$ORCL Q4 EARNINGS

• Revenue $19.2B vs Est. $19.1B

• EPS $2.11 vs Est. $1.97

• Operating Income $8.6B vs Est. $8.3B

• RPOs $638B vs Est. $590B (+363% YoY)

FY28 Guidance

• Revenue $90B vs Est. $89B

• EPS $8.05 vs Est. $7.45

Oracle announced a $40B financing plan.

How many of you are interested in learning how to use my Opening Range Breakout (ORB) day trading strategy?

How many of you are interested in learning how to use my 9ema day trading strategy?

Drop a ❤️ if either of those interest you

I'll be live trading on YouTube in 1 hour

I plan to discuss the overall market, day trading setups, swing trading setups, trade planning, & execution

I'd appreciate it if you checked it out. Here's the link👇

https://t.co/sTEenbUoYO

🔥RSVP for tomorrow's show here.

🎙️Please join us!

🗓️Thurs. June 11th

⏰8-10 PM CST

🌹Hostess: Spunky @SpunkyPatriot_ 🟣Co-Host: Brent @BFHAMMER1

🗣️Topics: Various with Open 🎙️

https://t.co/cvurRZQsXH

⚠️ Schedule Update ☔️

The DIRTcar Summer Nationals events @KankakeeSpdwy + @PeoriaSpeedway are postponed due to heavy rain through the week and more projected.

Kankakee rescheduled for July 6. Poplar Bluff is canceled for June 22; Peoria fills that date. https://t.co/8k1BeCBFMn

🚨Cody Overton back in a super late model🚨

Overton will pilot a second car out of the James Trantina III and Triple B Motorsports Team stable. It's a Longhorn with a Clements.

The team will make its debut with the World of Outlaws when they head north to Ogilvie on Monday, June 22nd.

$DDOG just got a wave of validation from Wall Street.

Piper Sandler, Canaccord, and Barclays all raised price targets after Datadog's DASH conference, citing growing adoption of its AI-powered observability platform and autonomous agent capabilities.

The key takeaway isn't the price target hikes. It's that Datadog is evolving from a monitoring platform into an AI operations platform.

Management highlighted explosive growth in Bits AI usage, rising AI observability demand, and increasing customer adoption of autonomous remediation tools. That's exactly the type of product expansion institutions want to see.

The stock has already been a leader, but this news reinforces the bull case: AI isn't just creating demand for chips and infrastructure, it's creating demand for software that helps enterprises manage increasingly complex AI environments.

When multiple firms raise targets on the same catalyst, I pay attention.

$275 is now the new high-water mark on the Street. The trend remains intact.

$SJM quietly had one of the stronger post-earnings reactions in consumer staples this week.

After reporting better-than-expected results and offering a solid FY27 outlook, analysts are starting to move targets higher:

• Morgan Stanley: $110 → $110 target, Equal Weight

• Stifel: $100 → $115 target, Hold

• BofA: $130 → $132 target, Buy

The important part isn't the target changes.

It's that multiple firms highlighted the same themes:

✅ Better-than-feared FY27 outlook

✅ Lower cost pressure

✅ Improving balance sheet

✅ Stronger earnings power than expected

The stock already responded with a ~10% move, so chasing isn't the game here.

What I'm watching now is whether institutions continue to accumulate shares after the earnings gap. If $SJM can hold these gains and build a new base, this could become more than just a defensive staples trade.

For now, the message from Wall Street is clear:

The earnings story improved, and analysts are being forced to adjust higher. The question is whether the stock can turn this earnings gap into a sustained trend.

$HNGE just reminded the market why strong growth stories get expensive.

This wasn't just a guidance raise. This was a company materially increasing both quarterly and full-year expectations while already growing at an impressive pace.

The highlights:

• Q2 revenue guidance raised to $200M-$202M vs. $195M consensus

• FY26 revenue guidance raised to $818M-$824M vs. $802M consensus

• Q2 revenue expected to grow 45% YoY

• FY26 revenue expected to grow 40% YoY

• Operating margins continue expanding

• Stifel raised its price target from $67 to $79 and maintained a Buy rating

What stands out to me is that this isn't growth at any cost. They're growing rapidly while simultaneously generating meaningful operating leverage. That's the combination institutions love to see.

The market has been rewarding companies that can prove three things:

1. Growth is accelerating.

2. Margins are expanding.

3. Guidance keeps moving higher.

Hinge Health just checked all three boxes.

The stock may be extended in the short term after the news, but from a fundamental perspective, this is exactly the type of update that can keep institutions accumulating shares over time.

