There is a drawer in almost every established company where the best AI experiments go. Not because the experiments failed. Because they worked too well and threatened something profitable. Find the drawer. That's the Kodak story repeating

Oil businesses can be really interesting.

Its cyclicality produces hidden opportunities.

Markets can stay irrational longer than you can stay rational.

A good oil business riding this tailwind can stay depressed for long periods.

So be in the Lutéce.

Because whatever you order, chances are, it will be Michelin grade.

QNX is 49% of revenue.

It delivered $268 million in FY2026 (up 13.6%).

It is a safety certified embedded operating system.

However, this take years to become royalties as vehicles ship.

$BB

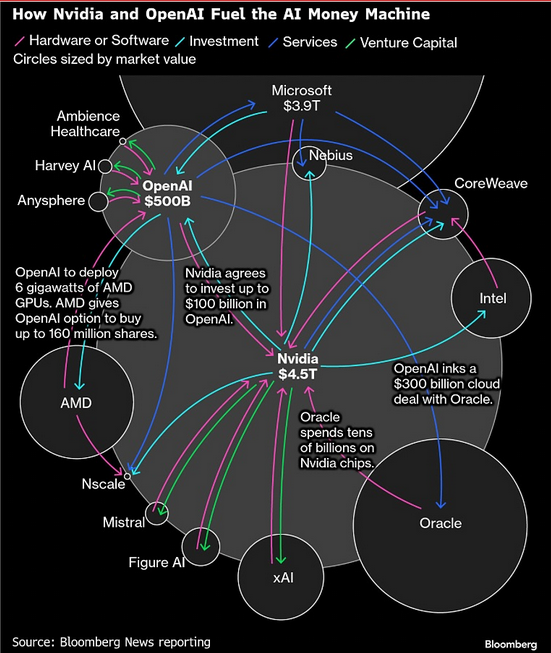

NVIDIA is financing its own demand.

$NVDA is reporting 55.6% net margins.

But is also putting billions into entities that buy its chips.

This is not a clean platform business.

This is a hardware company supporting its own revenue.

Watch Data Center revenue sequentially.

A sustained slowdown while hyperscalers ramp their own chips would expose the model.

This is the clearest test.

Everything else is secondary.

$NVDA

NVIDIA is financing its own demand.

$NVDA is reporting 55.6% net margins.

But is also putting billions into entities that buy its chips.

This is not a clean platform business.

This is a hardware company supporting its own revenue.

The market prices current margins as durable.

It assumes customers will keep expanding purchases of $NVDA full stack.

The financials show a different reality.

NVIDIA is already using its balance sheet to support demand.