Independent biopharma research

Clinical evidence • Drug development • Valuation

↓ Latest research

Clinical trials • Drug development • Healthcare investing

Where bears are still building in XBI. 🧵

Most short-interest screens rank stocks by current short interest.

But the more useful question is:

Where are shorts still adding?

Level ≠ flow.

What stood out from the June 30 FINRA settlement across the $1-5B $XBI biotech universe:

We aren’t building another “most shorted” leaderboard.

The Clinaptis Monthly Biotech Short Interest Monitor is a recurring framework for tracking how bearish positioning evolves around clinical and commercial catalysts.

👇 Full June 30 report below.

>$27B for Orforglipron is pure science fiction. Even $ABBV's Humira did $22Bish at its peak. In a crowded oral market, even with $LLY's execution, $7.5-$9B is our bull case. Expect estimates to keep getting chopped as we approach YE26.

Stellar review of the recent and remarkable advances vs Alzheimer's disease (AD).

Towards "a future where AD is not only treatable but also preventable."

@CellCellPress

https://t.co/p3hbqkDrtF

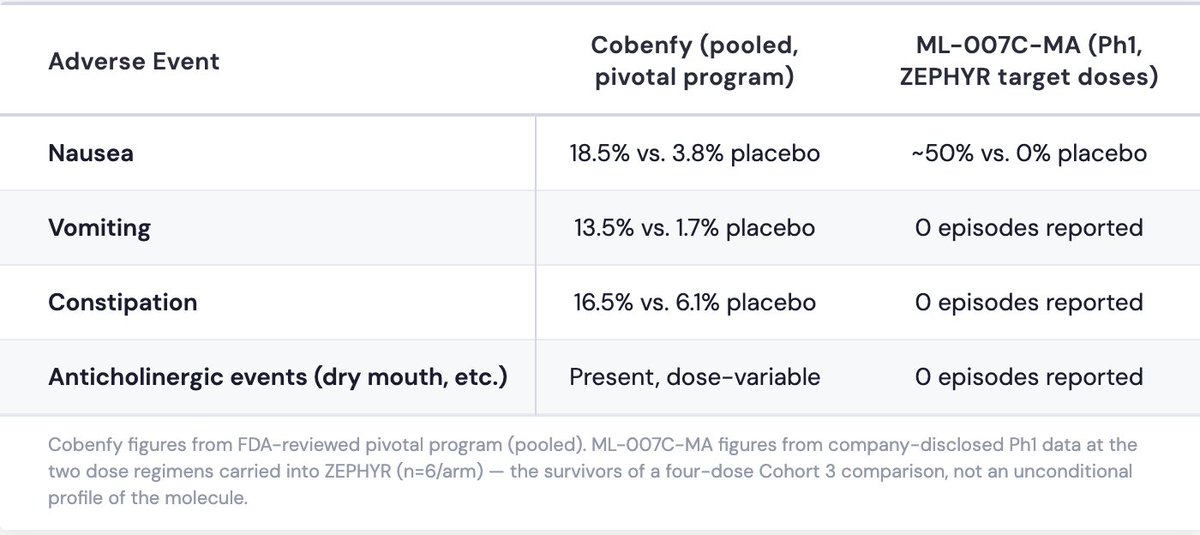

Cobenfy (KarXT) proved muscarinic agonism works 🧠 First new schizophrenia mechanism in 30 yrs.

MapLight ($MPLT ) doesn't need to de-risk the mechn.

It needs to prove its fixed-dose combo is actually better. Ph2 ZEPHYR reads out in August 📅

Here's the institutional bet 🧵👇

Our base case on ML-007C-MA:

✅ Efficacy in-line with Cobenfy (PANSS)

⚠️ Tolerability edge — sound, but unproven at scale If safety holds, it's not just a schizophrenia story—it reads straight into their Alzheimer’s psychosis asset.

🎯 Full note 👇

https://t.co/wg9eFqeDyt

Early Phase 1 data looks immaculate.

Too immaculate? 🤔

❌ 0% vomiting

❌ 0% constipation

❌ 0% anticholinergic events

But that’s 40 healthy volunteers over short dosing windows. Psychotic patients in an acute exacerbation are a completely different safety profile. 📊

Atacicept Approved. Called it. $VERA

Stock up 8% intraday. Flat-ish 5D -2%.

Label: no UPCR threshold. Broader than expected.

Weekly vs. monthly still the commercial headwind.

Q3 eGFR is the only number that matters now.

🔗 https://t.co/4lR687ljk6

$NVS $OTSUKA #IgAN

1. IgAN now has five approved therapies spanning four different mechanisms.

Yet most reduce proteinuria by roughly 40-50%.

The question is no longer who reduces proteinuria most.

It’s who leaves the least disease behind.

