This is the bigger idea:

Bondify is not just a place to create looping exposure.

It is a market layer for looping positions.

Future yield can be traded.

Position ownership can be transferred.

External positions can be migrated.

Exit paths can become more timely.

For users, the question becomes less:

“How do I enter/exit this loop?”

And more:

“What can I do with this position after I have it?”

That is where Bondify is different.

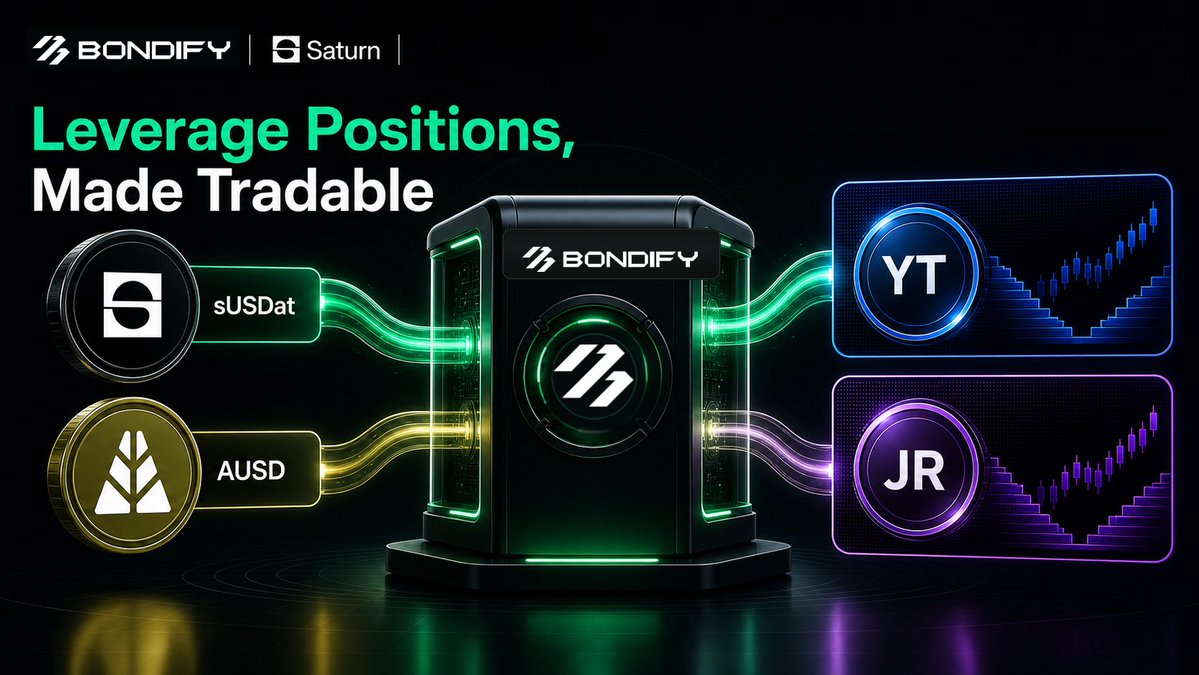

It is designed to make leverage positions which was once untradable becomes priceable, transparent, and tradable.

What is Looping in Bondify?

Looping is not only about opening a leveraged position.

Many users already build looping positions across DeFi.

The harder question is what happens after the position exists:

Can its future yield be sold?

Can the position itself be sold?

Can it be migrated instead of rebuilt from scratch?

One key feature is selling future yield.

A looper may want to keep the underlying position, but sell part of its future yield upfront.This creates a way to monetize expected returns without fully closing the position.

It also helps connect looping positions with yield markets, channeling additional supply to yield seekers from leveraged positions.

Another key feature is selling the looping position itself.

Instead of waiting for a full unwind, a user may want to transfer or sell the position to another participant.

This matters especially for RWA positions, where redemption timelines, liquidity conditions, and exit costs can make unwinding slower or more expensive.

