I’m not going to $TEL you where I bury my $HBARs and $BTC. 🥃 🥃 🥃 New profile not noob. (Due to confusion- I am not Ron Swanson and this is not my photo)

Oh boy… it’s almost telcoin:native time. Clues are everywhere. Don’t cry later 100x from here saying “How would I ever know”. Clues are everywhere ⏰👀 ripple:native ethereum:0x514910771af9ca656af840dff83e8264ecf986ca

Telcoin has started moving again…

but most people still don’t understand what it’s building.

What if the future of finance doesn’t come from banks…

but from mobile phones connected across the world?

New clip below.👇

telcoin:native #telcoin

@Sic2336 You should take a look at @telcoin, fam. telcoin:native coin will benefit from both sides as a crypto project and as a bank. The only federally regulated depository charter bank in the world. (About to open its doors for on-chain banking services)

📲 $TEL's stablecoin moat vs USDC and USDT:

USDC (Circle): regulated, but no Federal Reserve access. No banking charter.

USDT (Tether): unregulated offshore. No banking charter.

eUSD (Telcoin): federally chartered bank + Federal Reserve access + telecom distribution.

Circle and Tether CANNOT get what Telcoin has.

A banking charter requires years of regulatory work.

Federal Reserve access requires passing bank supervision.

Telecom distribution requires being a telco — or partnering with 200 of them.

$TEL's eUSD is structurally unreplicable. 🔐

🚀 $TEL Holders — this is the moment you've been waiting for!

Telcoin just unlocked history with the first regulated Digital Asset Bank charter in the US, launching real eUSD stablecoin and bridging traditional finance with blockchain power! 💥

Mobile operators worldwide are securing this EVM Layer 1, powering seamless cross-border transfers to 20+ countries and 30+ e-wallets. Real utility is here — Digital Cash is going mainstream!

Builders, remittance users, and crypto believers: the Telcoin Wallet V4+ is your gateway to the Internet of Money. Get ready for explosive adoption as eUSD, eEUR and more roll out!

This isn't hype — it's regulated reality delivering massive value to holders and users. Who's positioning for the next leg up in $TEL?

Drop your biggest takeaway below — are you all-in on Telcoin's bank revolution? 👇

@Telcoin@telcoin #Telcoin #TEL #CryptoBank #Stablecoin #Remittance #Web3 #DeFi #DigitalAssets

Buying more $TEL. Again. 🛒🔥 While the timeline FUDs without even reading the docs, the sleeping giant is waking up. Mass telecom adoption is coming. Paper hands, get out now. See you on the moon. 🌕🚀 #Telcoin $TEL Time will #tel

telcoin:native at ripple:native’s market cap = ~$0.94.

That’s a 331x reminder of what happens when real utility, regulatory groundwork, stablecoin rails, and patience finally collide.

The market has slept on @Telcoin long enough!

