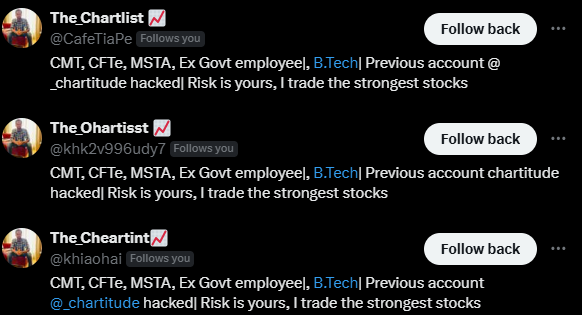

Just today I was searching for @thechartist26 and started following his account and within a couple of hours I got follow from 3 accounts impersonating @thechartist26.

I think these people are tracking chartist's account more than he himself does.

- Input cost inflation and geopolitical issues may stress gross margins in Q2. Recovery is expected in Q3 and Q4.

- The company is aiming for steady growth in the double-digit to low-teens range.

- EBITDA margins to remain in the low-to-mid 20s range.

Q1FY27 #BOM#bankofmaharashtra

1. Managed to beat their guidance on most fronts.

2. NIM - 3.85%

3. ROA 1.9% ROE 24.65%

4. Advances grew by 27% against the guidance of 18%

5. Deposits grew by 13%

6. Segemental Growth

- Retail 25%

- Agri 30%

- MSME 23%

- Corporate 30%

11. Maharashtra Debt Waiver:

- Scheme is still under formulation

- 3,500 crores is eligible accounts

- Outstanding exposure in the books 3,200 crores

- Gov receivables 2700Cr & 260Cr from Farmers

- Max haircut expected 450-500Cr

- 1700Cr already provisioned

#apollomicro#premierexplosive

1. Apollo Micro secured 41% stake in Premier Explosives for 1500Cr

2. Transaction expected to close by Dec-26.

3. Premier Explosive OB = 1500Cr and expecting to execute at least half of it in FY27.

No recomm

https://t.co/exNu6QLIKZ

8. Reasonable revenue contribution from new facility expected from FY28 and margin expansion expected from FY29.

9. Can grow 40% in FY27 & FY28 as well. EBITDA margins would be similar range.

Disc: No buy sell recomm.

https://t.co/QCwNvPRkQE

Yash Highvoltage #yashhigh

1. Company raising 151Cr through the combination of pref+warrants.

2. This will go towards the brownfield+greenfield capex that the company is doing.

3. Total capex would be 200Cr and asset turns would be in the range of 4 to 5.

4. The company is thus expecting additional 800 to 1000Cr from this capex.

5. The company had plans for 245Kv class but now planning to go till 550Kv.

6. Clients usually prefer vendors with complete range

7. Opens up global markets & improves the margins.

In Q4FY26 concall, management indicated that - Reported EBITDA is about 1.1x the run-rate EBITDA.

https://t.co/kzKTwN37Xd

Disc: No buy sell recommendation

6. Company has 35% of market share of the hyperscalers contracts in India.

7. Of 1.5GW expected to be put up in FY27, ~40% is for data & AI.

8. Guidance of total capacity to be ~4.5GW by FY28.

9. Run Rate EBITDA at start of FY27 was 1870Cr and by the end of FY27 it could be 3000

#cleanmax

1. FY27 guidance of 1.5GW capacity addition.

2. The company already added 500MW+

3. On track to beat the guidance.

4. Pipeline of 2600MW of which 42% is for AI DC.

5. For 1GW of DC needs 9K to 10K renewable energy, approx 40K Cr of renewable capex

4. FOC and connectivity solutions OB = 15000Cr. Expecting significant amount of orders from US.

5. Brownfield expansion at existing facilities for FOC.

6. New facility for preform.

7. Total capex would be around 950Cr

https://t.co/7KVwJ77xEZ

#HFCL

1. Aims to be a one stop solution for AI DC, by not just supplying FOC but also passive connectivity equipment called as data center interconnect.

2. 70% of the revenue comes from exports.

3. US hyperscalers are main drivers of the demand & India demand expected in 2 yrs