Bondify also supports the idea of migration.

Looping does not always have to start inside Bondify.

If users already have external looping positions, the goal is to make those positions easier to bring into Bondify’s liquidity layer.

That means users can think beyond “open a new loop.”

They can also think about migrating existing exposure.

How to start with Bondify?🤔

Bondify is now live for yield-bearing RWA positions.

If you are new here, the easiest way to understand Bondify is simple:

Bondify lets users trade different parts of a looping position.

It starts with Saturn sUSDat/AUSD loop positions on Morpho.

From there, users can enter Bondify in two main ways:

🔵1. Trade YT

YT gives exposure to the future yield / points side of a supported position.

If you are bullish on the future yield or points from a strategy, but do not want to build and manage the full loop yourself, buying YT gives you a more direct way to access that exposure.

For existing loopers, selling YT can also be useful.

After migrating a position into Bondify, a looper may sell part of the future yield / points exposure to lock in value earlier or hedge against uncertainty in future rewards.

🟣2. Trade JR

JR represents the standardized looping position with unified LTV%.

For buyers, JR offers the same loop exposure at a discount to building it at par, without being capped by available lending liquidity.

For existing loopers, selling JR can create anotherexit path. Instead of manually unwinding the whole loop with waiting time, a looper can transfer part of the position exposure through the market.

This is the core idea behind Bondify:

A loop position does not have to stay as one static position inside its original lending market.

It can be migrated, priced, traded, and hedged, letting you lock in future yield.

👇Start here:

https://t.co/jIojFNE5sF

Bondify’s first supported market: @saturn_credit sUSDat/AUSD leverage positions on Morpho.

Bondify helps turn supported leverage positions into tradable exposures:

YT for future yield / points, and JR for standardized position exposure.

Leverage positions, once untradable.

Now priceable, transparent, and tradable.

👇Explore now:

https://t.co/VCQbWRTLVU

Tokenization gives access.

But access alone is not utility.

For RWAs to become useful inside DeFi, they need to support real actions:

build looping positions,

trade future yield,

manage and exit positions over time.

Bondify focuses:

Looping positions

Yield markets

The goal is to help yield-bearing RWAs move from passive onchain assets into active DeFi positions.

🚀Bondify is now live.

Yield-bearing RWAs should do more than sit onchain.

Today, many tokenized RWAs are accessible, but still underused inside DeFi.

Users can hold them, but it is much harder to build liquidity, looping strategies, yield markets, or flexible exit paths around them.

Bondify is built for that post-tokenization layer.

👇Start here:

https://t.co/jIojFNE5sF

🚀Bondify is coming soon.

Yield-bearing RWAs should do more than sit onchain.

They should move through liquidity, looping, and yield markets.

Built for the next phase of RWAfi.

APY Is Not Risk Analysis: What Is Paying for This Yield?

When people look at RWA assets, most of the attention usually goes to two numbers: APY and TVL. That is understandable. APY tells people what they may earn, and TVL shows how much capital has already entered. Both are easy to compare, easy to screenshot, and easy to turn into a market narrative. But neither is enough. Looking at APY and TVL without looking through to the underlying asset and the mechanism behind it is not risk analysis.

As RWA products become more composable and are wrapped into tokens, used as collateral, deposited into vaults, or looped through lending markets, risk no longer stays neatly at the asset level. It moves through the system. That is why a useful framework has to start from a simple principle: same APY, different risk; same TVL, different liquidity.

A 10% APY does not tell us enough. One 10% may come from Treasuries, another from private credit, another from basis trading, incentives, or leverage. These may look similar on a dashboard, but they represent very different risk. The real question is not how high the APY is, but what is paying for it.

To diligence yield properly, I would start with four questions. First, what is the economic source of the yield, and is it organic, subsidized, or amplified by leverage? Second, who takes the first loss if the structure comes under stress? Third, how stable is that source across changing market conditions? And fourth, what exactly does the holder have a claim on?

