BofA Reiterates $AAPL Buy Rating, PT $325

Analyst comments: "We remain bullish on shares of Apple heading into 2026 given (1) iPhone upgrades are tracking better than expected (globally including China) with record upgraders, (2) gross margins continue to move higher despite commodity headwinds, (3) AI-enabled Siri will be available in 2026, (4) a foldable iPhone is expected in Sep 2026, and (5) a new record installed base of 2.5bn devices to drive continued double-digit growth in Services. In our Oct 29 note, we laid out our 5-year expectations for Apple's rev/earnings power where EPS could grow in the mid-teens through C2030E. We reiterate Buy on strong capital returns, an eventual winner on AI at the edge, and optionality from new products/markets."

Analyst: Wamsi Mohan

BofA Reiterates Buy on $ASML, PT $1672; Top Pick

Analyst comments: "Yesterday, we hosted Erik Hosler, former Chief Technology Officer and Founder at xLight Inc. Following the discussion, we continue to view China as a limited competitive risk and see emerging inflection points tied to the industry shift toward edge AI. We reiterate our Buy/Top Pick for ASML at PO €1,454/$1,672 on 31.0x CY27E EV/EBITDA.

China’s domestic EUV push is advancing but remains a limited competitive threat to ASML, with capabilities still several years behind.

A key structural disadvantage is China’s lack of global integration and deep customer collaboration, which underpins ASML’s technology leadership. Leading fabs (e.g., TSMC, Intel) are unlikely to adopt unproven Chinese EUV tools, while domestic players (e.g., SMIC, CXMT) will likely continue to purchase ASML immersion and local EUV systems in parallel. China may gain some traction in emerging markets through discounted pricing."

Analyst: Didier Scemama

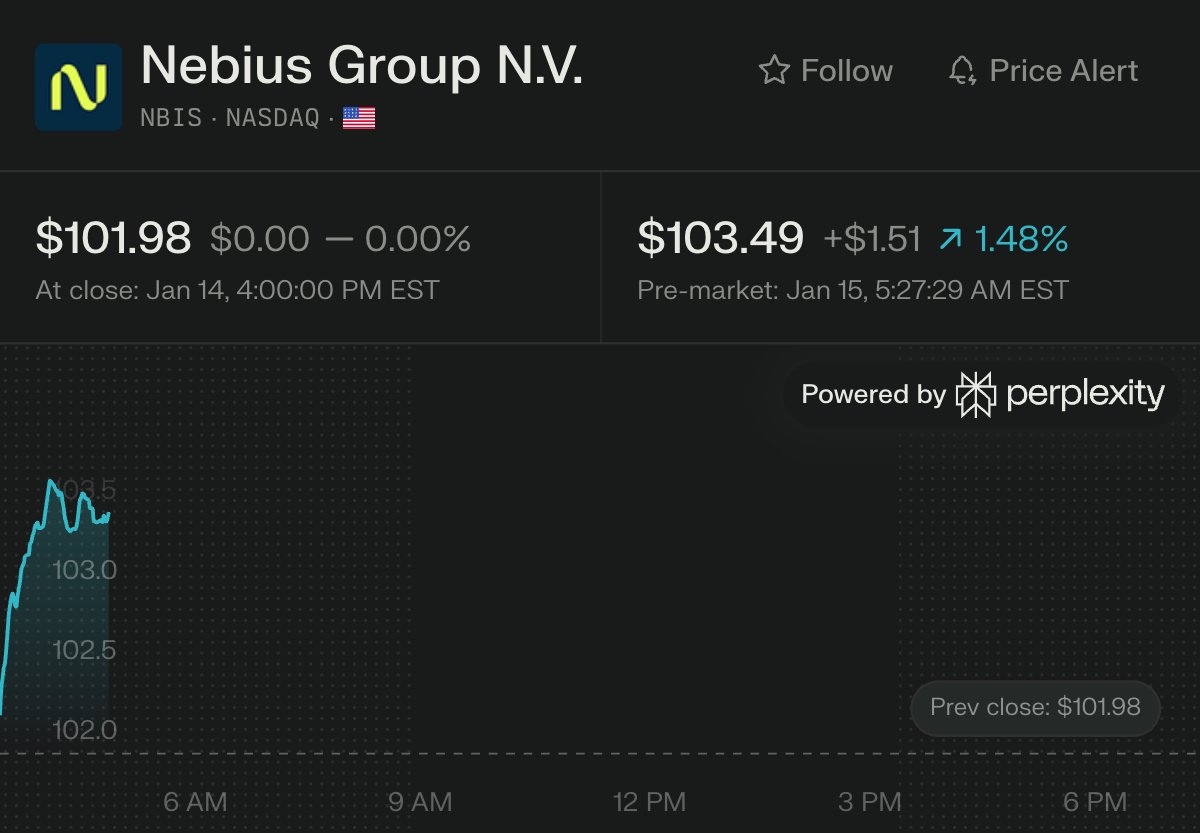

Morgan Stanley Initiates Coverage on $NBIS with Equalweight Rating, PT $126

Analyst comments: "Nebius' broader software platform and managed services, diversity of customer base, positioning to gain share of new AI infrastructure demand, as well as non-core consolidated businesses and investments with valuable equity stakes, all contribute to Nebius Group's value beyond its existing footprint of AI compute. We see Nebius well positioned to bring online significant capacity, scale rapidly, and long-term, we think Nebius can inflect margins and FCF meaningfully positive. Near-term, ramping depreciation (4-year useful life) weighs on margins, with FCF significantly negative given capex spend required to deliver 2.5 GW worth of AI infrastructure (company's end of 2026 contracted power target) in the coming years. With this ambition and a $7-9 billion 4Q26 ARR target, which we view as optimistic, we question what does Nebius need to do to outperform expectations? EBIT remains pressured in coming years given ramping depreciation, requiring investors to look to EBITDA or longer-term metrics for valuation. Initiate at Equal-weight."

Analyst: Josh Baer