🧵

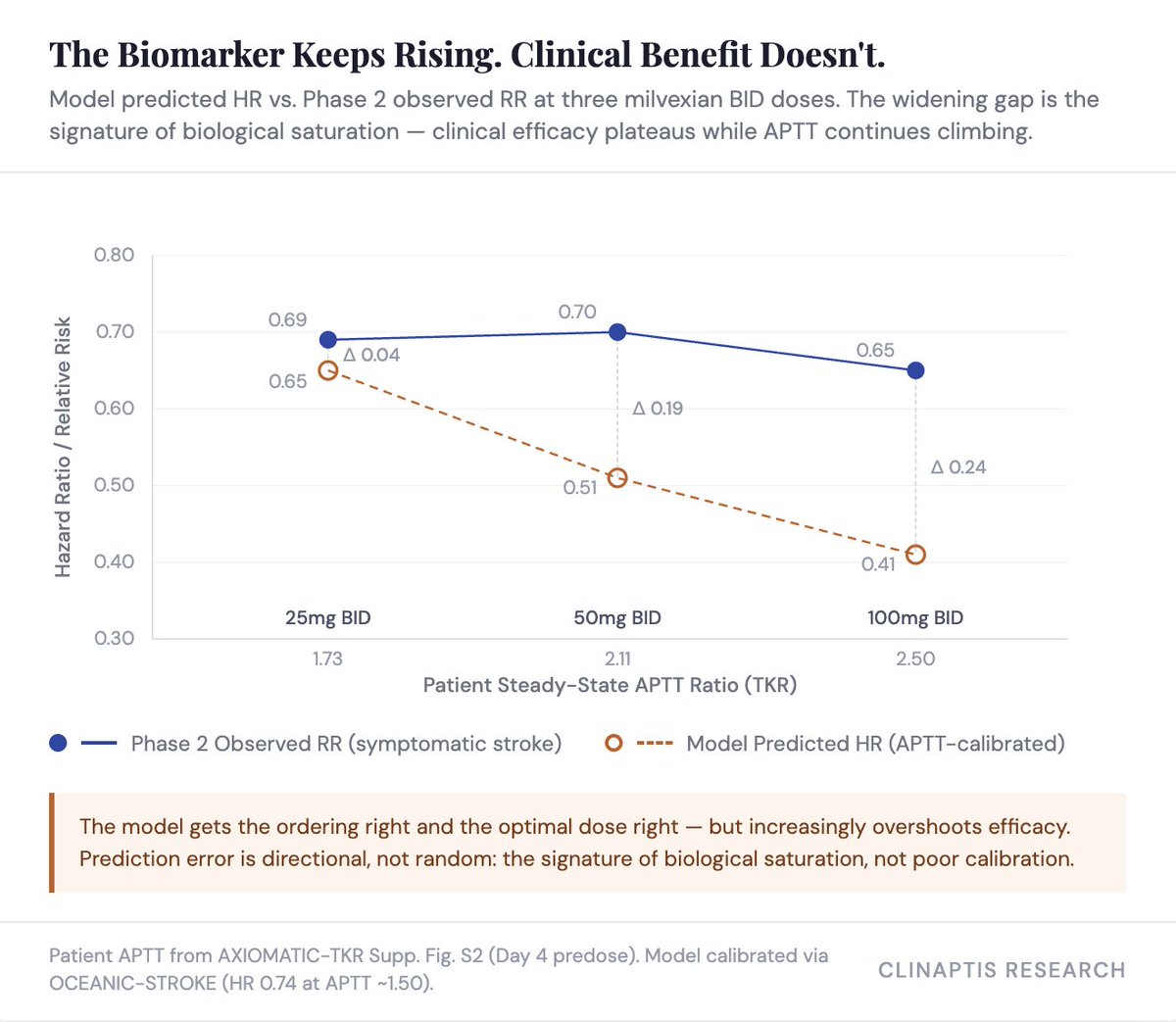

Milvexian ($BMY / $JNJ ): one failed Ph3 shifted the narrative toward caution.

ACS was always the low-expectation trial — the real value sits in Stroke and AF, both still ongoing.

Readout: YE2026.

Here's why they should be valued separately 🧵

Stroke is the higher-confidence clinical call (~65-70% POS, HR ~0.69-0.74).

AF is the higher-value commercial call, lower confidence (~55-60% POS) — our AF HR estimate is in the full note.

👇

$AMLX Phase 3 PBH readout is being treated as a binary event in 3Q26.

The market is focused on the wrong uncertainty - so reconstructed LUCIDITY using three independent statistical frameworks,

it's not n=78 sample size, but how much the Ph2 effect compresses in Ph3 of PBH

🧵

At today’s EV, AMLX pricing ~ 11K peak treated pts & underwrites the diagnosed population, not the diagnosable one.

📈 ~34% upside in the base case.

🚀 ~150% upside if approval expands diagnosis beyond today’s recognized PBH pop'n.

So, approval isn’t the end of the thesis!

👇