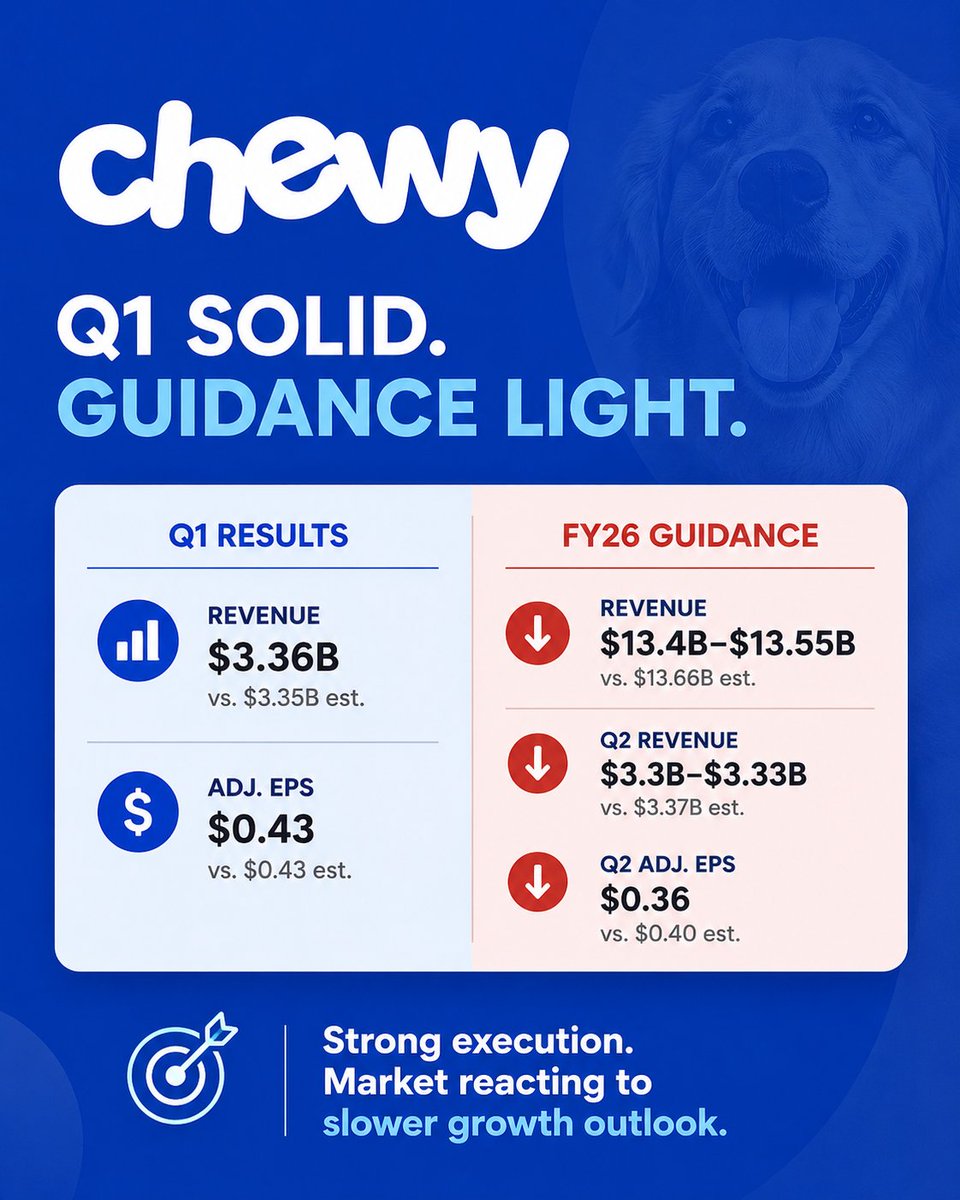

$CHWY delivered a solid quarter, but guidance is what has traders focused this morning.

Q1 revenue came in at $3.36B vs. $3.35B expected, while EPS matched estimates at $0.43. The business continues to execute well, adding customers, expanding margins, and generating strong cash flow.

The catch? Forward guidance was a little light. Management sees FY26 revenue of $13.4B-$13.55B, below the Street's $13.66B estimate, and Q2 revenue and EPS also came in slightly under consensus.

This wasn't a bad report. In fact, operationally it was strong. The market is simply adjusting to slower growth expectations after a big run. The key question now is whether institutions focus on the guidance miss, or the fact that Chewy continues to take share and improve profitability.

Watch the reaction, not the headline. Price pays. Narrative follows.