Here are some of the craziest details from Labor's 2026 Federal Budget:

- $124M for powerful Jewish lobby group the Executive Council of Australian Jewry (which is behind Australia's new "hate speech" laws)

- $207.4M to "combat the influences of anti-Semitism, violent extremism and hate"

- $46.7M in financial support for the Jewish community

- $41M for various education department anti-Semitism initiatives

- $9M for a hate crimes database

- $68.8M for National Security Investigations teams (hate speech and social media post police)

- $32.6M on social cohesion public awareness campaigns

- $793M for "Closing the Gap" policies for aboriginals

- $36.6M to help aboriginals to vote

- $48.3M for aboriginal hostels

- $4.2M for a new National Aboriginal and Torres Strait Islander Cultural Precinct

- $6.8M for aboriginals to "own, access and manage water"

- $308.6M to "end gender-based violence"

- $50.4M to continue investigating alleged Afghanistan war crimes

- $6.6M to give missiles to the UAE

- $64.6M to recruit Papua New Guineans into the Australian Defence Force

- $16.6M to investigate sexual violence in the ADF

- $24.7M to recycle solar panels

- $112.7M for gambling addicts

- $25.3M on the India-Australia Comprehensive Strategic Partnership, mainly for a grants and fellowships program

- $167.3M for Nauru

- $550M to "support high‑quality, climate‑resilient infrastructure in the Pacific and Timor‑Leste"

- $33.2M for Indonesia

- $68.5M for HIV treatment for immigrants who are not eligible for Medicare

- $449.3M for RSV vaccines

- $10.8M to "provide community‑led health literacy education to refugee and migrant women"

- $7.7M to boost refugee employment

- $74.2M to fight abuse of the refugee visa system

- $27M to make migrant workers follow the law

- $19.8M to fight abuse of the student visa system

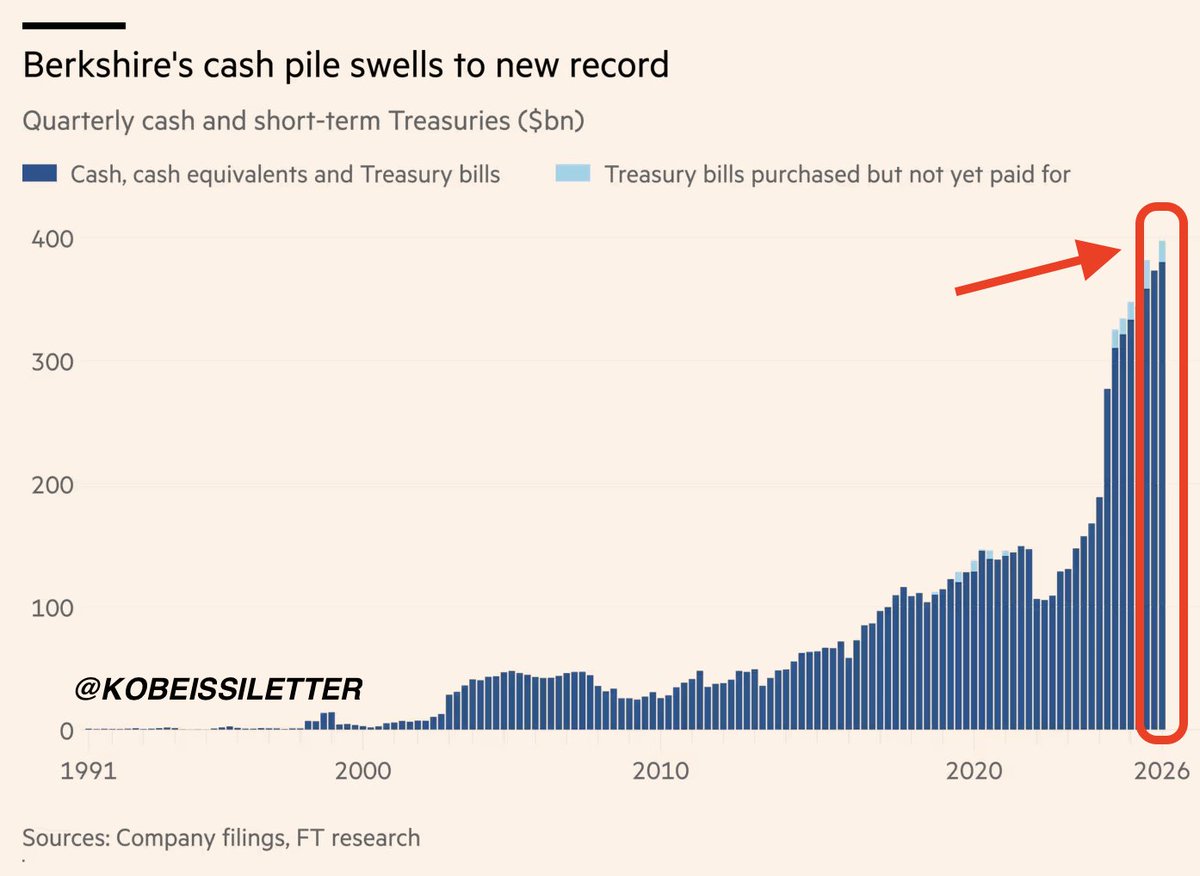

BREAKING: Berkshire Hathaway announces its cash balance is now up to a record $397 billion.

