Not investment advice.May have position in names mentioned.Opinions expressed strictly my own,not representative of my employer.Factcheck urself.RT≠endorsement

$KRYS

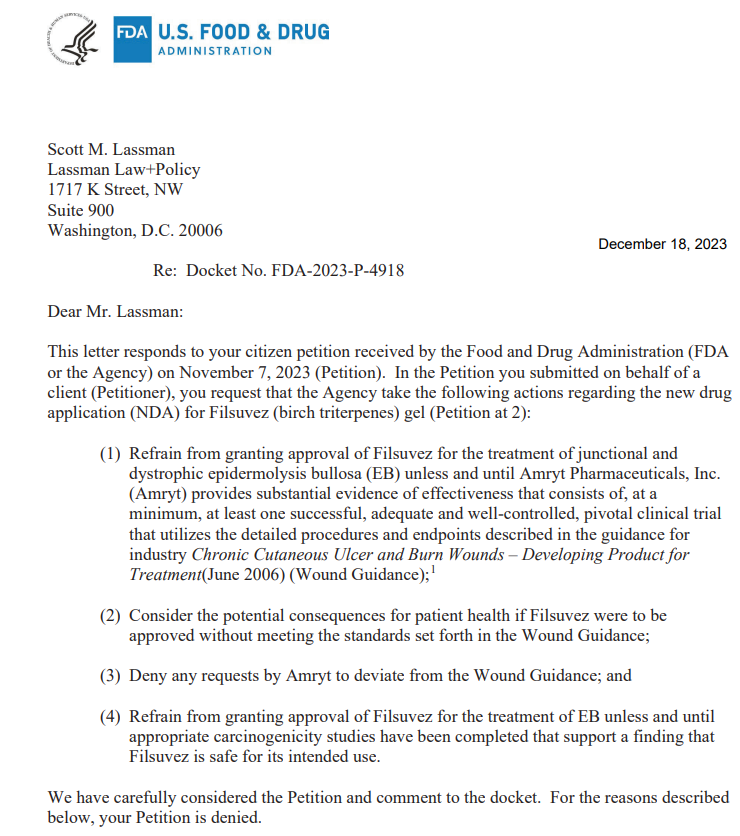

citizen petition to prevent Chiesi's Filsuvez approval denied.

Filsuvez approved yday with broad label for DEB and JEB, no HCP required.

Will be interesting to see how this tiny market gets split between Chiesi $KRYS and potentially $ABEO

Stock will do what it will do, but this $KRYS Vyjuvek launch is objectively one of the most underwhelming ones I’ve seen, for a disease clearly as severe as DEB is

Only 284 *start forms*, ~18 weeks since approval. 121 in q2 and so 163 in q3 by my math . Comp to likes of RETA Skyclarys which had 500 start forms BEFORE the drug was approved. Arguably a more questionable efficacy profile with skyckarys notwithstanding. Or ACAD Daybue, which has 800 patients ON the drug already, approved only ~1 month before KRYS Vyjuvek

Can’t imagine any parent won’t be rushing to fill out a simple ~2 minute start form while their kid’s skin is practically melting off and how unfortunately tortuous DEB is. Is the population smaller than what was imagined or is there something else going on?

https://t.co/Omyc1u1UDW

$ARGX announces fail in PV

BP under review given comparable biology

Illustrative note from Cowen 2024 best ideas list gives perspective on sellside model % of Vyvgart peak sales from these indications (~30%+)

Chiesi mamaged to get $AMYT's Filsuvez approved in the US in 2 types of EB

Chiesi Global Rare Diseases Receives FDA Approval for FILSUVEZ (birch triterpenes) topical gel for the Treatment of Epidermolysis Bullosa https://t.co/2kKrbtsk1y

APGE and SYRE both sub- $1B, pursuing much better commercial/deal value validated indications.

