Testing a longer-form research format away from the usual slide decks on bio-data for model training. Putting some highlights in the thread.

https://t.co/CRfbL74nyo

@AppleHelix is it corporate strategy or marketing strategy? I would argue rxrx is retail-forward and gets rewarded with a better valuation while sdgr is perceived as boring legacy-saas

both businesses arguably have very similar corporate strategies and have pivoted to asset development

underrated point of the ajax story is that schrodinger owned a sizable equity stake - as with structure therapeutics (3.2B), Morphic (acquired 3.2B), among others...

If they were a VC fund they would be taking victory laps, unfortunately they're a SaaS business...

Eli Lilly continued its recent buying spree, agreeing to pay up to $2.3 billion for Ajax Therapeutics in a deal that bolsters the drugmaker’s blood-cancer portfolio. https://t.co/0G3YkcilV8

@two_natural lots of people chasing this opportunity so you would have to assume so, there are preclinical "techbio" competitors like Recursion and Genesis Therapeutics going after the same target as well

TL;DR

AI performance is tied to scaling laws, which means more data going in, hence, "data problems". The next wave of value creation will be tied to new sources of data that explore new biological space. But the issue is that this data isn't readily available for the industry.

Testing a longer-form research format away from the usual slide decks on bio-data for model training. Putting some highlights in the thread.

https://t.co/CRfbL74nyo

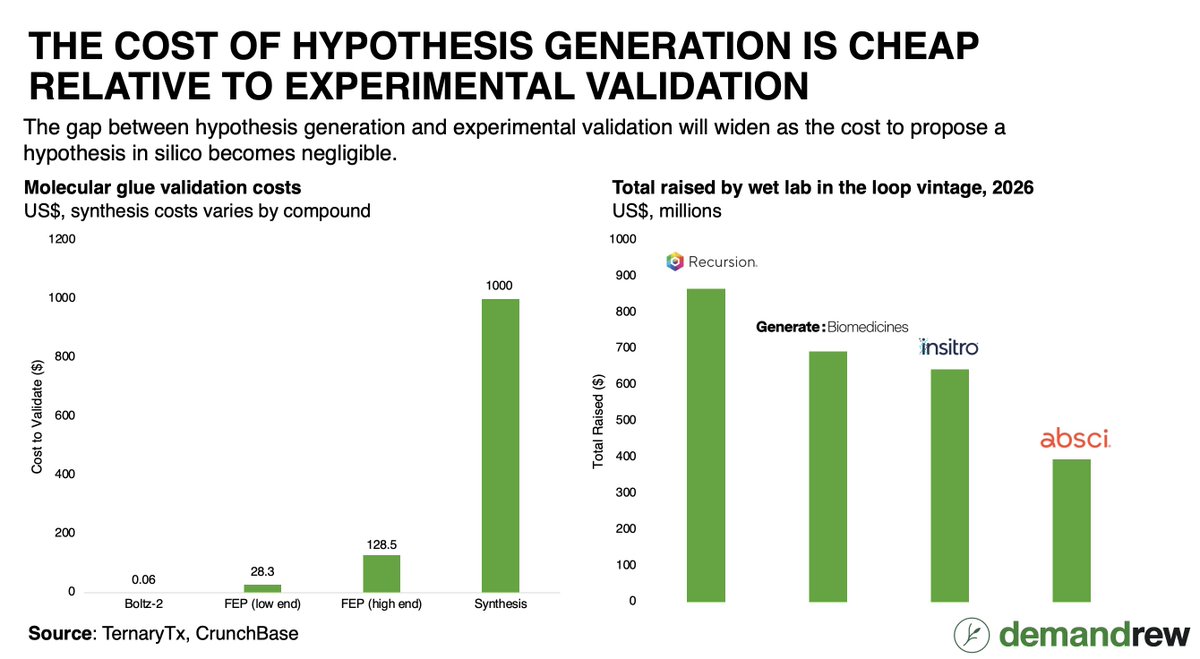

8/ Scaling generative models drives the cost of hypothesis generation to zero. However, the key is still wet lab validation. The gap between hypothesis generation and wet lab validation creates "speculation debt" that still needs to be bridged