Ways and Means Republicans rolled out six standalone bills and a discussion draft ahead of today’s crypto tax hearing at 2pm ET.

The bills address crypto donations, mining and staking taxation, reporting requirements, tax treatment parity, voluntary disclosure, and applying existing tax anti-abuse rules to digital assets. The discussion draft targets the use of offshore crypto tax shelters.

Witnesses include:

📌Sarah Reilly, Vice President and Senior Tax Counsel, @Fidelity

📌@LawrenceZlatkin, Vice President of Tax, @coinbase

📌@jasonsomensatto, Director of Policy, @coincenter

📌Mike Kaercher, Deputy Director,

Tax Law Center at @nyulaw

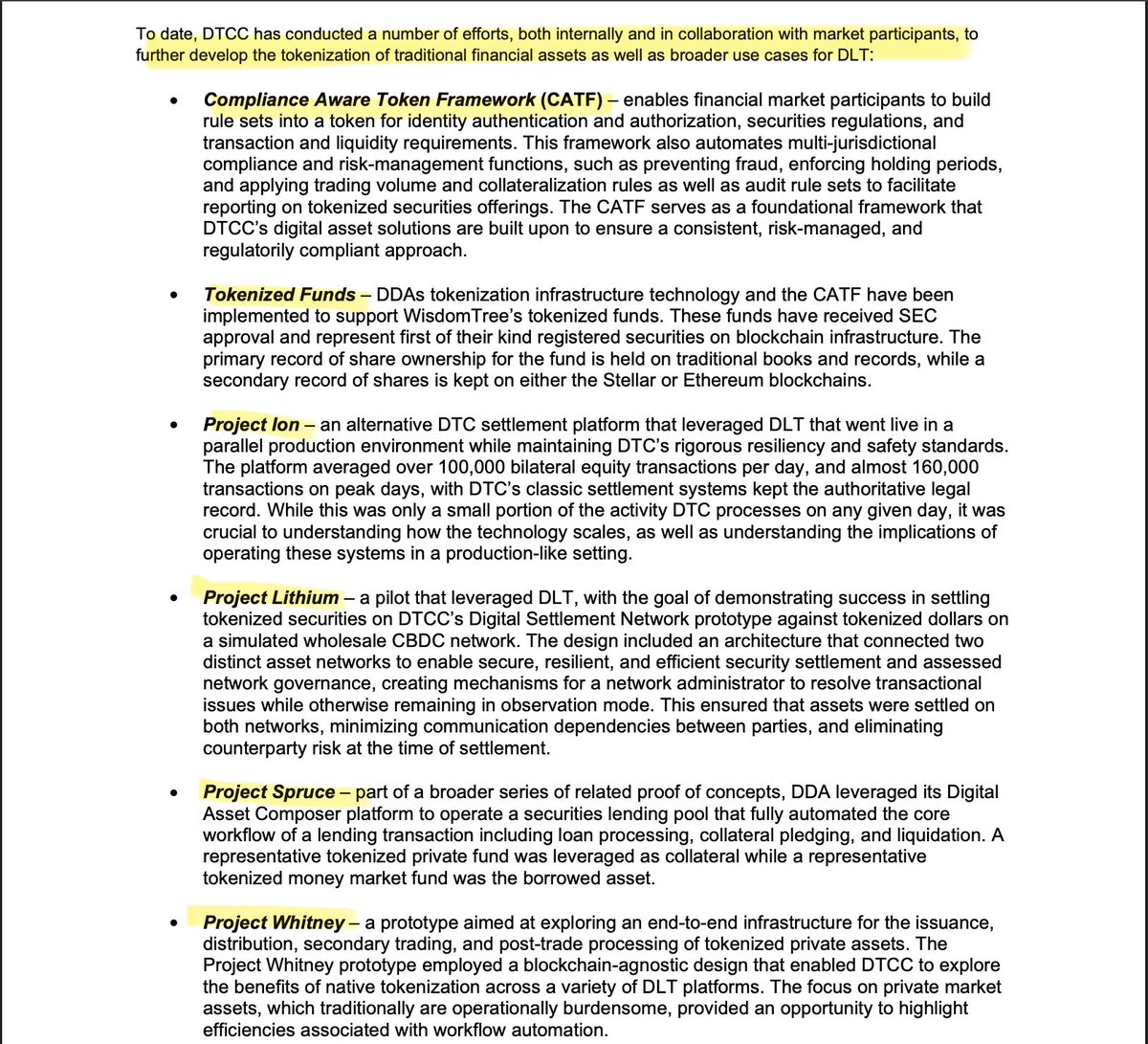

The DTCC has been deeply engaged in the blockchain space since 2016.🙇♂️

Project Ion.

Project Lithium.

Project Spruce.

Years of rigorous testing and continuous experimentation.⏳

Moments of mistakes, periods of delay, and countless lessons learned.💯

All of it leading to this pivotal year.🎯

It will seem like an overnight success.😶🌫️

However, the DTCC’s tokenization launch in July will be the culmination of years of hard work and preparation.

Documented.📝👇

Why does real-world utility actually matter?

Because crypto that only lives on exchanges doesn’t help everyday people or businesses.