#TEL/#Telcoin 🚀🌍📲

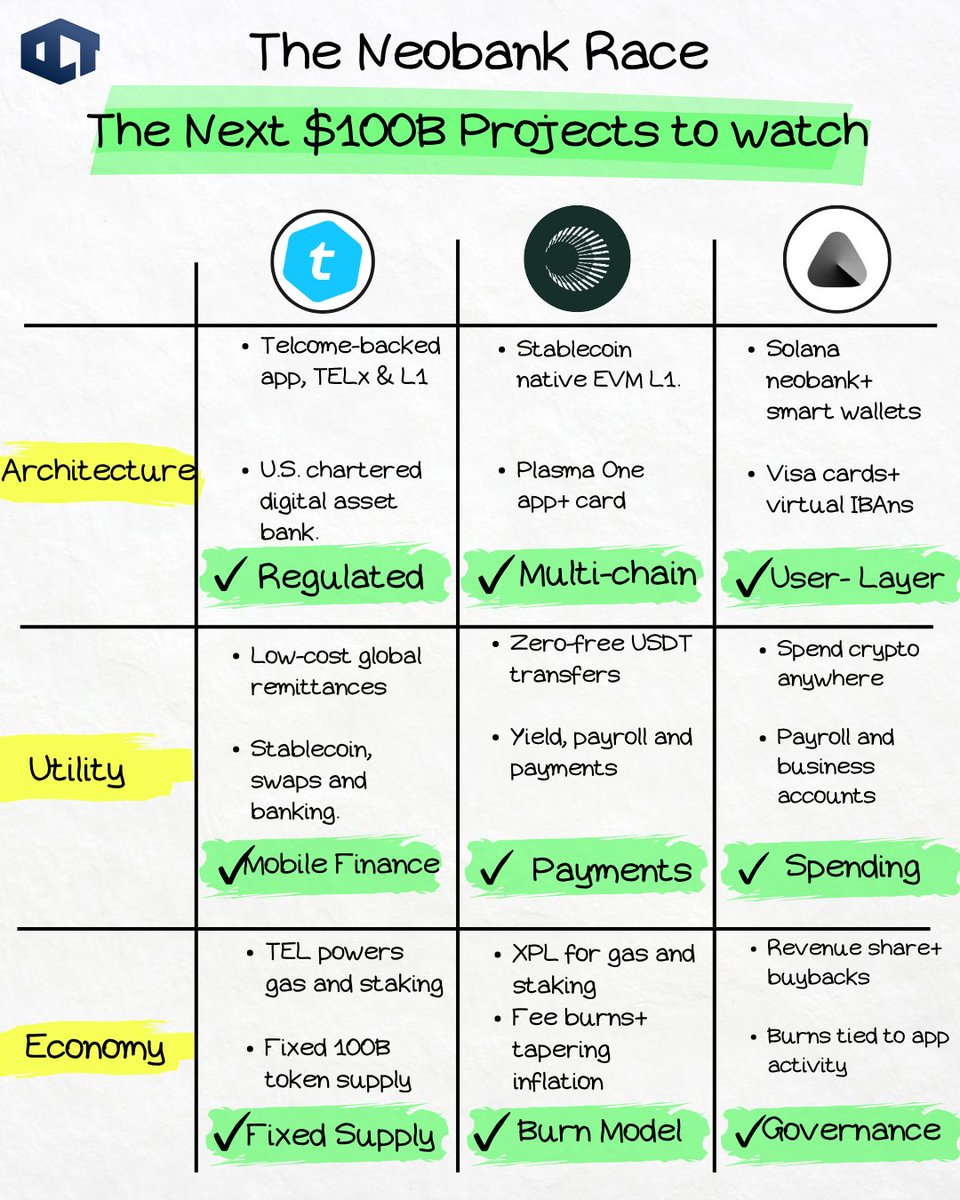

1. Everyone is chasing meme tokens, while crypto neobanks quietly target a $100B+ fintech shift.

Three early names sit at the center of Crypto Neobanks:

→ Telcoin ( $TEL )

→ Plasma ( $XPL )

→ AviciMoney ( $AVICI )

One of these could be the next 10x👇

🔵Telcoin ( $TEL ): The Telecom-Backed Regulated Neobank Platform

Telcoin is not building just another crypto wallet.

It is building a full-stack regulated fintech platform that connects mobile money, stablecoins, telecom distribution, and blockchain banking.

That matters because financial access is still heavily fragmented across the world.

Billions of people use mobile phones.

Hundreds of millions rely on mobile money.

But traditional banks still struggle with cross-border payments, high fees, slow settlement, and limited access in emerging markets.

Telcoin’s thesis is simple:

• Use telecom networks as the distribution layer.

• Use blockchain as the settlement layer.

• Use a regulated digital asset bank as the compliance layer.

That combination makes Telcoin one of the most serious neobank bets in crypto.

Architecture→ Mobile-First App + TELx + Operator-Secured L1

Telcoin’s core platform has three main layers.

