The bank confirmed it will halt the tapering of its government bond purchases in April 2027, letting monthly flows settle at ¥2 trillion. We flagged this QT freeze as a signaling mistake, and the market's initial reaction looked like a reprieve. Equities briefly crossed 70,000 and the Yen traded flat. But the underlying message is dovish, and I think markets will eventually price that in.

The BOJ has explicitly left the door open to step back in with asset purchases if yields rise too quickly. That's not a hawkish hike. That's a hike with a safety net attached, and the safety net changes the signal entirely.

The whole issue was defending the Yen, so none of this helps that cause.

Compounding this is a leadership problem we can't ignore. Governor Ueda is hospitalized. Deputy Governor Himino chaired the vote. Deputy Governor Uchida handled the press conference alone. That's a broken chain of command at exactly the moment when clear, unambiguous guidance is most needed to put a floor under the Yen.

For global investors, the synchronized central bank era is over. The Fed is holding with a hawkish tilt. The BOJ is hiking while keeping the balance sheet on pause.

The risk-reward on Japanese equities is iffy here. Monetary transmission is slow, which means the friction between a nominal rate hike and a frozen normalization path will show up in markets before policymakers acknowledge it. Watch for volatility compression to unwind across global macro desks as this divergence becomes impossible to ignore.

Hey friends!

Curious what's going on in these markets?

Want to learn more about order flow and how it can help you define risk intraday?

We're going live with this week's episode of Back to the Futures!

Tune in.

https://t.co/OaJ2D7dpzU

Hey friends,

Join me today at 1:30 pm ET as I analyze what's going on with these increasingly volatile markets.

We'll talk about what's going on with sentiment, flows and positioning.

Then we'll shift over to opportunities and risks.

Back to the Futures returns . . . 🦾

In a surprise move ahead of its scheduled June 17-18 policy review, Bank Indonesia raised its benchmark BI-Rate by 25 basis points to 5.5% on Tuesday.

This follows a larger-than-expected 50 basis point hike in May.