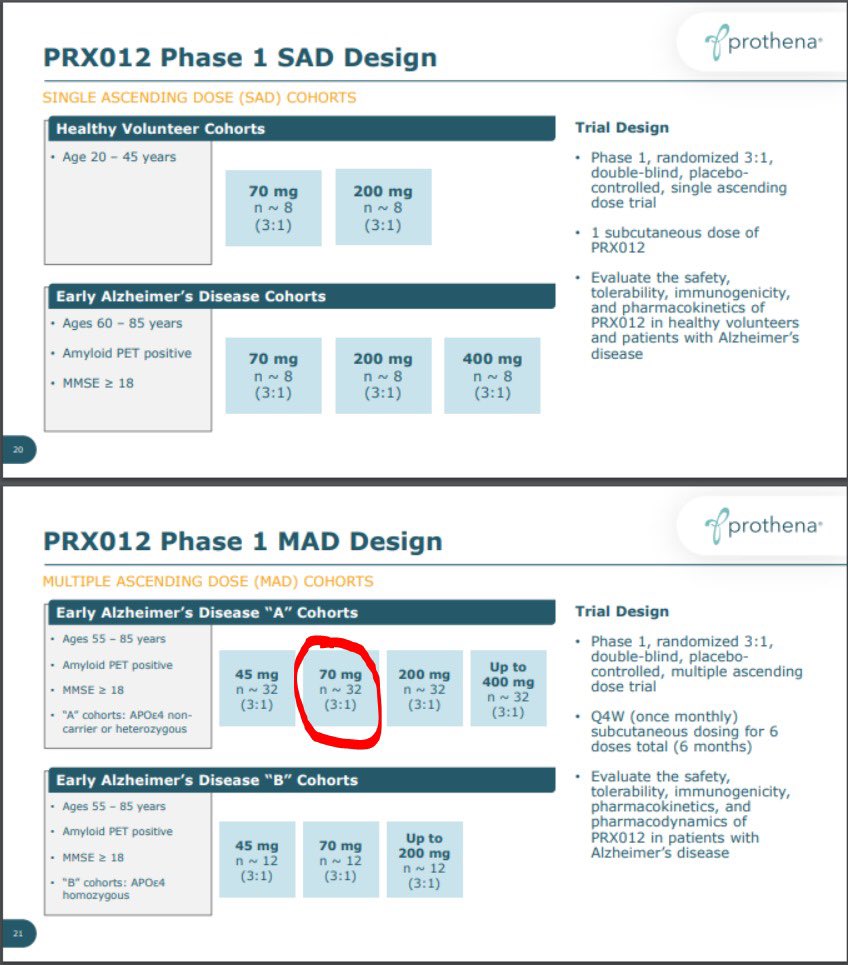

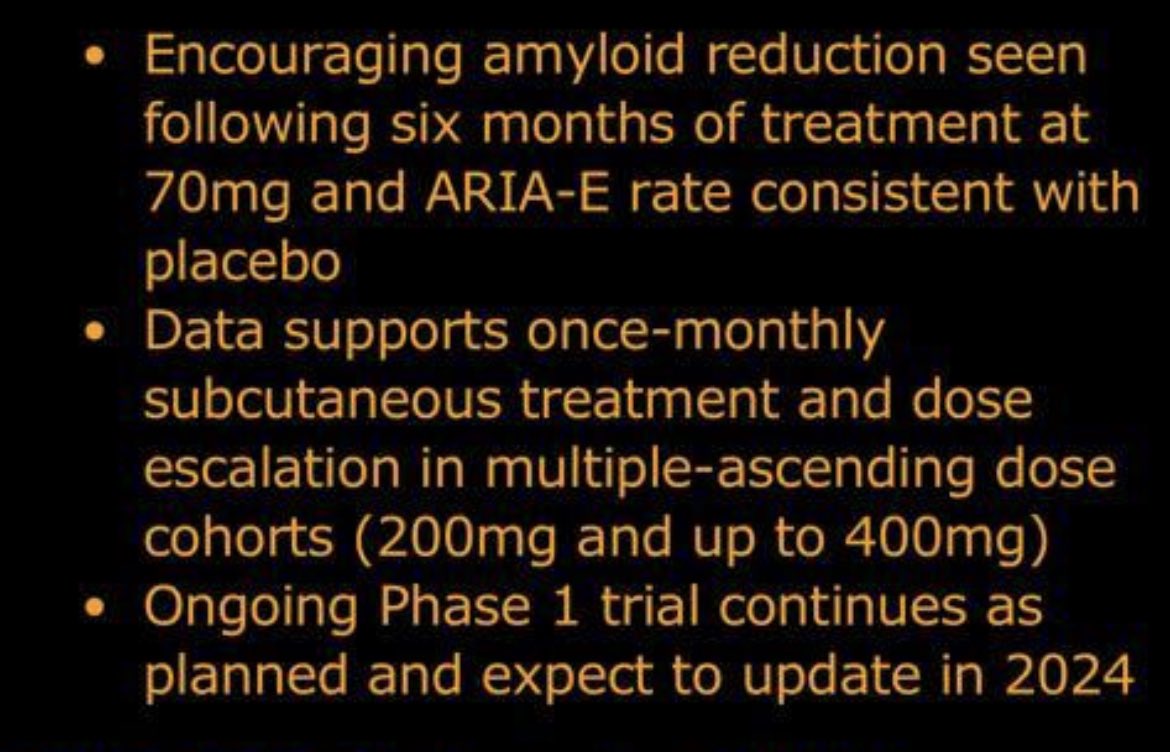

PRTA already at $2B, Alz market crowded with assets in development and commercial ones underwhelmed thus far.

HAE market probably the closest (still generous) analog for assets trying to differentiate on convenience, ATXS would be the analogous (pre data and ~5 years from commercial) comp, ~$300m cap. KALV PHVS combined have ~$1.5B cap post data

Stock will do what stock will do in this tape, but not sure the comps make the case for being undervalued.

HaploBMT with posttransplant cyclophosphamide for sickle cell disease.

Bombs dropped against gene therapy during late breaking #ASH23 and during QnA.

Access and affordability is key!

I was wrong. The 50mg, 100mg BID and 200mg all have HbA1c reductions of 0.4-0.5%. This calls into question the 100mg data, and likely means the drug isn’t doing anything

https://t.co/xqqzCurXzu

Digging into the $BMEA data. On first pass I agree with the general view coming out of ADA that the data are quite remarkable, with the durability of a short course of therapy and off-treatment effect pretty much unheard of for the commercial diabetes drugs, which of course are monster commercial blockbusters. Obviously early and I’ll have more once I dig further, but there’s not too many new, potentially disease modifying smid plays in diabetes.

Any credible critiques of the data, now that the old bear concerns (safety, durability, rbc and Hb effects) have been quietened? Genuinely curious.

$REPL with the unique achievement of a worse disease control rate (OR + SD) for the RP1 combo vs the control arm.

Implications for survival, in case anyone is still holding out hope

Sounds about right.