First, the "Telcoin App" acts as the mobile gateway.

It is where users access remittances, stablecoins, wallets, and future banking products.

Second, TELx provides the self-custodial DeFi liquidity layer. This supports swaps, liquidity routing, and on-chain financial activity.

Third, the Telcoin Network is a public EVM-compatible Layer 1. Its most important design choice is validator selection.

The network is secured and validated by GSMA mobile network operators.

That gives Telcoin a very different trust model from most crypto networks.

Instead of relying only on anonymous validators or retail staking, Telcoin plugs into existing telecom infrastructure.

The Bank Layer→ Telcoin Digital Asset Bank

The biggest unlock is the **Telcoin Digital Asset Bank**. Telcoin received a Nebraska Digital Asset Depository Institution charter in November 2025.

That made it one of the first U.S.-chartered digital asset banks focused on blockchain-powered finance.

This bank layer allows Telcoin to issue **Digital Cash** stablecoins.

These include eUSD and other planned fiat-backed currencies such as eAUD, eCAD, and eMXN.

Each stablecoin is designed to be backed 1:1 by fiat reserves. The idea is not to create another offshore stablecoin.

The idea is to create regulated, bank-issued digital money that connects directly to traditional financial rails.

Utility→ Remittances, Stablecoins, Banking, and Governance

Telcoin’s utility is rooted in real financial activity.

The platform targets:

• Low-cost global remittances

• Mobile wallet transfers

• Bank-issued stablecoins

• Merchant payments

• Self-custodial swaps

• Digital deposits and loans

• Fiat on-ramps and off-ramps

• Operator-secured blockchain settlement

This is not DeFi for DeFi users only.

It is mobile finance for everyday users.

That is why Telcoin’s telecom strategy matters.

Economy→ Fixed Supply and Usage-Aligned Incentives

TEL has a fixed max supply of 100 billion tokens.

Its design focuses on long-term ecosystem growth rather than aggressive short-term inflation.

Token distribution supports market circulation, ecosystem incentives, telecom operator participation, and team allocation with vesting.

TEL issuance is programmatic and controlled through the treasury. That matters because neobank tokens need sustainable economics.

They cannot rely forever on hype, liquidity mining, or temporary reward campaigns.

Telcoin’s model is more conservative.

Validators, users, telecom partners, and ecosystem participants are incentivized around productive activity.

As stablecoins, remittances, banking products, and network usage grow, TEL becomes more deeply tied to the platform’s financial flows.

My take:

Telcoin is the strongest regulated, telecom-anchored neobank in crypto today.

If mobile money and compliant stablecoins become mainstream, $TEL could become the backbone utility token for global crypto banking.

🟢 2. Plasma ( $XPL ): The Stablecoin-Native L1 Neobank

Plasma takes a more focused approach.

It is not trying to be a broad Layer 1 for every crypto use case.

It is building a high-performance EVM-compatible blockchain designed specifically for stablecoin payments.

That focus matters. Stablecoins are already one of crypto’s strongest product-market fits.

People use them for trading, remittances, savings, payroll, merchant settlement, and cross-border transfers.

But most chains were not built specifically for stablecoin payments.

They were built for general-purpose smart contracts. Plasma flips that model.

Architecture→ Stablecoin L1 + Plasma One App

Plasma is an EVM-compatible Layer 1 built around USDT payments.

Its pitch includes native USDT support, fast settlement, high throughput, and zero-fee or near-zero-fee stablecoin transfers.

That makes it very different from most chains where stablecoin transfers still compete with every other type of on-chain activity.

The network is also designed to connect Bitcoin-level security assumptions with Ethereum-style tooling.

This gives developers access to familiar EVM infrastructure while giving users a payment-first experience.

The second major piece is Plasma One

This is the consumer-facing neobank super-app.

Users can hold, send, spend, and earn from stablecoin balances without needing to jump across wallets, bridges, and DeFi protocols.