VELO brings real utility: compliant payments, instant off-ramps to local currency, fast settlement for merchants, and rewards on your money while it moves.

It solves actual problems like slow transfers and idle cash sitting in banks.

This is crypto that works in the real world.

🇺🇸 JUST IN: WHITE HOUSE TO HOST HIGH-STAKES TALKS ON THE CLARITY ACT

White House officials will meet with law enforcement groups on Wednesday to resolve concerns that key provisions of the Clarity Act could weaken efforts to combat illicit finance, per Eleanor Terrett.

Guys… Time is running out. Those who bought in early and held on will live the life of their dreams.

No, it’s not a fantasy. It’s reality.

XRP will be the foundation of the new financial system.

Probably nothing..

Brinc and @Ripple have launched the Hong Kong Financial Innovation Program, a first-of-its-kind accelerator powered by none other than $XRP Ledger, designed to reshape the future of finance in Asia 🌐

Ripple are also a member of HKMA Project BLOOM 🇭🇰

DTCC: 30 days from now

Not a POC

Not Stellar

Not XRPL

This is the @CantonNetwork infra with some new working partners and new types of trades.

👉📺https://t.co/MHzPePPxDm

#CC

I’m done with YouTube’s censored, controlled narrative machine.

The real unfiltered truth, the dark connections, the hidden mechanics, the raw geopolitical and financial warfare most creators are too scared to touch, is now exclusive on Substack.

https://t.co/1uZUa0bOSu

Ripple successfully secured both an Electronic Money Institution (EMI) license and Cryptoasset Registration from the UK’s Financial Conduct Authority (FCA).

These authorizations enable Ripple Markets UK Ltd. to scale its end-to-end cross-border payments infrastructure and offer regulated e-money and digital asset services to institutional clients across the United Kingdom.

Ripple isn't just testing the XRPL lending protocol they're using formal verification (math-based proofs) to hunt bugs that normal testing can't even see 👀

Working with Common Prefix to stress-test XLS-66 & XLS-65 before Mainnet. Because one flaw in L1 core code = every app built on it is affected.

"Traditional testing isn't enough when you're building DeFi directly into Layer-1. Ripple engineer Vito Tumas

RIPPLE'S BANKING PARTNER JUST WENT CRYPTO-NATIVE 🚨

🇯🇵 SBI Shinsei Bank 4.33M accounts now rewarding depositors with BTC, ETH & $XRP vouchers on top of regular yen interest

🚨 KNOW: Japan's SBI Shinsei Bank Will Let Customers Turn Their Deposit Interest Into $XRP, With The Pilot Launching June 10. 🇯🇵

In Simple Words:

Normally, when you keep money in a bank, you earn a small interest payment in cash. SBI Shinsei Bank is changing that.

Customers can now choose to receive a portion of their interest as actual crypto, including $XRP, instead of yen.

How It Works

→ Customers earn interest on their yen deposits as usual

→ They can convert roughly 20% of that interest into crypto vouchers

→ Those vouchers can be redeemed for Bitcoin, Ethereum, or $XRP

→ The conversion uses live market rates at the time of redemption

→ The pilot begins June 10, with full rollout planned for autumn 2026

Why This Matters

→ SBI is one of Japan's most powerful financial conglomerates and Ripple's longest-standing partner since 2012

→ This makes $XRP a built-in reward inside mainstream Japanese banking, not a separate crypto app

→ Millions of everyday savers get exposure to $XRP simply by keeping money in the bank

→ It builds directly on SBI's Hyper Deposit product and the upcoming RLUSD launch in Japan

SBI isn't just offering crypto. SBI is wiring $XRP directly into the act of saving money.

Follow @RippleXity for the deep links nobody else is connecting in the $XRP ecosystem.

BANK OF AMERICA IS LAUNCHING CROSS-BORDER PAYMENTS VIA SWIFT. 👇

Most people will see that headline and think it has nothing to do with $XRP.

That is where they miss the bigger picture.

Bank of America is not some random bank in Ripple’s orbit. It has been listed as a RippleNet member. It has sat on Ripple’s Governance Committee. That means institutional-level involvement, not a casual partnership mention.

Now add this.

A February 2026 SEC filing showed Bank of America holding around 13,000 shares of the Volatility Shares XRP ETF.

So the same bank expanding SWIFT cross-border payment services already has regulated XRP exposure and existing Ripple ties.

Connect the dots.

Banks are not choosing between SWIFT and Ripple.

They are running both lanes at the same time.

SWIFT gives banks global messaging reach across 11,000+ institutions.

RippleNet gives them blockchain-based settlement and on-demand liquidity through XRP where speed, cost, and capital efficiency matter.

That is the hybrid model.

Use SWIFT where it makes sense.

Use Ripple rails where settlement needs to be faster, cheaper, and more efficient.

This is why Bank of America expanding cross-border payments through SWIFT does not kill the XRP case.

It may actually expand the highway XRP can later move through.

The bank already has Ripple connections.

The bank already has XRP ETF exposure.

The bank already sits close to Ripple’s institutional payment network.

Now it is expanding global payment corridors.

That is not bearish for $XRP.

That is infrastructure getting wider before the settlement layer gets fully used.