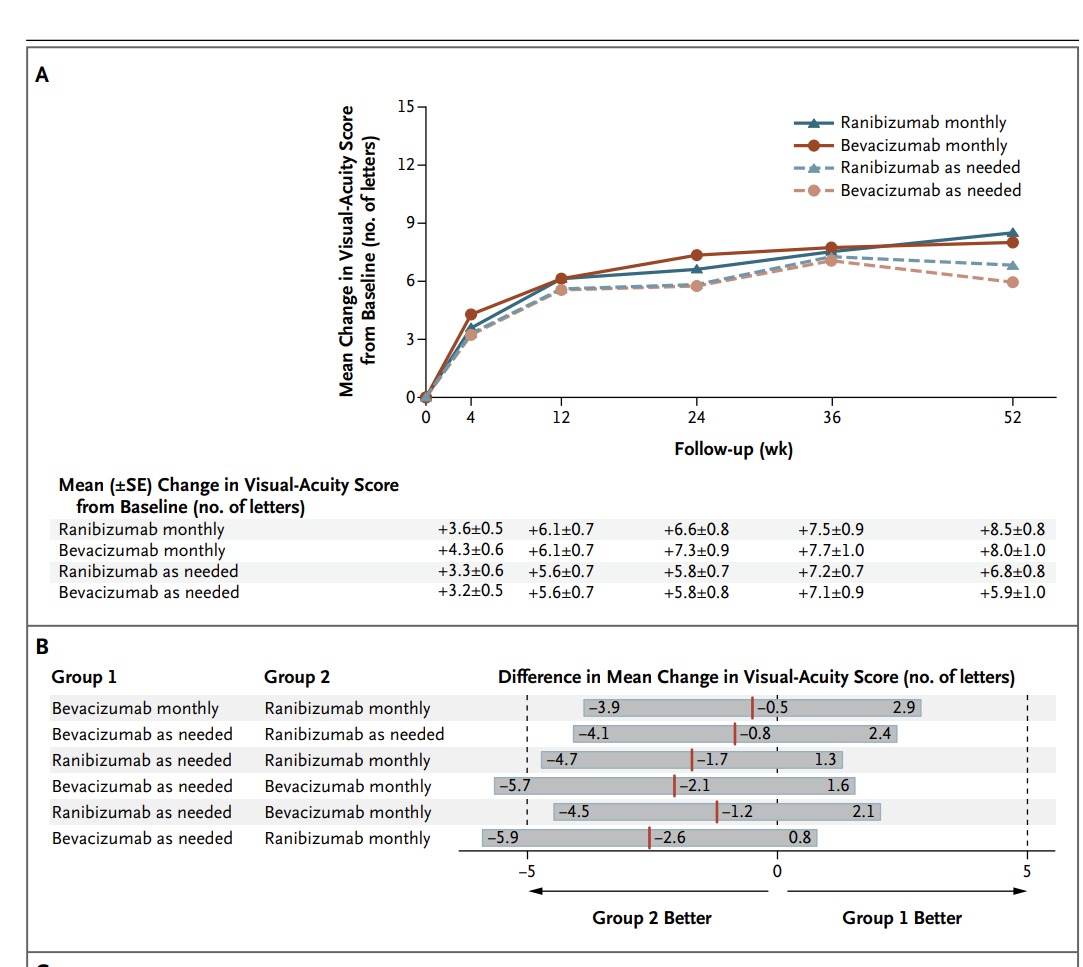

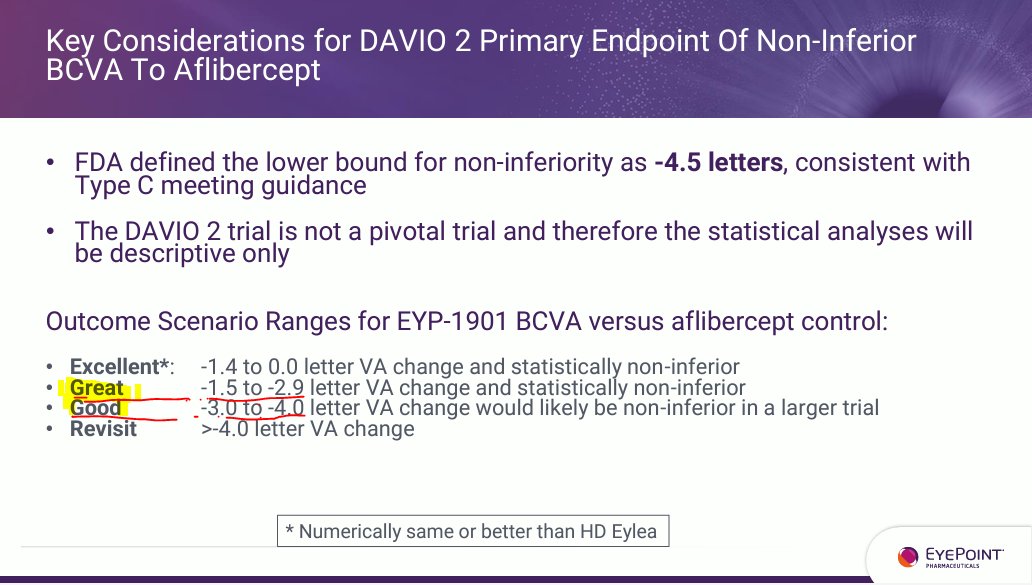

Lower bound for non-inferiority is -4.5 letters.

Looking at typical wAMD Ph3 trials below, ~300 patients per arm (KOD recent trial similar n), a 1-1.5 letter difference already gets the lower bound CI to ~4.5+.

So if $EYPT shows up in a ph2 with 2 letters or greater difference then logic would dictate they'd have to run massive ph3s to hit non-inferiority. Not to mention the typical degradation of effect from ph2 to ph3.

Not sure how they are characterizing -1.5 to -2.9 letters as a "great" outcome given this fact pattern which argues the exact opposite