These questions matter because yield can be produced in very different ways. Some yield comes from relatively direct cash flows such as Treasury bills, staking rewards, or lending interest. Some comes from credit risk and compensates investors for borrower risk, collateral risk, illiquidity, underwriting complexity, and recovery uncertainty. Some comes from active strategies such as basis trading, delta-neutral positioning, market making, or OTC flow, where the risk lies not only in the asset but also in execution, leverage, counterparty exposure, and stress performance. Some comes from incentives rather than organic cash flow, which may be rational for bootstrapping but should not be confused with sustainable yield. Some comes from leverage, which can amplify returns but also introduces borrow-rate risk, liquidation risk, and exit-path risk.

A useful example is STRC, which has been discussed heavily recently. STRC is Strategy’s Nasdaq-listed perpetual preferred stock, and Strategy says it currently pays an 11.50% variable annualized dividend, payable monthly in cash.

Strategy also says the rate is adjusted monthly, that cash dividends

are not guaranteed, and that the rate may be significantly lower in

future periods. The dividend is ultimately supported by a corporate

treasury whose primary holding is BTC, with convertible notes sitting

senior to STRC in the capital structure. This means the yield is not independent of BTC price, funding conditions, or capital markets access. The number is attractive, but the number is not the analysis.

The relevant questions are what supports the dividend, how the rate can change, where the preferred sits in the issuer’s capital structure, how the claim behaves under stress, and what happens if market conditions change.

Once STRC-linked exposure is wrapped on-chain through structured products, the analysis becomes more important rather than less. The asset is no longer simply a traditional preferred stock. It becomes a yield source inside a DeFi stack. At that point, the question is no longer just what STRC is. The question becomes what the full path is from STRC dividends to the on-chain token holder, what the holder is actually exposed to, and who absorbs the loss if that path breaks.

TVL is easy to misread for similar reasons. A growing TVL can reflect product-market fit, confidence, or attractive relative yield. It can also reflect short-term incentives, leverage stacking, temporary liquidity windows, or crowded positioning. TVL tells us that capital entered. It does not tell us how quickly capital can leave. For RWA assets, that distinction matters even more because the token may move instantly while the underlying asset still settles on a redemption cycle, a DEX pool may exist while remaining too shallow for large exits, and a stable NAV may coexist with a portfolio that still takes time to liquidate. TVL should therefore be treated as a starting signal rather than a safety label.

The core point is straightforward. RWA risk analysis should not begin with a headline yield and end with a headline TVL. It should begin by asking what is paying for the yield, what the holder actually owns a claim on, how stable that source really is, and who takes the loss when the structure comes under stress.

Following continued monitoring, assessment, and necessary handling, Cian has now resumed normal deposit and withdrawal services for all ETH-related strategies.

Previously, due to volatility in underlying market conditions and related incidents, we implemented temporary risk control measures on certain ETH-related strategies as a precaution to prioritize user fund safety. After further review and observation, these strategies have now returned to normal operation, and users may deposit to and withdraw from them as usual.

We will continue to closely monitor underlying protocols, market liquidity, and relevant risk indicators, and will dynamically manage risk controls and strategy operations to help ensure the safety of user assets and the stability of our strategies.

Thank you for your understanding and patience.

Due to the recent Kelp DAO rsETH bridge incident, ETH borrowing conditions on Aave have seen short-term volatility and imbalance. As a precautionary measure, CIAN has temporarily paused deposits and withdrawals for all ETH-related strategies.

This is a risk control measure in response to abnormal market conditions caused by an external event, and was not triggered by any security incident involving CIAN’s frontend or strategy contracts.

We are closely monitoring ETH borrowing rates, liquidity conditions, and strategy execution parameters.

We will keep you posted as we learn more about the situation. Please follow only @CIAN_protocol for updates.