That is important because most normal users do not want to manage complex DeFi workflows.

They want a simple app. They want stable balances.

They want instant transfers. They want a card.

They want yield without complexity. Plasma is trying to package all of that inside one stablecoin-native ecosystem.

Utility→ Zero-Fee Transfers, Cards, Yield, and Payments

Plasma’s utility is very clear. Users get instant stablecoin transfers.

They get access to a Plasma One card. They can spend stablecoins across merchant networks.

They can access integrated DeFi yield. They can use stablecoins for payroll, remittances, and merchant settlement.

That makes Plasma highly relevant in emerging markets.

In regions where local currencies are unstable, banking access is limited, or cross-border fees remain high, stablecoins already solve real problems.

Plasma wants to make those flows smoother.

The $XPL token secures the network through staking and delegation.

It also pays gas outside gasless USDT transfers. It supports governance. And it powers ecosystem rewards.

That gives XPL a direct role in the infrastructure layer behind stablecoin payments.

Economy→ Inflation Tapering, Fee Burns, and Usage Growth

XPL has an initial supply of 10 billion tokens.

Its inflation begins at 5% for validator rewards and tapers over time toward a 3% floor.

This helps bootstrap security while reducing emissions over time.

The network also uses an EIP-1559-style burn mechanism for base transaction fees.

That means higher usage can create deflationary pressure. This is important because stablecoin networks need volume.

A payments chain without transaction activity has weak economics.

But a payments chain with serious stablecoin flow can generate meaningful fee burn, merchant revenue, card revenue, FX revenue, and DeFi activity.

Plasma’s upside depends on whether it can attract enough users and liquidity to make that flywheel real.

The early liquidity base and DeFi partner network give it momentum.

But execution risk remains high.

The stablecoin market is competitive.

Payments users are hard to acquire.

And neobank apps need trust, reliability, compliance, and distribution.

My take:

Plasma is the pure infrastructure plus distribution bet.

If stablecoins become everyday money, $XPL could power the rails while Plasma One captures the user layer.

⚫ AviciMoney ( $AVICI ): The On-Chain Internet Neobank

Avici takes a different route.

It is not building the telecom backbone like Telcoin.

It is not building a stablecoin-native Layer 1 like Plasma.

It is building the front-end experience.

Its goal is to make crypto spending and stablecoin finance feel as easy as using a modern fintech app.

That positioning is powerful because users rarely care about the rails underneath.

Architecture→ Solana Neobank + Visa + Virtual IBANs

Avici combines self-custodial smart wallets, Visa cards, business accounts, and stablecoin payroll tools.

Users can spend without fully exiting crypto.

Businesses can manage treasury and payments.

Freelancers can receive stablecoin income and use funds in the real world.

Recent upgrades include virtual IBAN accounts.

That is important because IBAN access improves fiat-to-stablecoin onboarding, cross-border payments, and global account functionality.

This makes Avici feel less like a crypto wallet and more like a crypto-native bank account.

Utility→ Spending, Ownership, and Revenue Share

The $AVICI token is designed around ownership and revenue participation.

Its utility includes:

• Revenue sharing from card fees and services

• Buybacks and burns from real activity

• Governance over product development

• On-chain payroll tools

• Business accounts

• Future credit products

• Trust scoring and financial identity

This is where Avici becomes interesting.

It is not only offering access.

It is trying to let users own part of the neobank they use.

That is a strong crypto-native idea.

Traditional neobanks capture user activity and keep the upside for private shareholders.

Avici tries to redirect some of that value back to token holders and users.

That creates a direct flywheel.

Economy→ Revenue-Backed Deflation and a Live Flywheel

Avici’s economy is more usage-driven than emission-driven.

Card fees, transaction activity, and product revenue fund buybacks, burns, and ecosystem expansion.

That makes it cleaner than many token models.

The risk is liquidity.

