Since you asked an honest question here’s my attempt to honestly answer it:

America’s wealth is driven primarily by high-value service industries such as banking, technology, and entertainment. Just think of companies like JPMorgan Chase, Netflix, or Amazon. These sectors not only dominate the domestic economy but also play a key role in U.S. exports.

According to the U.S. Bureau of Economic Analysis, in 2023 the services sector accounted for over 77% of the U.S. GDP, while manufacturing contributed approximately 11%. The U.S. is also the world’s largest exporter of services, with exports totaling more than $970 billion in 2023—covering financial services, software, cloud computing, intellectual property, and consulting. These are areas largely not subject to tariffs.

In a sense, manufacturing is a game the U.S. has already outgrown, shifting its focus to more sophisticated and less labor-intensive sectors. This evolution allows the U.S. to leverage its comparative advantage in innovation and productivity, rather than competing on low-cost labor.

Meanwhile, many other countries impose tariffs on U.S. agricultural and consumer goods because they lack competitiveness in fields like finance, technology, and professional services. By protecting these less efficient sectors, they attempt to shelter local jobs, but at the cost of higher consumer prices and economic inefficiencies.

Americans are major consumers of agricultural and manufactured goods, not because these sectors dominate the economy, but because of the purchasing power generated by a highly productive, service-oriented economy. Imposing tariffs on imports may create the illusion of protecting domestic jobs, but in reality, it often leads to higher prices for consumers and little to no job creation, especially in a country operating near full employment (the U.S. unemployment rate was just 3.7% in early 2024).

In short, tariffs are a blunt instrument that may be politically appealing but are economically inefficient in a modern, dynamic, service-led economy like the United States.

@BradRTorgersen It would make more sense if tariffs were sector specific and targeted due to the competitive advantage caused by low labor cost.

From my understanding, they are reciprocal; if they lower their tariffs so will we. Jobs will stay where they are of the negotiation works.

@bretas_erick@BradRTorgersen This is one of the most thoughtful resorts I've seen to the tariff debate. No "orange man bad" appeals to emotion, just practical real world facts. We need more in the world like you. Thank you sir.

@elonmusk Your claim that judicial blocks on presidential orders signal "TYRANNY of the JUDICIARY" oversimplifies the U.S. system. Courts uphold checks and balances, not tyranny, by ensuring executive actions comply with the Constitution—crucial for democracy, not its demise.

@DisrespectedThe Price inflation will occur whether or not the countries move operations to the US. Either through the increased taxes or increase moving/labor cost. I don't see any other way around it.

#BTC

Bitcoin has experienced a rejection from the top of the Downtrending Channel (red) just like in the past (blue circles)

It's essential Bitcoin Weekly Closes inside the red resistance to avoid a deeper rejection from here

Still early on in the week

Generally, we need to observe this Downtrending Channel resistance (red) for signs of weakening compared to previous rejections

$BTC #Crypto #Bitcoin

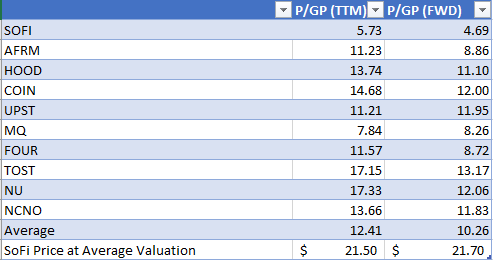

If $SOFI were priced the same as their fintech competitors, they'd be trading above $21 today (based on gross profit).

SoFi is above average in both growth and profitability from this list, so it should trade at an above average price.

Still lots of room to run.

Buying since sub $5 with an average cost of $7.30. If I'm comfortable with this breakout, I will likely be dip buying with a $14+ target. If the dips don't happen, I'm happy with my position. $SOFI