The company sold a net -$8.1 billion worth of stocks last quarter, marking its 14th-consecutive net quarterly sale.

Paul Tudor Jones just said something the market really doesn't want to hear.

"We're clearly so leveraged in equities in this country. We're 252% of stock market cap to GDP. In 1929, we were at 65%. In 1987, about 85%. In 2000, we got to 170%. And now we're at 252."

Every number he listed, 1929, 1987, 2000 ended the same way.

"If you think about the periodicity of significant bear markets since 1970, we get a mean reversion about every ten years. That would be a 30 to 35% decline. Well, 35% on 250% of GDP is 89% of GDP. The reverse wealth effect, oh my gosh. 10% of our tax revenues are capital gains; they go to zero."

This isn't a perma bear making noise but Paul Tudor Jones called the 1987 crash before it happened and made 200% that year.

When he talks about mean reversion, he's speaking from a track record that almost nobody in finance can match and then he said this:

"If you buy the S&P at this current valuation, the 10-year forward returns are negative when you buy with the S&P P/E of 22. That's what history shows."

He's right, every major study on long-term equity returns shows that starting valuation is the single most predictive variable for 10-year forward performance.

At a P/E of 22, history doesn't give you a great answer.

"The real problem is, if you look at private equity in 2007 and 2008, that was about 7% of institutional portfolios. Now it's about 16%. Real estate's gone up. Infrastructure bets have gone up. We're so much more illiquid than we were in 2008."

In 2008, the crisis was bad because the system was leveraged.

Today the system is leveraged and illiquid, pension funds, endowments, and sovereign wealth funds can't hit a sell button on private equity.

They can't exit real estate in a week, when forced deleveraging starts in a system this illiquid, the exit doors are half the size they were last time.

Jones didn't say a crash is coming tomorrow.

He said the conditions that produce the worst outcomes in financial history are more present right now than at any prior peak he's seen in 50 years of trading.

He said buying the S&P at these levels and expecting the same returns as the past 100 years is math that doesn't work because those 100-year averages include decades when stocks were priced at 6 or 7 times earnings, not 22.

"Valuation matters a lot, and the stock market's really high, and it's going to be really hard to make money from here."

Paul Tudor Jones says the US is more dependent on equity prices than ever, and explains what a 35% correction would trigger in the economy:

"We're 252% of stock market cap to GDP. In 1929 we were 65%. In 1987 we got to ~85-90%. In 2000, 170%.

If you think about the periodicity of significant bear markets. Since 1970, we get a mean reversion about every 10 years.

Let's say mean revert to the past 25 or 30-year PE. That would be a 30, 35% decline. Well, 35% on 250% of GDP is 80, 90% of GDP.

10% of our tax revenues are capital gains, they go to zero. So you can see the budget deficit blowing up. You can see the bond market getting smoked. You can see this kind of negative self-reinforcing effect.

In the stock market, we're over-equitized as a country. We have the highest individual equity weightings in the history of the country.

And then the real problem is if you look at private equity in 2007-2008, that was about 7% of institutional portfolios. Now it's about 16% of the institutional portfolios. We're so much more illiquid than we were in 2008.

The problem is that if you buy the S&P at this current valuation, the 10-year forward return is negative when you buy the S&P with a PE of 22. That's what history shows.

So yes, the S&P is spectacular long-term, if you have a hundred-year view. But that's because that's an average of a hundred years, including times when the S&P 500 PE was 6, 7 and 8, or one third of what it is right now.

Valuation matters a lot, and the stock market's really high and it's gonna be really hard to make money from here with any kind of long-term view."

In 2007, I was sitting on a large amount of undrawn commitments to invest in bombed out MBS securities.

Didn’t invest at all until 2008, didn’t get fully invested until March 2009.

It’s 2007 for Private Credit.

Come home to DoubleLine.

@LouiChristopher Who cares - waste of time. It’s all a big Ponzi scheme anywhere with super propping up stock market and government the job market with tax loop holes for housing.

Last night, I was contacted by a former roommate of Keir Starmer.

After our conversation, I now believe that he is the most dangerous Prime Minister Britain has ever had.

Here’s what he told me:🧵