Thin liquidity can create major volatility.

A smaller user base also means the flywheel needs more scale before the economics become durable.

Still, Avici has one advantage many crypto projects lack:

My take:

Avici is the pure interface and ownership play.

If crypto neobanks go mainstream, the front-end that users actually enjoy could capture outsized value.

The Neobank Stack→

These three projects are not direct copies of each other.

They represent different layers of the same future.

Telcoin ($TEL)

Regulated telecom distribution, bank-issued stablecoins, and mobile financial infrastructure.

Plasma ($XPL)

Stablecoin-native Layer 1 rails, zero-fee transfers, and a consumer payments app.

Avici ($AVICI)

Solana-based user interface, cards, IBANs, payroll, and revenue-linked ownership.

That is why the comparison is interesting.

Final Rankings

Best Architecture→

$TEL > $XPL > $AVICI

Telcoin has the most complete and regulated architecture.

It combines telecom operators, a digital asset bank, stablecoins, an app, DeFi liquidity, and its own Layer 1.

Plasma comes second because its stablecoin-native chain is highly focused.

Avici ranks third because it depends more on front-end execution and Solana infrastructure.

Best Utility and Adoption Potential→

$AVICI > $TEL > $XPL

Avici has the clearest user-facing experience.

Cards, payroll, IBANs, spending, and business accounts are easy for users to understand.

Telcoin has broader infrastructure and remittance utility, but adoption depends on telecom and banking rollout.

Plasma has massive potential, but it still needs to prove sticky user adoption around Plasma One.

Best Economic Sustainability→

$TEL > $XPL > $AVICI

Telcoin has the strongest long-term sustainability because of its capped supply, regulated bank model, telecom alignment, and real payment flows.

Plasma has strong economics if transaction volume grows enough to support fee burns and stablecoin activity.

Avici has a clean revenue-backed model, but thin liquidity and smaller scale make it riskier today.

🔚 Final Takeaway

If you want the regulated global remittance and bank-issued stablecoin play:

Telcoin ($TEL) is the strongest bet.

If you want the stablecoin-native payment rails and neobank distribution play:

Plasma ($XPL) has the highest infrastructure upside.

If you want the consumer crypto spending, card, payroll, and ownership play:

Avici ($AVICI) is the most direct user-layer bet.

The meme trade is loud.

The neobank shift is quiet.

But this is where real crypto adoption may happen.

That is why $TEL, $XPL, and $AVICI deserve serious attention.

They are not just tokens.

They are three different bets on the same outcome:

Crypto becoming the financial layer for everyday money.

The 400x run from $TEL in 2020/21 will not only happen again, it’ll go beyond that.

@telcoin is building a regulated on-chain banking infrastructure with real-world utility through mass adopted already existing infrastructure from giant telecoms. Watch it unfolding👀 ripple:native ethereum:0x514910771af9ca656af840dff83e8264ecf986ca

I created this BOB MORTIMER name generator with Manus in 5 mins this morning. Share your own #manus#ai#bobmortimer#namegenerator

I got "Turnip Graham" — We called him that because he was earthy and dense...

What's YOUR Bob Mortimer name? https://t.co/nGbRd0QU9l

Britain took on fifty nations. African kings. Arab sultans.

Bombarded ports. Deposed rulers who refused. Lost 1,600 men. Spent 40% of the entire Treasury.

A debt so big it wasn't paid off until 2015. You or your parents were still paying for it.

Not for land. Not for gold.

To end the slave trade.

They captured 1,600 ships. Freed 150,000 people. Patrolled 3,000 miles of coastline for sixty years.

And none of it was the government's idea. It was 400,000 ordinary people who signed petitions and 300,000 families who refused to buy sugar.

They forced Parliament's hand. Your ancestors changed the world and nobody told you.

If you think this should be taught in schools, help us reach more people: https://t.co/rih7iKwnvf

Be part of us

Be Proud Of Us 🇬🇧