$NYCB isn't the canary in the coalmine that signals bad CRE loans are a systemic threat to the banking system. Here's the industry-wide delinquency rate. 👇

A 10% tariff on all imports. Up to 60% on imports from China. A Donald Trump win in November could mean lower US growth, rebounding inflation and higher rates. But his other isolationist policies would have an even bigger impact on global GDP growth https://t.co/w7Ahh3hvxk

We’re at the bullish end of 2024 S&P 500 forecasters – get our new report explaining the fundamental and speculative forces that will drive another year of outsized gains for US equities.

https://t.co/eGosrde4OM

#SP500#USequities

We estimate that core PCE prices increased by 0.17% m/m in Dec, which means the 3m annualised rate fell to 1.5%, the 6m annualised rate remained at a below-target 1.9% and the 12m rate dipped to 2.9%. Ignore the disinflation deniers, it's happening. Rate cut March.

“.. new data on rent inflation released this week raise the possibility that the disinflationary process won’t stop there, with a period of below-target inflation a growing risk.”

- @CapEconUS#CPI

About that "last mile is the hardest" nonsense. Remember rent of shelter accounts for 43% of the core #CPI basket. So if it does fall from 6.2% in Dec to -1% that would subtract 3.1% points, leaving core CPI Inflation at sub-1% by end-2024. Jan rate cut maybe?

We're Team #PCE rather than #CPI, but there's a possible upward revision to the portfolio management component coming that could add 0.14% to the core PCE inflation rate.

The collapse in the NY Fed manufacturing index to -43.7 in Jan is going to attract a lot of attention from the perma bears, but we'd caution it's more likely noise rather than signal.

We estimate that core PCE prices increased by 0.17% m/m in Dec, which means the 3m annualised rate fell to 1.5%, the 6m annualised rate remained at a below-target 1.9% and the 12m rate dipped to 2.9%. Ignore the disinflation deniers, it's happening. Rate cut March.

“The surge in Chapter 11 business bankruptcy filings .. is not as bad as it looks, as many of them related to the WeWork failure. Excluding those, bankruptcies trended lower at the end of 2023 and, with corporate bond yields falling .. the worst may already be behind us.”

@CapEconUS

The lagged impact of previous monetary tightening will continue to push GDP growth well below potential next year. Get our latest forecasts for the #US economy in our Q1 2024 US Economic Outlook. Download the key takeaways from our client report now.

https://t.co/RcrH5d1bIp

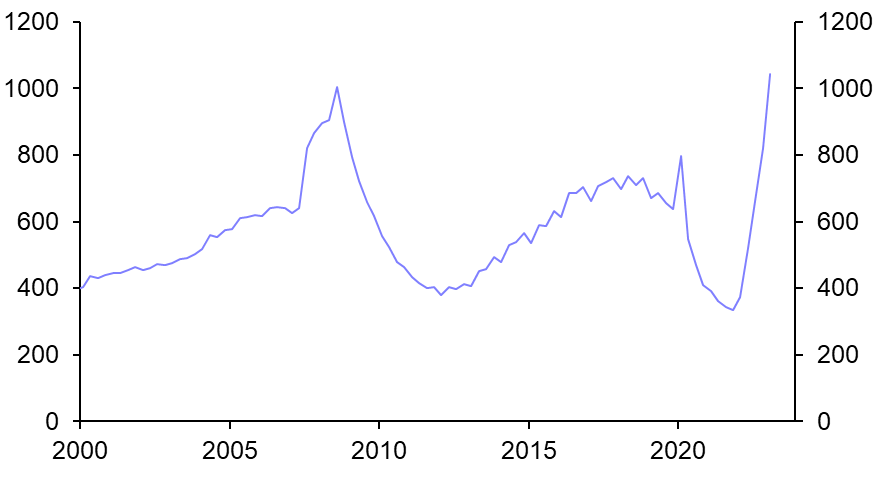

Post-SVB, Federal Home Loan Bank advances to commercial #banks rocketed to a record high of more than $1trn. The real lender of last resort in a banking crisis.

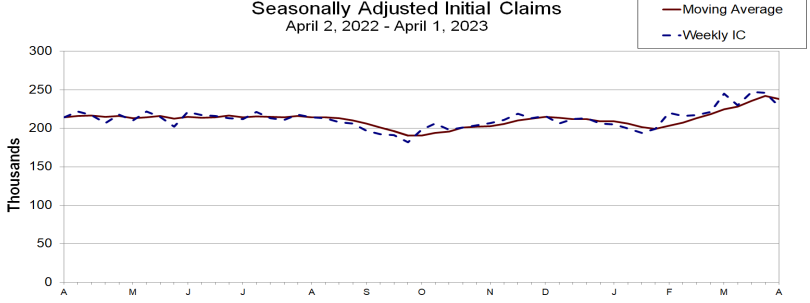

After switching up the blend on additive/multiplicative seasonal adjustment, the DoL now thinks that initial jobless #claims have been on an upward trend for several months. That matches a similar adverse trend in the Challenger mass layoffs data.

There's growing downside risk that the stresses on small US banks & commercial real estate develop into an adverse feedback loop. In a worse-case scenario, this could mean a rolling crisis that lasts for years. Read our report to learn more: https://t.co/IFzvc78wUL

#USrealestate

Data releases this week in new order of importance:

1. H.4.1 Fed's balance sheet (due Thurs)

2. H.8 commercial banks assets & liabilities (due Fri)

3. February CPI